Long: Amer Sports, Inc. (NYSE:AS), 12-month Target of $45.00, or ~39% upside

Mar 10, 2026

INTRODUCTION

Amer Sports is a global performance platform built around a portfolio of heritage brands anchored by Arc’teryx, the technical outerwear brand founded in the rugged Coast Mountains of British Columbia. Salomon and Wilson round out the foundational brands in the portfolio.

The group specializes in high-end technical gear and apparel with a premium positioning. Under new ownership and a strategic shift toward direct-to-consumer distribution, Amer has transitioned from a traditional multi-brand sporting goods conglomerate into a higher-growth premium platform.

In its most recent fiscal year, the company generated approximately $6.5 billion in revenue and ~$840 million in operating income, representing meaningful acceleration from its pre-IPO footprint. Operating margins have expanded as the mix shifts toward higher-margin technical apparel.

Amer is beginning to demonstrate a repeatable ability to scale niche performance brands into global platforms. At the same time, the current setup presents a compelling tension between rapid geographic and category expansion and the challenge of maintaining brand heat as the brands grow globally. That tension is what makes the stock interesting today.

The remainder of this post focuses on Arc’teryx and why the brand may still be early in its global scaling curve.

WHY CONSIDER THE STOCK DESPITE THE PREMIUM VALUATION?

At roughly 30x forward earnings, Amer does not screen as cheap on near-term fundamentals.

I am not arguing that this is the single highest IRR consumer opportunity available today. However, the past twelve months have marked the emergence of multiple growth curves within the portfolio.

Historically, the Amer story was largely synonymous with Arc’teryx growth in China. The brand’s performance in that region drove the majority of the investment narrative.

Going forward, that dynamic appears to be evolving.

Arc’teryx should continue to serve as a powerful growth engine driven by geographic expansion and category development, one that the company believes can scale from $2-3 billion today to $5 billion by 2030. At the same time, Salomon is beginning to emerge as a second growth pillar (which I will cover in Part 2), particularly as its footwear franchise gains traction globally.

If Salomon’s trajectory continues, the Amer story evolves from a company driven primarily by a single brand into a platform with two meaningful growth engines.

This matters for both revenue growth and margin structure. As Salomon scales, improvements in product mix and operating leverage should contribute incremental margin expansion.

In other words, the story is abouta strong asset becoming stronger while another brand begins to scale into a meaningful contributor.

If current trajectories hold, Amer may be entering a new growth phase that pushes out the typical maturity curve investors often expect from premium outdoor brands.

The Consumer Ascent is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

THE NICHE-TO-GLOBAL PLAYBOOK

Many of the most successful consumer brands follow a similar trajectory. A niche performance brand first earns credibility with the most demanding users before expanding into a broader cultural phenomenon.

Arc’teryx appears to be following that exact path.

Within the technical outerwear category, the brand has long held benchmark status among alpine climbers and mountaineers. Independent gear testing regularly ranks Arc’teryx shells at or near the top of the most demanding categories such as severe-weather alpine hardshells and mountaineering shells where durability, weather protection, and mobility are critical.

Specialist climbing media and expert reviewers consistently treat Arc’teryx as a reference brand for technical shells rather than simply another outdoor apparel label.

(Switchback Travel’s 2026 Hardshell Jacket Picks)

Salomon occupies a similar position within a different technical ecosystem.

In trail running and alpine sports, Salomon footwear and equipment have historically been developed alongside elite athletes and mountain guides. This close collaboration has helped the brand build deep credibility among serious runners and mountain athletes.

Today Salomon footwear frequently appears among the most recommended products in specialist gear guides across categories such as trail running and hiking. That continued presence reinforces the brand’s reputation as a technical benchmark within the category.

(Switchback Travel’s 2026 Hiking Shoe Picks)

This type of credibility among core users often precedes broader cultural adoption.

Nike built authority with elite runners before becoming a global lifestyle brand. Lululemon began within the yoga studio before expanding into a broader athletic lifestyle brand. Hoka first gained traction among ultramarathoners before entering the mainstream running market.

Arc’teryx and Salomon appear to be following a similar trajectory. Both brands have unusually strong technical credibility within demanding outdoor segments while still having relatively low global penetration relative to their brand heat.

That combination of intense loyalty among expert users and large untapped scale is often what precedes the most compelling growth stories in consumer brands.

The key question is whether the brands can maintain their technical authority as they expand into new categories.

It is worth noting that the management team appears highly sensitive to protecting brand integrity. Prior to the IPO, the company cut roughly 25 to 30 percent of SKUs it considered non-core and significantly reduced wholesale distribution, sacrificing hundreds of millions of revenue in the process in order to preserve brand equity.

In effect, the company deliberately slowed short-term revenue growth in order to protect the brand’s long-term positioning.

As Arc’teryx CEO Stuart Haselden summarized the philosophy:

“The world does not need Arc’teryx to make athleisure products. The appeal of our brand is that we are focused in a disciplined way, in a committed way, to making these performance products.”

