Consumer Brief: Week of April 5, 2026

A look at the tape, themes, earnings recaps, and the week ahead

Themes: 1) Oil-shock math: how much energy inflation can the consumer actually absorb? 2) Nike and the China problem every Western consumer brand has 3) Amazon FBA surcharge signals logistics inflation incoming | Recent earnings: NKE, RH, PVH, Pop Mart, GME, CHWY, DRI | Into this week: LEVI, March CPI, FOMC minutes | Key events calendar

On the Tape

The S&P 500 spent most of March below its 200-day moving average and closed Thursday April 2nd near the low end of its 2026 range. US markets closed Friday April 3rd for Good Friday. The March jobs report (+178K, well above the +59K consensus) was released Friday but will be absorbed by markets Monday morning for the first time. It was stronger than expected, arriving in a tape that has been driven primarily by oil and geopolitics rather than economic data.

Consumer Discretionary (XLY) was among the worst-performing S&P sectors in March, while Consumer Staples (XLP) held up better as a defensive trade. Energy (XLE) remains the standout sector performer year-to-date.

Brent crude closed the week near $109/barrel, up from around $108 on Thursday April 2nd as futures continued to move through the holiday. The national average gas price is $4.10 as of Sunday April 5 per AAA, up from $2.98 on February 26 -- a $1.12 increase in five weeks. California is above $5.50. Diesel is around $5.45 nationally, up roughly 45% since the conflict began February 28. The Strait of Hormuz is operating under selective access as of April 5, more than five weeks into the conflict. Iran has maintained a permission-based transit regime, allowing some non-US/non-Israeli-linked vessels through while restricting others. Trump posted on Truth Social this morning giving Iran until Tuesday evening (later specified as Tuesday 8:00pm ET) to reopen the strait or face strikes on Iranian power plants and bridges. The IEA authorized the release of 400 million barrels of emergency reserves on March 11.

The Fed held rates steady at its March 18–19 meeting, and Chair Powell said near-term inflation expectations had risen in recent weeks, likely reflecting higher oil prices. Since then, stronger March jobs data and the oil shock have pushed rate-cut expectations further out, with markets increasingly pricing a prolonged hold. Wednesday’s FOMC minutes will matter less for fresh policy direction than for how much the committee was already incorporating energy-driven inflation risk at the March meeting.

What Matters This Week

1) Oil-Shock Math: How Much Can the Consumer Actually Absorb?

Five weeks in, the energy shock has produced actual consumer data rather than just forecasts.

University of Michigan consumer sentiment hit 55.5 in March. What matters: surveys taken before February 28 showed improvement from the prior month. Surveys taken in the nine days after the strikes “completely erased those initial gains,” per survey director Joanne Hsu. Gas spending in the week to March 14 was up 14.4% year over year per Bank of America Institute transaction data.

Context on risk: US households spend a relatively small share of income on energy compared to the 1970s, and the pattern in prior oil shocks is that consumption does not contract materially until prices stay elevated for an extended period. We are not there yet. The complication is that the shock is broader than just crude: diesel up 45%, LNG disrupted, fertilizer supply constrained. And the consumer was already softening before the war began, with February payrolls revised to -133K and confidence data deteriorating since January.

This part is already showing up in the data: lower-income households are spending more on gas than they were in February, consumer confidence broke sharply in the two weeks after the strikes, and the retailers most exposed to lower-income discretionary traffic (FIVE, DLTR, DG) carry more near-term risk on QTD trends than their Q4 prints suggest.

2) Nike and the China Problem Every Western Consumer Brand Has

NKE fell 15.4% on April 1st on Q3 results that beat on both revenue and EPS. The guidance was the issue: Q4 revenue guided down 2-4% against Street expectations of +1.9% growth, with Greater China guided to decline 20% in Q4. That is multiple consecutive quarters of deterioration in China, and management said the recovery there “is not happening at the level or the pace we need.”

The problem is not specific to Nike. Every Western consumer brand with significant Greater China exposure faces the same dynamic: domestic Chinese brands (Anta, Li-Ning) have closed the technical performance gap while offering stronger local relevance and lower prices; the post-pandemic Chinese consumer has shifted toward domestic brands; and inventory resets in the digital channel take multiple quarters without damaging brand equity. Nike is large enough that its China trajectory shapes the narrative for the whole sector. If Nike, with its marketing budget and World Cup activation capability, cannot stabilize China by Q2 FY27, the market will apply a more skeptical lens to every Western brand’s China recovery timeline.

