Consumer Brief #2: Week of April 12, 2026

A look at the tape, themes, earnings recaps, and the week ahead

Key events calendar | On the Tape | Themes: 1) The ceasefire changed the tape but not the consumer math 2) March CPI: hot headline, clean core; what the Fed does with it 3) What LEVI’s Q1 actually tells us about the pre-war consumer | Recent earnings: LEVI, DAL | Into this week: banks dominate, but watch the read-throughs

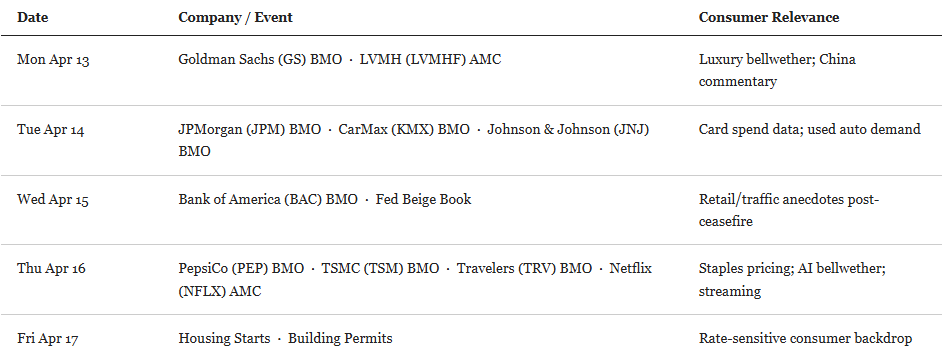

Calendar

On the Tape

The S&P 500 closed Friday April 10 at approximately 6,817, up roughly 3.5% for the week, its best weekly performance since November. The entire move was geopolitical. On Wednesday evening, April 8, Trump announced a two-week ceasefire with Iran contingent on the reopening of the Strait of Hormuz. The Dow surged 1,325 points on Wednesday, its best single day in over a year. Oil fell 13-16% on the ceasefire news, Brent dropping to around $94 before partly rebounding to close the week near $96.

The relief was real but partial. The Strait has not fully reopened as of Sunday April 12, though transit activity picked up through the week. Three fully laden supertankers passed through on April 11, the first oil-carrying vessels to exit the Gulf since the ceasefire deal, per Reuters. Earlier in the week only bulk carriers carrying dry cargo had transited. A large backlog remains: MarineTraffic data showed 187 laden oil tankers with approximately 172 million barrels still inside the Gulf as of the ceasefire announcement. Iran said passage requires coordination with its armed forces, and Israel’s continued strikes on Lebanon complicated the terms almost immediately. Vance led the US delegation to Islamabad for formal talks on April 11, left Sunday without an agreement, and Trump announced a US naval blockade of ships going to and from Iranian ports, starting Monday. The ceasefire is technically intact but under significant strain.

The sector rotation from last week partially reversed. Energy gave back some gains as oil fell. Consumer discretionary, airlines, and travel names rallied sharply. The XLE fell roughly 4% on Wednesday alone after leading the market for six weeks. VIX dropped from the mid-20s to just above pre-war levels.

The Fed picture shifted slightly. March CPI came in at +0.9% MoM seasonally adjusted, +3.3% YoY, the highest annual reading since May 2024. But core (ex food and energy) rose only +0.2% MoM and +2.6% YoY, both below forecast. CME FedWatch barely moved. Goldman Sachs noted the Fed can “look through the energy-driven noise so long as these factors hold.” The ceasefire, if it holds, removes the most acute inflation risk; if it breaks down it reverses fast.

What Matters This Week

1) The Ceasefire Changed the Tape but Not the Consumer Math

The market’s Wednesday relief rally was rational. A ceasefire and Strait reopening, if sustained, removes the primary inflationary pressure on the consumer: gas prices, logistics surcharges, airline fares, freight costs feeding into goods prices. When the Strait was closing in March, Consumer Discretionary was the worst-performing S&P sector. When the ceasefire was announced, airlines jumped 10-12%, travel stocks led the market, and the rotation reversed sharply.

