Ferrari: D(ep)rive to Survive?

F80 Backlog, Auction Data, Luce Launch, and What the 5% CAGR Guidance Is Implying

THE RESET

If you went back a year and described where Ferrari’s stock would be today, it would have sounded out of place. A 45% drawdown, trading at a 52-week low, following a stretch where it had become one of the more widely owned “quality compounders” across both institutional and retail circles.

That positioning was not without justification. At the 2022 Capital Markets Day, management guided to 9% revenue CAGR and 14% EBIT CAGR through 2026. Those targets were effectively achieved well ahead of schedule, reinforcing the idea that Ferrari could deliver both growth and consistency at scale.

The reset came in October 2025. Expectations were anchored to a continuation of that trajectory. Instead, management introduced a materially lower framework, guiding to roughly 5% CAGR across the P&L from 2026 to 2030. As Bernstein’s Stephen Reitman noted, the reaction in the room was one of surprise.

h/t @WTCM3 for the post and highlights

What makes the situation notable is not simply the change in guidance, but the contrast between that guidance and what is already visible within the product cycle. The business itself has not obviously deteriorated. The forward view, however, implies something closer to stagnation.

At higher multiples, that tension is difficult to underwrite. At current levels, it at least invites a second look.

THE F80 CONUNDRUM

What makes the guidance genuinely hard to accept is that a single car can single-handedly shift gears in the P&L profile, and Ferrari already knows it will deliver that car.

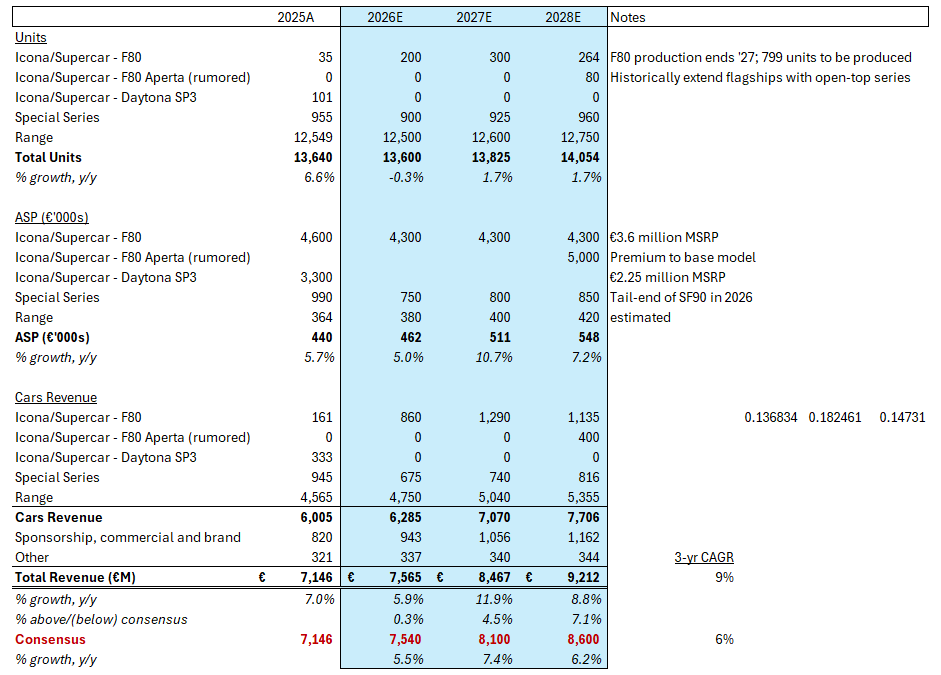

The F80 Supercar is priced at €3.6 million at list. All 799 units were spoken for before the exterior was publicly revealed. Ferrari delivered approximately 25–45 units in Q4 2025 (my estimate; the company described it as “the first few units” and declined to give a specific count) which means over 750 units remain to be delivered across a stated two-to-three-year window.

Personalization is a key monetization lever on every Ferrari, and more so on its Supercars. On a €3.6M Supercar with a client base pre-selected for both financial capacity and Ferrari loyalty, average realized ASP should comfortably clear €4.5M all-in.