3) Amazon FBA Surcharge: Logistics Inflation Is Coming for Marketplace Prices

On April 2, Amazon announced a 3.5% fuel and logistics surcharge on FBA fulfillment fees effective April 17 in the US and Canada, expanding to Buy with Prime and Multi-Channel Fulfillment on May 2. The average impact is $0.17/unit for standard US FBA orders. Amazon called it “temporary.” In 2022, Amazon ran a similar 5% surcharge under the same framing and it was subsequently absorbed into the permanent fee structure.

The Amazon announcement sits alongside two other surcharges announced in the same period: USPS adding 8% on packages effective April 26, and UPS/FedEx fuel surcharges already running at up to 26% of total shipping cost since early March. Diesel is at $5.45 nationally.

A substantial majority of Amazon units come from third-party sellers, most of them using FBA. Most sellers will reprice within 60-90 days or absorb the hit on margins. Either way, consumers are likely to see higher marketplace prices or fewer SKUs by June. For retail investors, every brand using FBA as a primary fulfillment channel carries this cost as an undisclosed headwind to Q2 and Q3 margins unless they have already adjusted pricing.

Earnings Recaps

NKE: China Is the Story

Nike’s 15.4% drop on April 1 perfectly illustrates the China problem covered in Theme 2. The Q3 print itself was fine, with revenue in line at $11.28B and a bottom-line beat of $0.35 against the $0.28 consensus. The market punished the forward view. Management guided Q4 revenue down 2% to 4% against Street expectations of positive 1.9% growth, entirely dragged down by a projected 20% decline in Greater China. At roughly $44 a share, Nike is now down about 70% from its pandemic peak and triggered over twenty analyst price target cuts in a single morning.

RH: The Most Interesting Guidance in Home

RH missed on both lines, reporting $842.6M in revenue and $1.53 adjusted EPS against a $2.21 consensus, sending the stock down roughly 22% on April 1. Management pointed to $30M in tariff-related sourcing backorders and $10M in late-quarter adverse weather as the culprits, masking what they described as solid underlying demand.

The near-term pressure is evident. RH is simultaneously absorbing margin pressure from tariff sourcing changes, a rate-sensitive housing market, and the front-loaded costs of its international gallery expansion in Paris, Milan, and London. First-quarter EBITDA margin is projected to fall to the 5.5% to 6.5% range due to these startup costs. Gary Friedman’s long-term targets remain intact on paper, but the compressed timeline leaves less room for error in 2026.

PVH: Lapping a Genuine Cultural Moment

PVH absorbed a 170bps gross tariff impact in Q4 and still managed to post a 10% operating margin, beating non-GAAP EPS consensus by 16% at $3.82. Tommy Hilfiger grew 7% and Calvin Klein added 3%.

What makes PVH interesting heading into 2026 is the cultural energy surrounding its two core brands. Calvin Klein is riding a wave from the Hulu series Love Story, which CEO Stefan Larsson said on the call was the platform’s most-streamed show ever. That momentum helped drive men’s underwear up 20% and women’s up 13%. Meanwhile, Tommy Hilfiger just tapped Travis Kelce as a global ambassador for fall 2026. Neither of these completely offset the reality of flat FY2026 revenue guidance or the fact that their heavy reliance on Bangladesh and Vietnam exposes them to the freight cost spikes from the Iran conflict. But the brand heat is real, and that matters for full-price sell-through.

Pop Mart: A 22% Haircut on a Growth Reset

Pop Mart delivered a strong 2025, with revenue up 185% to $5.1B and net profit up 308% to 12.78B yuan. The Labubu property alone generated 14.2B yuan, a 366% spike. Yet the stock fell 22% in Hong Kong on March 25th.

The sell-off was a reaction to forward guidance. Management set the 2026 growth floor at “no less than 20%.” After printing 185%, the market read that as a deceleration warning. Pop Mart has repeatedly relied on breakout IP cycles, and the market is clearly asking how durable Labubu will be once the growth rate normalizes. Any sign of slowing sell-through will immediately validate the skeptics who view this as a fad rather than a durable platform.