But the consumer’s situation has not actually improved yet. Gas prices nationally were still around $4 as of this week, well above the $2.98 they were on February 26. Even if Brent stabilizes in the $90s, the pump-price relief takes weeks to show up, and the damage to confidence from the March shock has already been registered in the data. University of Michigan sentiment plunged to a preliminary April reading of 47.6, a record low for the survey going back to 1952, down from 53.3 in March. Bank of America Institute transaction data showed gasoline spending up 14.4% year over year in the week to March 14.

The ceasefire is only days old, and this week will be the first real test of whether it holds. Vance left Islamabad without an agreement on April 12 and Trump announced a US naval blockade of ships going to and from Iranian ports, starting Monday. If the Strait reopens durably and oil falls toward $70-80, the consumer recovery thesis reasserts. If the talks collapse and the Strait closes again, the market gives back much of Wednesday’s rally and the consumer headwind resets. This is the dominant variable for every consumer name through the end of April.

One read-through that does not depend on the oil path: the Islamabad talks failing on April 12 does not by itself invalidate the ceasefire, which technically remains in place. The naval blockade announcement is consistent with Trump’s pattern of escalating pressure between rounds of negotiation. Watch whether the ceasefire survives this week as the first real test.

2) March CPI: Hot Headline, Clean Core

March CPI came in at +0.9% MoM (seasonally adjusted) and +3.3% YoY, the highest annual reading since May 2024. Energy drove it: the energy index rose 10.9% for the month, with gasoline up 21.2%, accounting for nearly three-quarters of the entire monthly increase. Shelter rose 0.3%. Food was unchanged for the month. Core (ex food and energy) rose just 0.2% MoM and 2.6% YoY, both 0.1 percentage points below forecast.

The Fed’s read is that this is energy noise, not embedded inflation. Services ex-energy rose 0.2% and are up 3% annually. Shelter at 3% annually is tied for its lowest level since August 2021. Apparel climbed 1% (one of the few non-energy categories showing war-related pass-through) and airfares jumped 2.7%. Medical care, personal care, and used cars all fell.

Raymond James chief economist Eugenio Aleman said: “As long as the increase in gasoline prices is not translating into an increase in the core measures of inflation, the Fed is probably not going to react to the noise in the headline measures.” That is the operative framework for now. Core PCE for February came in at 2.8% YoY, still above target but not accelerating. The April CPI, due May 12, will show whether the ceasefire-driven oil pullback is feeding through to gas prices, or whether the supply chain disruptions from six weeks of Strait closure are starting to show up in goods and food prices more broadly. That print will either validate the energy-transitory framing (geopolitical noise that unwinds as the Strait reopens) or complicate it.

For consumer companies, the March CPI print has three practical implications. First, real wages fell 0.6% in March, the consumer’s purchasing power declined even as nominal wages rose 0.2%, because energy inflation outpaced earnings. Second, the tariff overlay is still present: apparel at +1% in March suggests the trade policy headwinds haven’t gone away even as the energy shock grabbed the headlines. Third, the April print, which will capture the ceasefire’s effect on gasoline, will either validate the transitory framing or complicate it. If gas prices at the pump fall 30-40 cents by mid-April, the April CPI is clean. If the Strait stays restricted, it won’t be.

3) What LEVI’s Q1 Actually Tells Us About the Pre-War Consumer

Levi reported Tuesday April 7 and the result was a genuine beat across every line. Revenue +14% reported (+9% organic) to $1.74B against a $1.65B consensus. Adjusted EPS $0.42 vs $0.38 consensus. DTC comparable sales +7% for the 16th consecutive positive quarter. DTC is now 52% of total revenue. FY2026 guidance raised across revenue, margins, and EPS, reported net revenue growth guided to 5.5%-6.5%, adjusted EPS to $1.42-$1.48. Stock +6.3% in after-hours.

The framing matters here. Q1 ended March 1, meaning the quarter captured only the first two days of the conflict. This is not a clean war-era consumer read: it is a strong brand-demand read from a period when consumer sentiment was softer but the oil shock had not yet hit. The better way to read it: a premium DTC brand grew 9% organically through a period of pre-existing macro softness, entering the war in a position of strength. Management’s comment that “positive quarter-to-date trends” supported the raised guide on April 7 (six weeks into the conflict) is the actual war-era signal, and it is directionally encouraging. Europe led with 24% reported growth. Americas rose 9% with the US up 4%.