Whether the company can scale new growth curves while preserving that discipline is the central question for investors.

THE ARC’TERYX PHENOMENON: TECHNICAL LUXURY

Market Awareness (scale up)

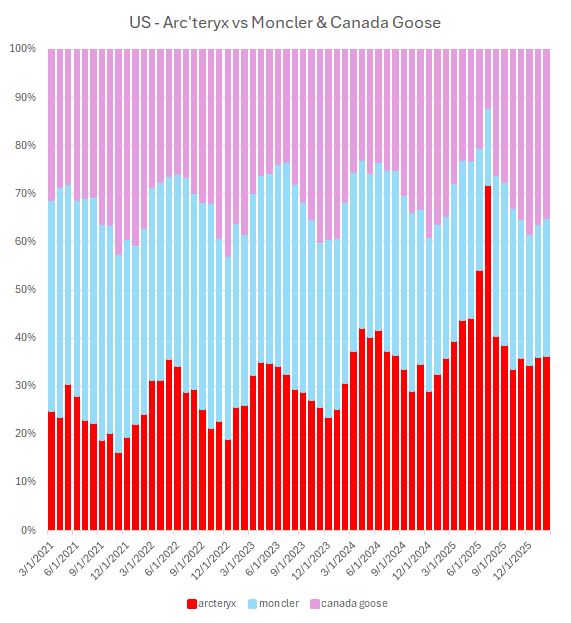

Arc’teryx occupies a rare position within the outdoor industry. It is simultaneously a technical performance leader and a status symbol.

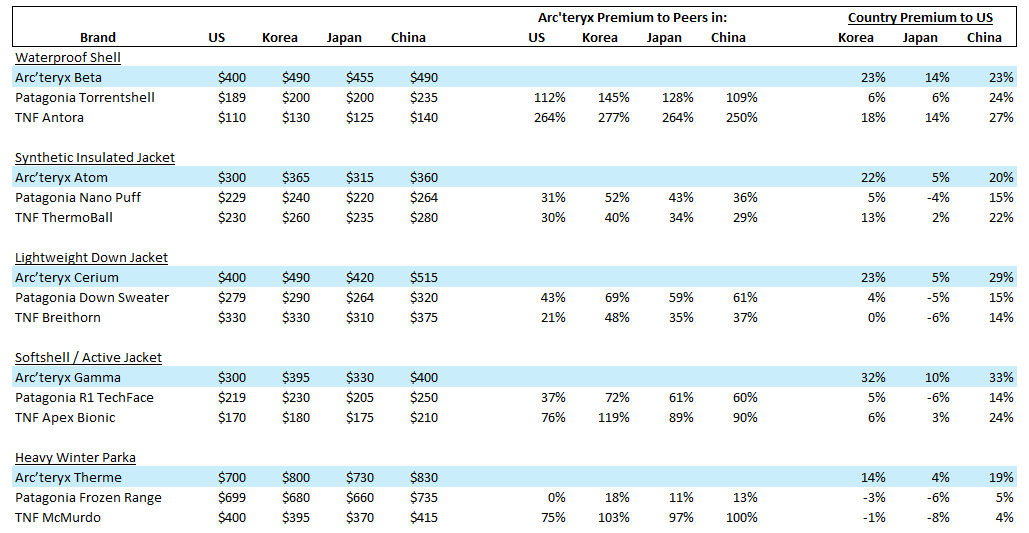

At $700 to $900 for a premium shell, Arc’teryx products are expensive relative to traditional outdoor brands. Yet they remain inexpensive relative to luxury outerwear brands such as Moncler or Canada Goose.

This positioning allows Arc’teryx to operate in two overlapping worlds.

On one side, the brand remains deeply embedded in the high-performance alpine ecosystem where technical credibility matters most. On the other, it increasingly functions as a premium lifestyle product worn in cities from Seoul to Manhattan.

The “deadbird” logo appears almost as frequently on urban streets as it does on mountain trails.

This dual identity creates a powerful dynamic. Arc’teryx competes simultaneously against technical outdoor brands and luxury outerwear brands, while maintaining pricing power in both arenas. Yet despite its strong pricing power and cultural momentum, the brand still trails larger outdoor peers in global awareness.

One way to observe this positioning is through search share, see below. Relative search trends suggest Arc’teryx is steadily gaining mindshare within both the performance and lifestyle ecosystems. The most interesting takeaway is not only that Arc’teryx is winning share from luxury brands, but that it also appears to be gaining traction against the traditional outdoor incumbents.

This suggests the opportunity may be less about convincing consumers to trade down from luxury and more about convincing mainstream outdoor customers to trade up.

Pricing Power in the Wholesale Channel

A common concern with premium brands is whether broader distribution eventually erodes pricing power.