GME: The Bitcoin Covered-Call Footnote

GameStop missed Q4 revenue expectations, posting $1.10B against a $1.47B consensus as the core retail business remains in managed decline. They managed an EPS beat of $0.49 on cost discipline. The stock barely moved. The 10-K included a balance-sheet disclosure related to the company’s Bitcoin holdings that signals management is treating the position as a yield-generating vehicle rather than a pure appreciation bet -- worth reading if you follow the GME holding-company thesis.

CHWY: The Pet Economy Holds the Line

Chewy posted a strong beat with full-year reported revenue growth of 6.2%, or 8.3% normalized for the 53-week year. Management guided 2026 up approximately 8.5% at the midpoint. Autoship is now up to 84% of net sales, meaning 84 cents of every dollar is recurring revenue. The stock popped 12% on the print. Chewy is not entirely immune to a macroeconomic downturn, but pet care tends to be one of the last categories consumers cut when budgets tighten. Between the autoship penetration and the rollout of 18 total Vet Care clinics, it remains a relatively defensive name in the consumer space.

DRI: Solid Quarter, LongHorn Is Accelerating

Reported three weeks ago but worth including for context. Q3 FY2026: total sales +5.9% to $3.35B, blended SSS +4.2%, outperforming the casual dining industry benchmark by 540bps. Beef inflation was a 50bps margin headwind. LongHorn comps +7.2%, outperforming the benchmark by 840bps. Bahama Breeze resolved: 14 closures, 14 conversions. FY2026 guide reiterated. CEO Cardenas flagged GLP-1-friendly menu development at Olive Garden on the call, an early example of a casual dining chain treating GLP-1 as a structural demand variable worth planning around.

Into This Week

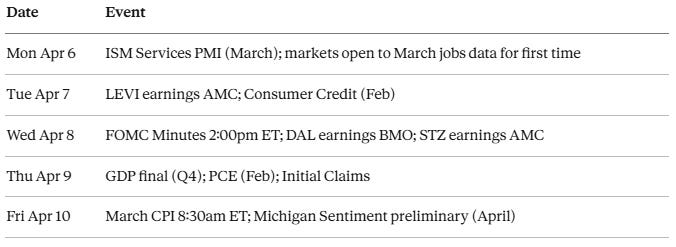

LEVI (reports Tuesday April 7, AMC)

Levi announced on March 3 that the Dockers sale to Authentic Brands Group had closed on February 27, leaving the company centered on Levi’s and Beyond Yoga. DTC was roughly half of FY2025 sales and 49% of Q4 revenue, and it helped drive FY2025 organic growth of 7%. Q1 FY2026 is the first reported quarter after the Dockers close, though the quarter itself still included nearly all of the pre-close period.

Expectations: revenue consensus $1.65B (+3.2% YoY), split approximately $812M Americas, $455M Europe, $340M Asia. EPS consensus $0.37, down 2.6% YoY, though the trailing 4-quarter average beat is 26.9%. FY2026 guide calls for organic net revenue +4-5%, gross margin roughly flat (150bps tariff headwind offset by pricing and product cost reductions), adj. EBIT margin expansion +40-60bps to approximately 11.8-12%.

Key watch: DTC channel mix and whether the 50% threshold is holding. The stock sold off 7% after Q4 despite beating on both lines, which reflects how sensitive the market is to any guidance softness. Any QTD commentary on March traffic would be valuable given what happened to consumer confidence after February 28.

March CPI (Friday April 10, 8:30am ET)

The first CPI to capture part of the energy shock. Brent moved from approximately $74/barrel to over $90 during the March survey window (late February through mid-March). Continuum Economics projects headline CPI +1.0% MoM, which would be the strongest monthly print since June 2022. Headline YoY is projected to jump to approximately 3.4% from 2.4% in February. Core (ex food and energy) is expected at +0.22% MoM, in line with February, with YoY nudging to 2.6% from 2.5%.

A core print at or below 0.22% MoM allows the Fed to maintain the transitory energy framing. A core print of 0.3%+ changes the rate path conversation and puts additional pressure on consumer discretionary multiples, which have already de-rated through March.

FOMC Minutes (Wednesday April 8, 2:00pm ET)

From the March 18-19 meeting, 18 days after the initial strikes and before the Strait closed March 4. Powell publicly flagged rising inflation expectations at that meeting. The minutes will show how much internal debate there was about whether to model the energy shock as temporary or sustained. Probably not a market-mover unless the committee was more hawkish internally than Powell’s press conference suggested.

Calendar