Where the Icona and Supercar segment contributed approximately 9% of total Cars & Spare Parts revenue in 2025, it is likely to approach 15–20% in the 2027–2028 window at peak F80 delivery pace. The Range business sustains with the introduction and ramp of the Amalfi, 849 Testarossa and Spider, and Luce. Accounting for the SF90 XX tail in Special Series, the P&L is setting up to approach its 2030 revenue floor two years early, not dissimilar to what happened after the 2022 CMD.

And in a scenario where revenue grows HSD% annually the next few years driven by performance at the Supercar-level, the EPS growth profile should reach mid-teens %.

Published consensus for 2027 revenues sits at approximately €8.1B, only €550M above the 2026 estimate of €7.6B. At an estimated all-in F80 ASP of €4.5–5.0M, that €550M of incremental revenue would be broadly consistent with on the order of ~100–150 incremental F80-equivalent units. The implication is that consensus is embedding a relatively modest F80 delivery pace in 2027, likely not far above prior Icona peak levels, despite what should be the highest-volume delivery year of the program..

With ~750 units remaining over a two-to-three-year window, a delivery distribution of 200–250 units in 2026 (though near-term geopolitical risk puts ‘26 numbers at risk) followed by 300+ in 2027 is both historically plausible and implied by Ferrari’s own guidance language.

There are a few reasons why management might be conservative about the F80's production rate. The F80 will be the most produced Supercar outside of the F40, and producing at or above 300 units per year could prove challenging when simultaneously ramping a first-generation EV program. More importantly, the guidance may deliberately exclude the optionality of the F80 Aperta, a potential open-top variant, on the entirely rational basis that you cannot pre-announce a derivative of a car that is still in delivery.