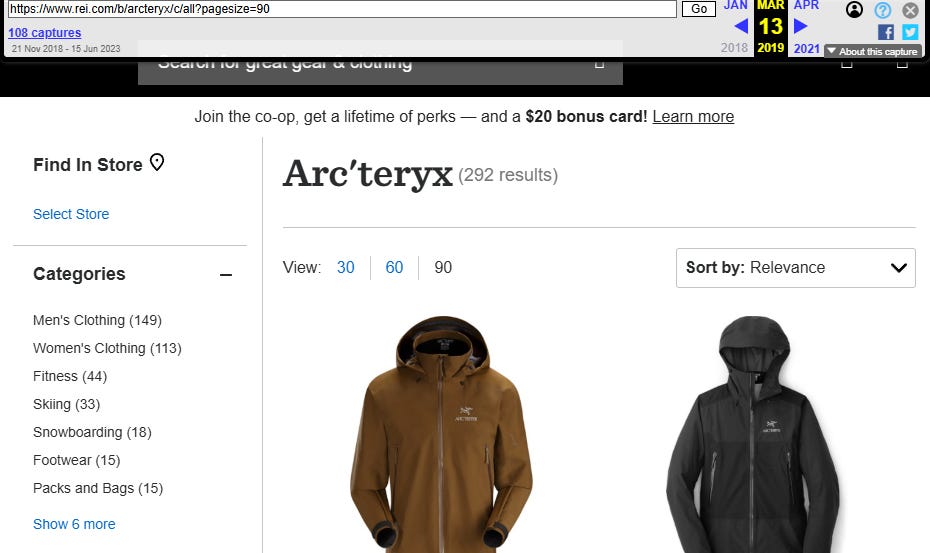

One way to test whether Arc’teryx’s premium positioning holds up in a competitive retail environment is to look at product-level performance inside a large wholesale partner such as REI.

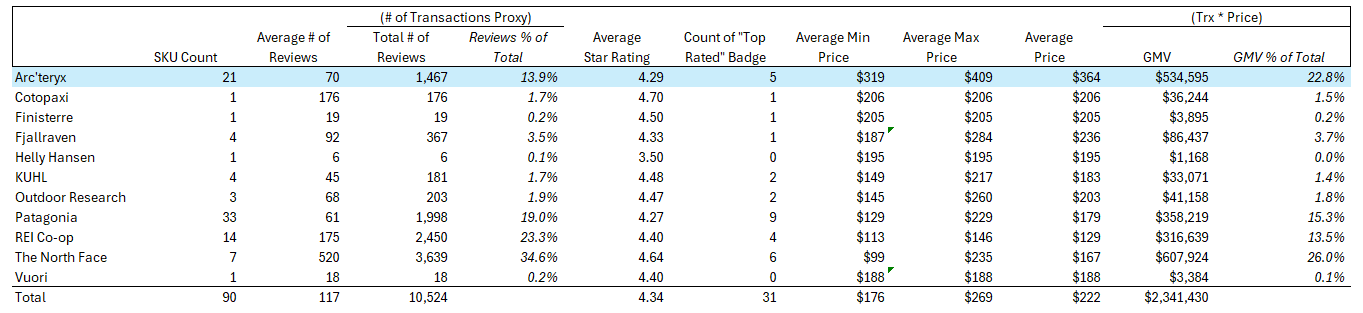

Let’s examine the top 90 jacket SKUs on REI’s website (with Arc’teryx Beta SL being the #1 bestseller):

The results are notable. The data shows the brand retains pricing power even in highly competitive retail environments.

Using review counts as a rough proxy for relative transaction volume (while acknowledging that reviews are an imperfect measure of demand), Arc’teryx accounts for only roughly 14 percent of unit demand within the category. However, because Arc’teryx jackets command significant price premiums, the brand represents approximately 23 percent of category GMV. And more importantly, Arc’teryx most likely commands close to 40% of the profit pool represented there.

The key takeaway is that Arc’teryx products frequently sell at more than a 50 percent price premium relative to the field while still capturing meaningful share within a broad outdoor retail environment.

In other words, even in a mass outdoor retail setting where consumers can easily compare alternatives, Arc’teryx continues to monetize at a premium.

This suggests that pricing power is not purely a function of scarcity or limited distribution. Instead, it appears tied to genuine brand preference once the consumer is exposed to the product.

Arc’teryx does not appear constrained by pricing power. The primary constraint appears to be exposure.

Once consumers encounter the brand, conversion and monetization appear unusually strong.

That raises a natural question:

How much larger can Arc’teryx become as global awareness expands?

The remainder of this post explores the major growth vectors that could potentially double the brand over time.

Retail Expansion and the Exposure Constraint

If awareness is the primary constraint on Arc’teryx’s growth, one of the most direct ways to address it is through owned retail expansion.

Direct-to-consumer channels have historically played an important role in the brand’s development. Unlike wholesale environments where Arc’teryx competes for attention alongside dozens of other brands, a dedicated store allows the company to fully control the consumer experience.