Two things worth watching from the call. First, CFO Harmit Singh announced his retirement after a planned transition. Singh architected the DTC pivot that is now clearly working. His departure is not a crisis (new CEO Michelle Gass has been the strategic driver) but it is a succession watch. Second, gross margin came in at 61.9%, down 20bps year over year, primarily from tariffs, partially offset by pricing and fewer promotions. The company absorbed the tariff headwind without giving back margin. That is the playbook working as designed.

The broader read: a premium DTC brand growing 9% organically in a period that included the onset of a war and an oil shock is a signal that the consumer bifurcation thesis remains intact. Higher-income consumers with direct brand relationships are not cutting denim. The segment most at risk, lower-income discretionary, is LEVI’s smallest exposure. The DTC mix means lower price sensitivity and fewer markdowns. This is the right positioning for the current environment.

Recent Earnings

LEVI: Guidance raised. DTC at 52%.

Covered in full under Theme 3. Key numbers: revenue $1.74B (+14% reported, +9% organic), adjusted EPS $0.42 vs $0.38 consensus, DTC comps +7% (16th consecutive positive quarter), gross margin 61.9% (-20bps from tariffs, absorbed). FY2026 reported net revenue growth guided to 5.5%-6.5%, adjusted EPS to $1.42-$1.48. Stock +6.3%.

DAL: Record revenue, fuel the overhang.

Q1 2026 (April 8 BMO): record operating revenue of $15.9B, or $14.2B on an adjusted operating basis (+9.4% YoY), adjusted EPS $0.64 vs $0.62 consensus. Premium and loyalty revenue now 62% of total, corporate travel at record levels with double-digit growth across all sectors. The first-quarter beat was driven by the first eight weeks of the year, before the oil shock hit mid-quarter. Management did not update full-year guidance given fuel cost uncertainty, but guided Q2 pretax profit of $1B and noted a $300M benefit expected from its refinery operation. All-in fuel cost expected at $4.30/gallon in Q2.

The consumer read-through: premium travel is holding. Corporate travel is at record levels. The demand story is intact; the margin story depends entirely on whether the ceasefire holds and jet fuel normalizes. Delta stock +12% on April 8 ceasefire day, one of the biggest single-day moves in the sector.

Into This Week

The earnings calendar this week is heavier on consumer read-throughs than the bank-heavy headline suggests.

JPMorgan Tuesday is still the closest thing to a real-time March consumer read. Card spend data by category will show how much of the energy-wallet squeeze actually moved through household spending. Watch for any commentary on delinquency trends and gas-category concentration.

CarMax also reports Tuesday morning. Used auto demand, payment affordability, and credit approval rates at CarMax give a direct read on lower-to-middle income consumers transacting on big-ticket purchases during the oil shock. It is one of the cleanest consumer stress indicators available this early in the earnings cycle.

LVMH reports Monday after the close. As the bellwether for global luxury, the revenue print will show whether high-end consumers stayed engaged through the March geopolitical shock. The China and Asia commentary will be the most watched line; it is the same dynamic driving the Nike thesis from two weeks ago, and LVMH’s read tends to lead the sector.

Thursday is the most consumer-dense day of the week. PepsiCo reports before the open and will show whether staples pricing power is holding or whether snack and beverage volumes are finally hitting a ceiling as energy inflation compresses household budgets. Netflix reports after the close, in a geopolitical environment that pushes consumers toward home entertainment, streaming engagement is a proxy for consumer caution as much as a discretionary spend signal. TSMC also reports Thursday; less directly consumer-facing but the most reliable read-through for smartphone, PC, and gaming demand through the rest of 2026.

The Fed Beige Book drops Wednesday and will be the first anecdotal read on business conditions post-ceasefire, drawing on district contacts across retail, manufacturing, and services.

March retail sales are not out until April 21. That print, the first hard spending data to capture the full month of the oil shock, is next week’s setup, not this week’s.