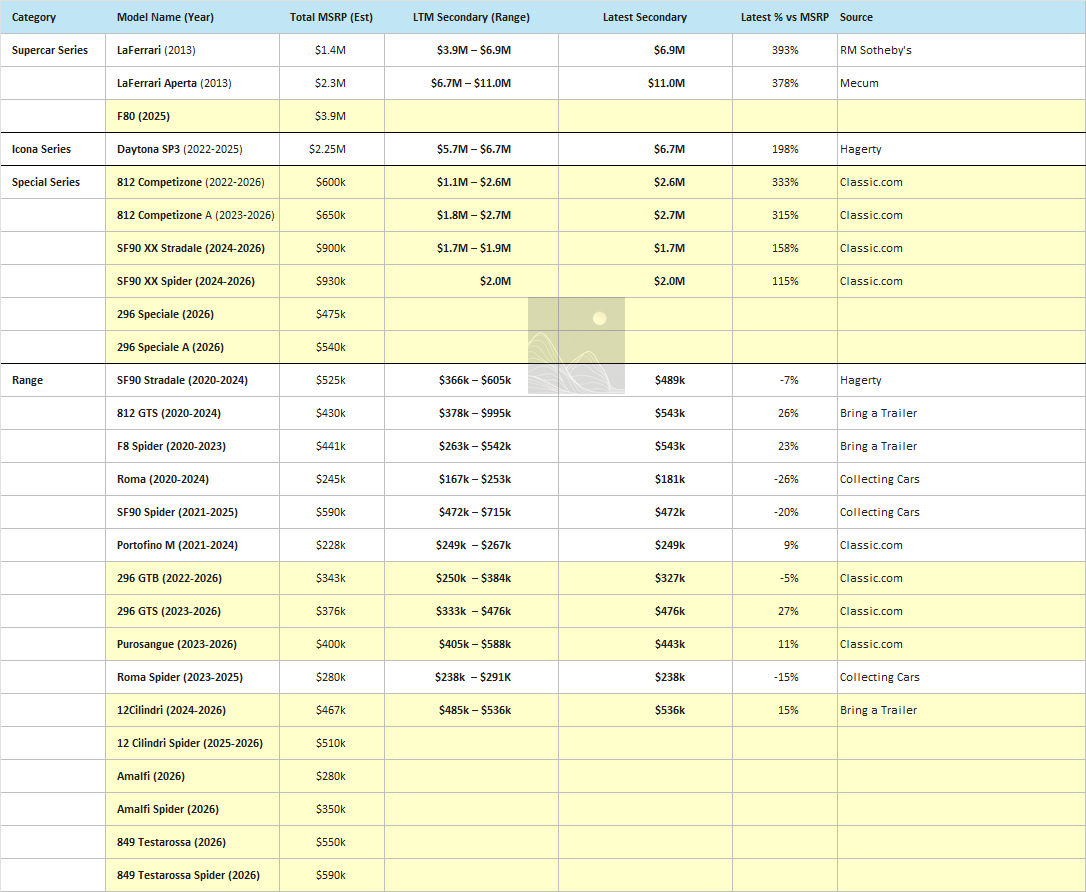

The Aperta is not a trivial option. Every open-top Supercar Ferrari has produced has commanded a significant premium over its coupe: the LaFerrari Aperta launched at roughly 40% above the coupe's base price, and today trades at approximately 50% above the coupe on the secondary market. Applying that to the F80: an Aperta variant would likely price at €4.9–5.0M base, with all-in realized ASP including personalization approaching €7.0–7.5M per unit. At 100–150 units (a production run that keeps the total F80 family well within the bounds of exclusivity, since each Aperta is generating the revenue equivalent of two coupe deliveries) that is €700M to over €1B of incremental revenue landing largely over a concentrated 1–2 year delivery window, from a car whose development cost is almost entirely already sunk in the coupe program.

Beyond the Aperta, the out-years carry a second option: a fresh Icona. Industry reporting suggests Ferrari may be developing an SP4 (likely V12-based, potentially a tribute to the F40 on its 40th anniversary) for the 2028–2030 window. That would be a new program at a new price point, not a derivative. If both happen sequentially, F80 Aperta in 2028 and SP4 in 2030, the Supercar and Icona tier sustains meaningful revenue contribution through the entire guidance period, which is precisely what the 2030 guidance's <4% Icona/Supercar mix target implies Ferrari is planning for.