That matters for a technical brand. Much of Arc’teryx’s value proposition lies in details that are easier to communicate in person, including product construction, materials, and technical features.

A dedicated store also allows the brand to present its products within the broader Arc’teryx ecosystem rather than as a single item on a crowded rack.

This helps explain why the company has steadily expanded its owned store footprint over the past several years.

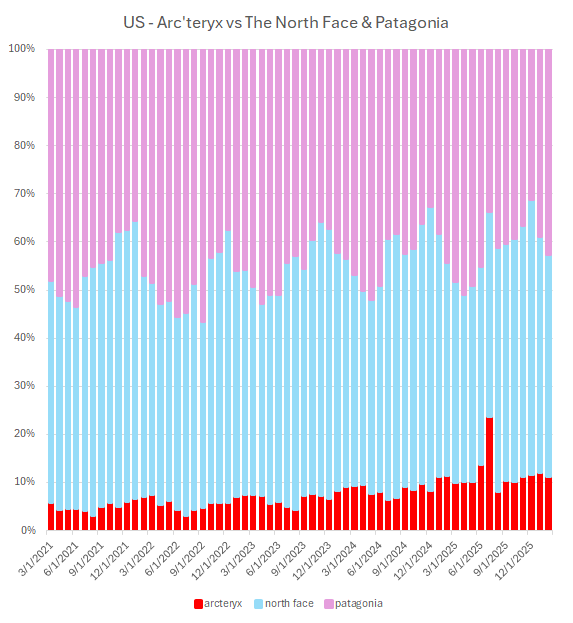

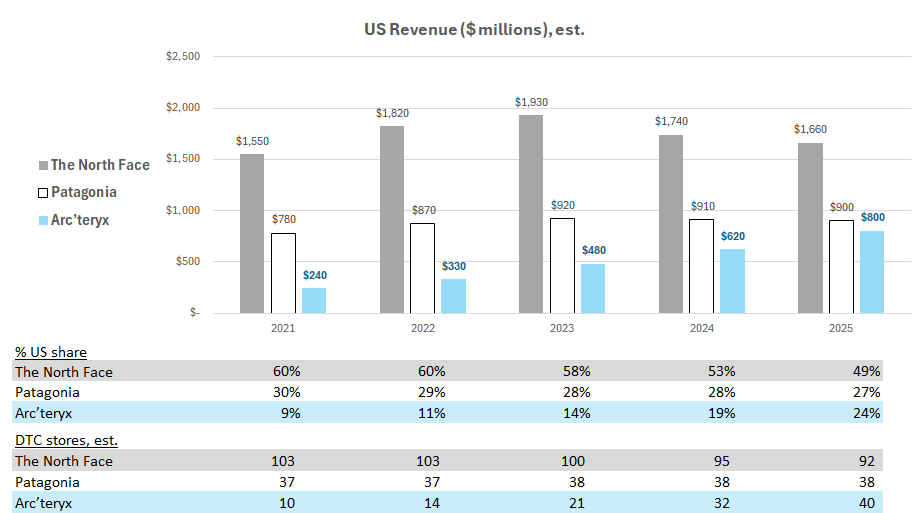

Despite that expansion, Arc’teryx still operates a relatively small retail network compared with peers such as The North Face and Patagonia, particularly in the United States.

At the same time, the growth of the Arc’teryx store base appears to have coincided with meaningful gains in U.S. market share.

A simple comparison of estimated U.S. revenue across Arc’teryx, The North Face, and Patagonia illustrates the gap in scale. Even with significantly lower wholesale penetration, Arc’teryx has managed to close part of the revenue gap as its retail footprint has expanded.

Adding another 40+ Arc’teryx stores in the U.S. appears reasonable when compared with The North Face, which operates roughly 90 stores in addition to its broad wholesale distribution.

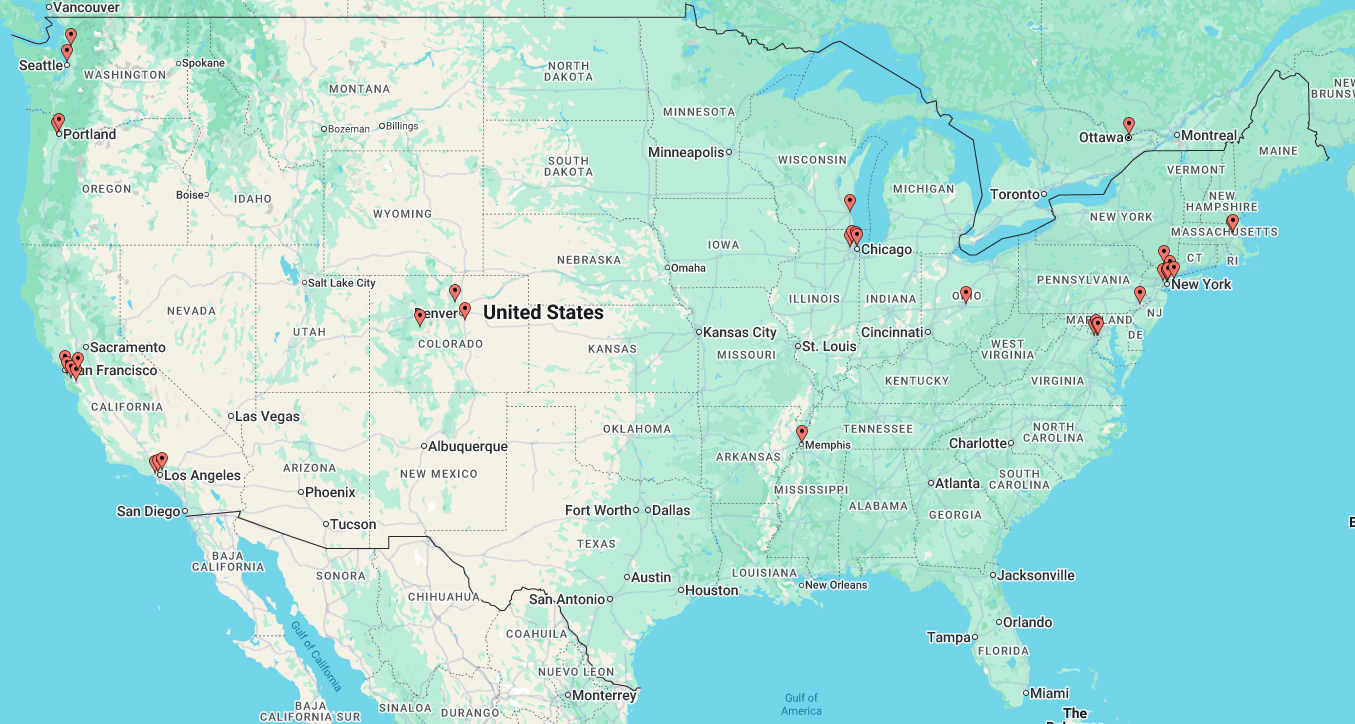

Additionally, looking at store location maps also reveals clear whitespace opportunities across the United States, both in entirely new markets and through additional infill within existing metropolitan areas:

Arc’teryx owned store base:

The North Face owned store base:

It’s incumbent on management to determine the health of the 2025 cohort relative to the 2022 stores, but assuming management continues to monitor store productivity closely, the opportunity to expand the retail footprint appears clear. 2026 will add somewhere around 10-12 stores (they’ve said the largest of the 25-30 net adds will be in the US), so we should be looking at a ~5 year growth opportunity just on increasing exposure in the US.

Assuming continued brand maturation alongside increased physical exposure, the U.S. market alone could represent up to $1 billion of incremental revenue opportunity over time.

APAC Opportunity (scale up)

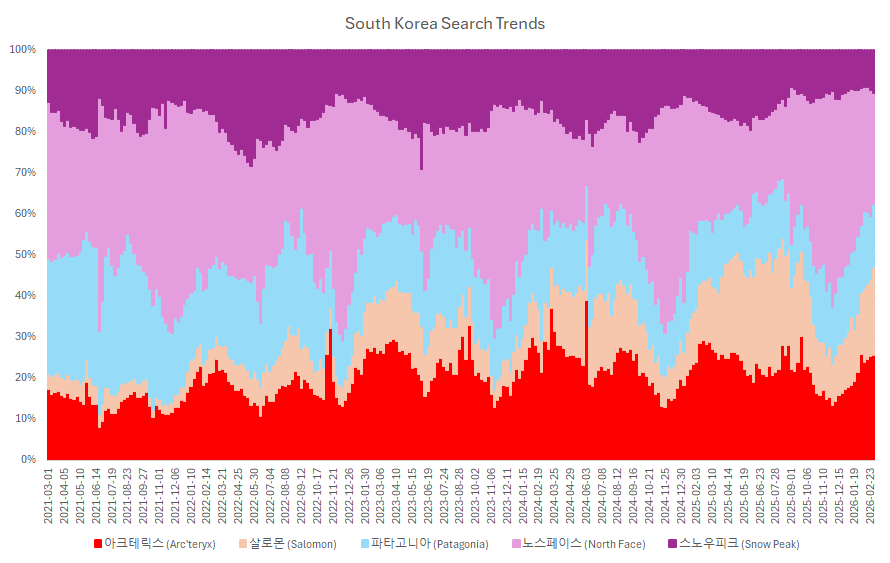

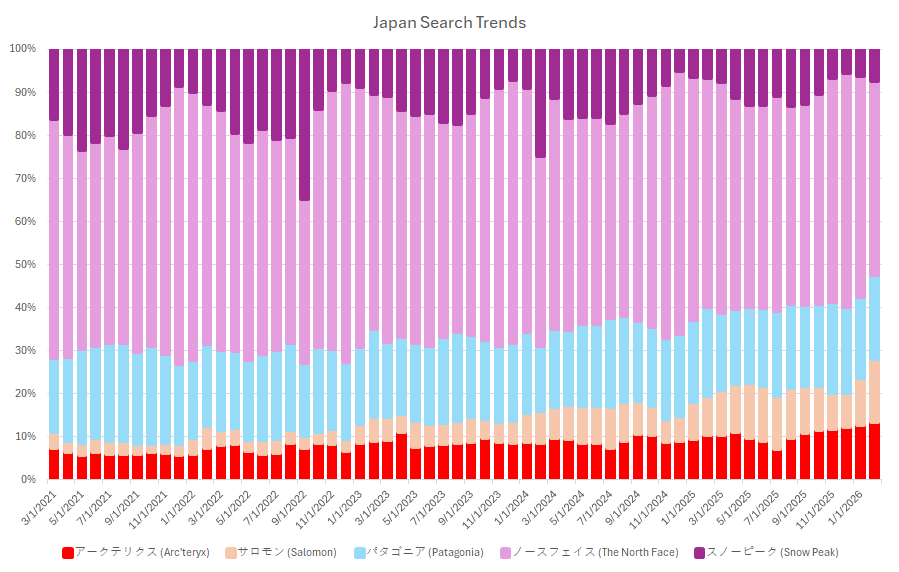

Another underappreciated aspect of the Arc’teryx growth story is the opportunity across Asia-Pacific outside of China, particularly in South Korea and Japan.

These markets already support large premium outdoor businesses. For example, local distributors of The North Face generate roughly $700 million in annual revenue in both South Korea and Japan.

By comparison, Arc’teryx only generates low hundreds of millions in each market today, suggesting significant room for expansion even without assuming category leadership.

Importantly, these markets operate at price tiers that are often higher than the United States, with premium outdoor apparel functioning as both performance gear and lifestyle fashion.

This dynamic is visible across many premium outdoor brands. In Korea and Japan, outdoor apparel often occupies a hybrid position between performance gear and fashion, which allows brands with strong technical credibility to command higher pricing.

Arc’teryx appears particularly well positioned within this ecosystem.

Search trend data below suggests the brand has already established strong cultural momentum in South Korea, while Japan is showing clear signs of increasing traction as well.

[side note: Interestingly, the same datasets also show rising momentum for Salomon, particularly in Korea, which has historically served as a leading indicator for emerging outdoor lifestyle trends globally.]

Taken together, the size of the existing premium outdoor market and the brand’s growing cultural momentum suggest that Arc’teryx still has substantial runway across APAC outside of China.

Even partial convergence toward the scale achieved by larger outdoor brands could represent several hundred million dollars of incremental revenue opportunity.

Category Expansion (scale out)

Beyond geographic expansion, Arc’teryx also has meaningful runway through category expansion within its existing customer base.

Women’s

Women represented roughly 25 percent of Arc’teryx revenue in 2025, up from approximately 22 percent in 2024. Management has stated a goal of reaching 30 percent mix by 2030.

Based on the company’s long-term revenue ambition, achieving that mix would represent roughly $800 million of incremental revenue.

Importantly, this target does not appear aggressive when compared with industry benchmarks.

The North Face previously disclosed that women represented approximately 35 percent of its business in 2019, with expectations that the mix would move toward 40 percent over time. Patagonia has also indicated that its customer base is roughly 50 percent men and 50 percent women.

Taken together, these benchmarks suggest that 40 percent revenue mix is a reasonable long-term ceiling for a mature outdoor brand, implying that Arc’teryx still has significant room to expand from current levels.

Several indicators suggest this shift is already underway.

First, participation data continues to move in the right direction. According to the Outdoor Industry Association, women accounted for more than 50 percent of outdoor recreation participants for the first time in 2024.

Second, search data suggests growing interest in the brand among female consumers. Pinterest searches for terms such as “Arc’teryx jacket” have grown steadily over the past several years, which is notable given Pinterest’s strong female user base.

Finally, the company has been expanding its women’s assortment.

Using REI’s product catalog as a rough proxy for assortment breadth, the number of Arc’teryx women’s SKUs has grown meaningfully over time. A snapshot of the REI catalog in 2019 shows:

2019 - Mens: 149 // Womens: 113

Today the assortment is at parity:

2026 - Mens: 201 // Womens: 208

This suggests that women’s product development has been a deliberate focus for the brand over the past several years.

Marketing activity appears to reflect the same shift. A simple review of Arc’teryx’s recent Instagram posts shows that women account for a majority of the identifiable athletes and models (17 of the last 25) in recent campaigns:

Together, these signals suggest that Arc’teryx is actively investing behind a category that still has meaningful runway relative to industry peers.

Footwear

Footwear represents a second category expansion opportunity, though this one carries more uncertainty.

Footwear accounted for roughly 8 percent of Arc’teryx revenue in 2025 and exited the year growing approximately 40 percent, up from roughly 35 percent growth in the prior quarter.

Management’s long-term goal is for footwear to reach approximately 13 percent of revenue by 2030.

If the company ultimately achieves its broader $5 billion revenue aspiration, that mix would imply a footwear business approaching $650 million in annual revenue. From the current base of roughly $200 million, this would represent approximately $450 to $500 million of incremental opportunity.

Skepticism around this category is understandable. Footwear represents a larger leap from Arc’teryx’s historical core competency in technical outerwear.

That said, the progress to date is notable.

The footwear division was originally established in 2015 but underwent a significant strategic reset in 2021, mirroring the broader brand strategy of reducing non-core SKUs and refocusing on technical performance.

Since then, the company has invested heavily in building the category.

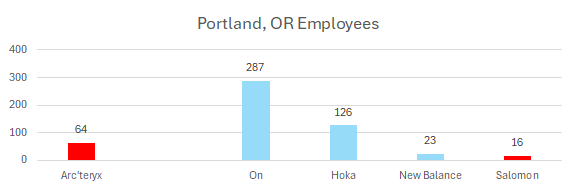

Arc’teryx established a dedicated footwear development presence in Portland, widely regarded as the center of the global performance footwear industry. The team initially consisted of only a handful of employees but has grown to several dozen employees based on LinkedIn headcount data.

While headcount data alone is not conclusive, the expansion suggests a sustained commitment to developing in-house footwear capabilities.

Operationally, the category also appears to be gaining strategic prominence. The Arc’teryx website recently introduced a dedicated footwear navigation category, reflecting the company’s growing emphasis on the segment.

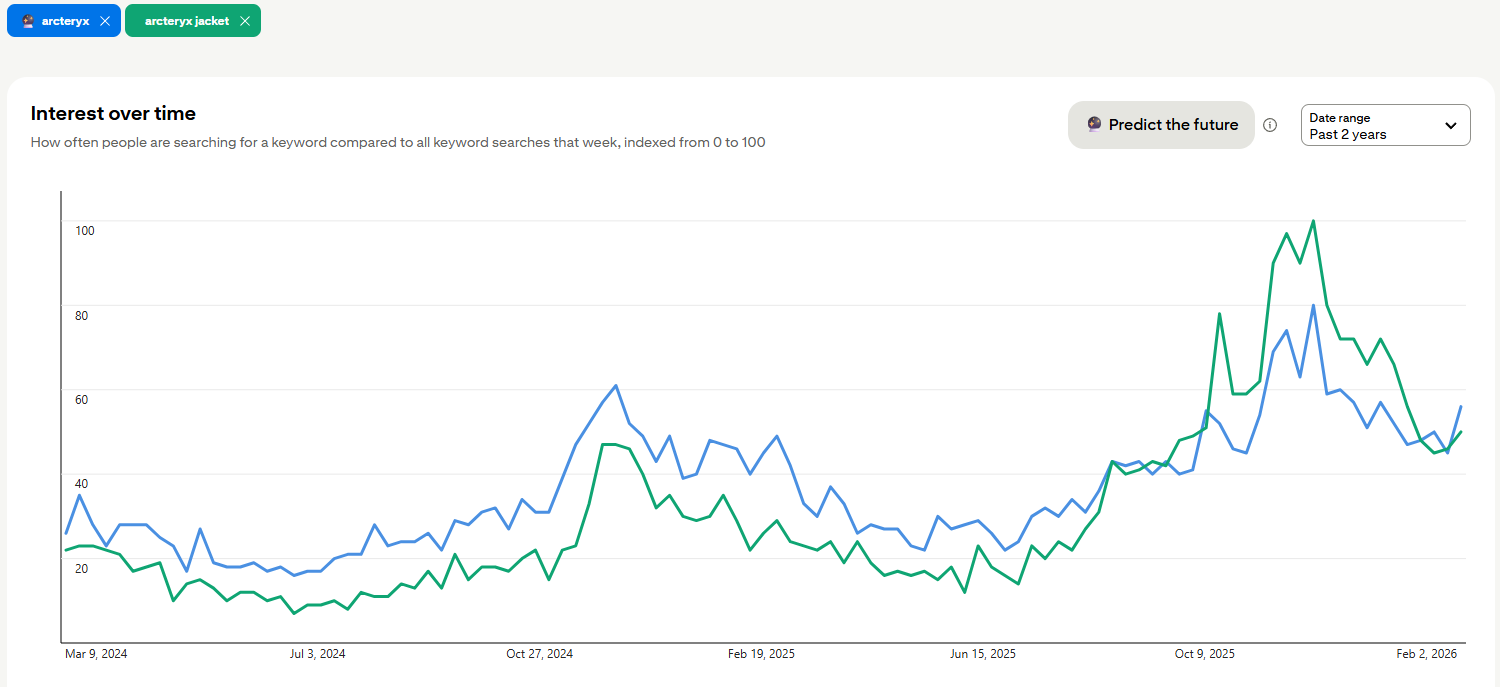

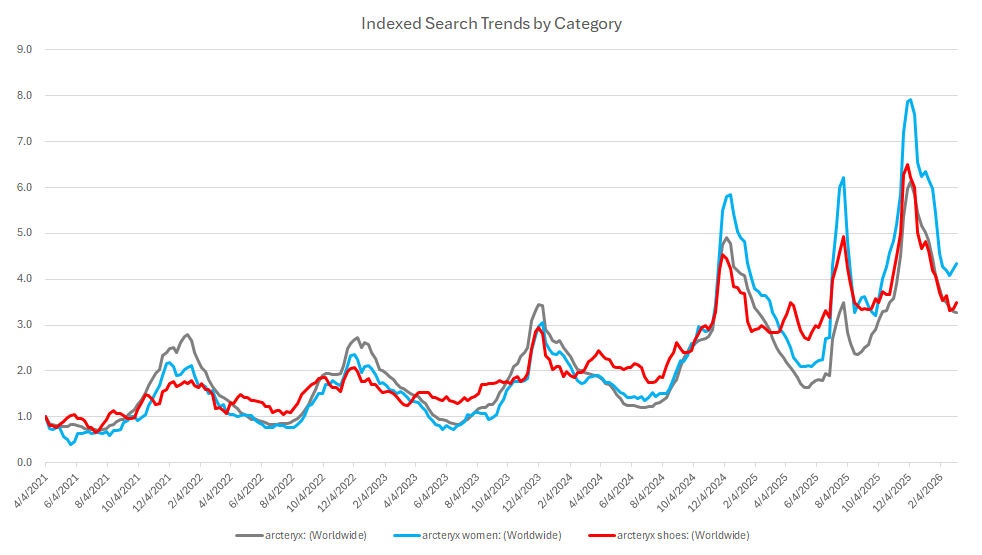

One way to corroborate whether these (womens & footwear) initiatives are working is by indexing search results starting from five years ago. Below, we see that the growth in searches for the womens category started to outperform the overall business in the 2024 peak season and the footwear category reaching parity relative to the overall peak starting this past year.

Prior to, let’s say, 12-18 months ago, the nascent categories were lagging the overall key term (though closing the gap), which wasn’t great. Even now, you’d want these newer divisions to significantly outperform the overall by an amount larger than those you see above, but it’s a step in the right direction and indicative of traction.

DURABILITY OF THE BRAND

One legitimate question is whether Arc’teryx’s recent cultural momentum reflects a durable brand advantage or simply a temporary fashion cycle tied to the broader “gorpcore” trend.

However, unlike many fashion-driven brands, Arc’teryx built its reputation within technical alpine environments decades before its recent urban popularity. The brand’s credibility among core users and its disciplined approach to distribution suggest the current momentum may reflect structural brand strength rather than a purely cyclical fashion moment.

This reinforces an earlier point about the importance of maintaining the brand’s technical heritage. As CEO Stuart Haselden has emphasized, Arc’teryx is intentionally focused on performance products rather than expanding indiscriminately into lifestyle categories.

Preserving that discipline will be critical. Many premium consumer brands have damaged their long-term equity by pursuing growth too aggressively and diluting what made the brand distinctive in the first place.

CLOSING THOUGHTS

Arc’teryx today sits at an interesting point in its evolution.

The brand has already established itself as the technical benchmark in its category. It commands premium pricing, maintains strong cultural momentum, and continues to expand geographically and across new product categories.

Yet relative to its global peers, Arc’teryx still appears early in its global awareness curve.

If the company successfully executes across the opportunities discussed above, including U.S. retail expansion, growth in APAC outside of China, women’s category development, and footwear scaling, the brand could plausibly grow from roughly $2-3 billion today toward the company’s stated $5 billion ambition by 2030.

If Arc’teryx ultimately approaches $5 billion in revenue, the incremental operating income could be substantial given the brand’s premium pricing and growing DTC mix. That path would represent one of the most impressive brand scaling stories in modern outdoor apparel.

Taken together, these opportunities suggest Arc’teryx may still be early in its global scaling curve despite its already strong momentum. If the brand’s conversion and pricing power remain intact as awareness expands, Arc’teryx’s long-term ceiling may be significantly higher than its current scale suggests.

But Arc’teryx is no longer the only growth engine inside Amer Sports.

While Arc’teryx has dominated the narrative around the company for several years, another brand inside the portfolio has quietly begun building its own growth curve.

In many ways, Salomon may now be at the stage Arc’teryx occupied several years ago. It has deep credibility within its core performance ecosystem, rising cultural momentum, and a rapidly expanding global footwear franchise.

If Arc’teryx represents the first chapter of Amer’s growth story, Salomon may represent the second.

That will be the focus of the next post.

The Consumer Ascent is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.