DEPRIVE TO SURVIVE

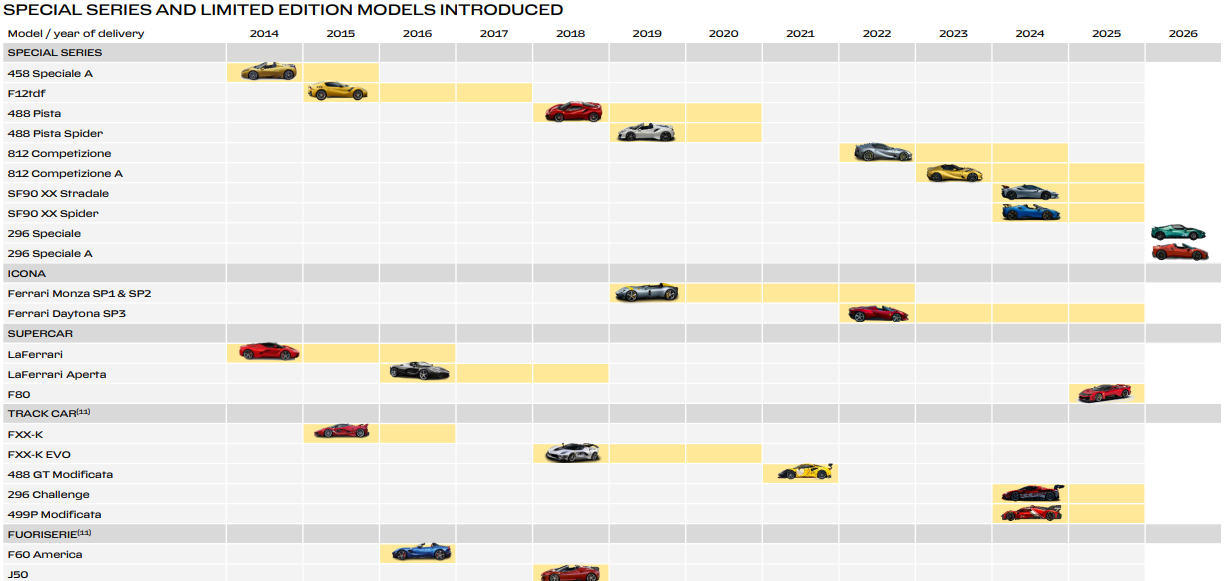

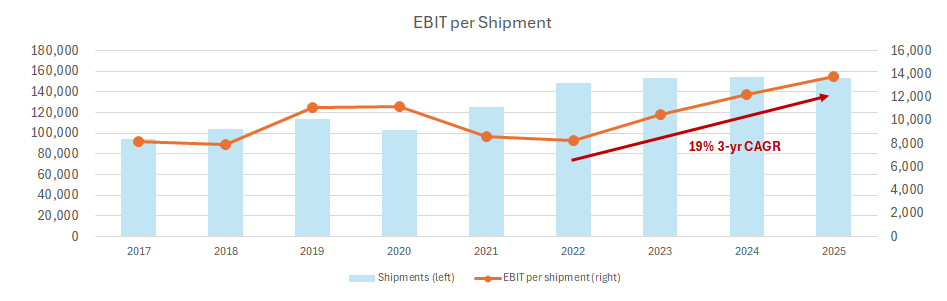

Ferrari is a Veblen good. These should be assets that appreciate. But looking line-by-line at the last five years of Range launches and comparing current secondary market values to list, they have been hit or miss.

The 812 GTS, F8 Spider, 296 GTS, and 12Cilindri have held their value well. The Roma, Roma Spider, SF90 Stradale and Spider, and 296 GTB have not. The Range models are a legitimate cause for concern, and the chart laying out realized secondary values versus MSRP makes it stark.

What might be the issue here?

It’s possible that a product decision aggravated this: the shift to haptic and digital steering wheel controls, which was enough of a customer backlash that Ferrari has since offered retrofit kits. The company acknowledged it. That kind of self-correction is healthy but the residual value damage on affected models has already been done.

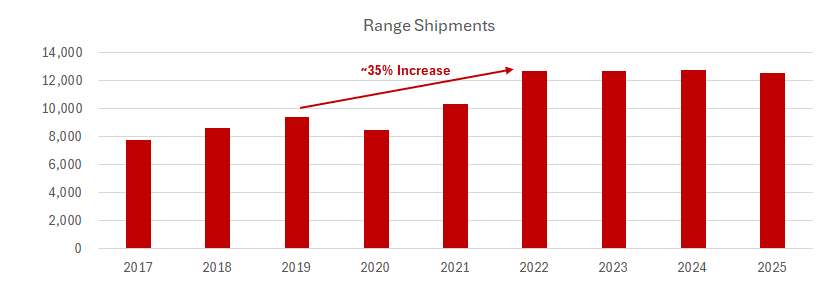

The simplest explanation is likely volume, though broader cooling in secondary luxury markets has also played a role. From 2017 to 2022, Ferrari delivered 60% more Range units annually. Supply caught up to and exceeded secondary market clearing demand on certain models. When that happens on a Veblen good, the feedback loop can be severe: depreciation discourages new buyers, who worry they will take a loss, which reduces demand further.

And while 2022 was a strong financial performing year with topline up 19% y-o-y (driven entirely by shipments growth) and EPS up 13% y-o-y, 2023 only had shipments up 3% but revenues, EBIT, and EPS were up 17%, 32%, and 36%, respectively. The profitability gains in 2023 were driven almost entirely by enhanced product mix (Daytona SP3, 812 Competizione and SF90 families) and country mix (the U.S.).

And the product actions Ferrari is taking suggest management understands the issues. The 849 Testarossa replaces the SF90 with a fresh platform and fresh allocation, resetting the depreciation clock. The Amalfi replaces the Roma with tighter initial supply. The Luce is explicitly production-capped at 20% of total output from day one. These are not coincidences, they are supply discipline responses to an oversupply perception problem. The constraint of today is what unconstrains the business longer-term.

GUIDANCE EX-LUCE CONTRIBUTION: “HEAD SCRATCHER”

Initially, the instinct when Ferrari disclosed its EV mix target was to back into the core ICE/hybrid business and find something compelling. The results were, if anything, more confounding than the headline guidance.

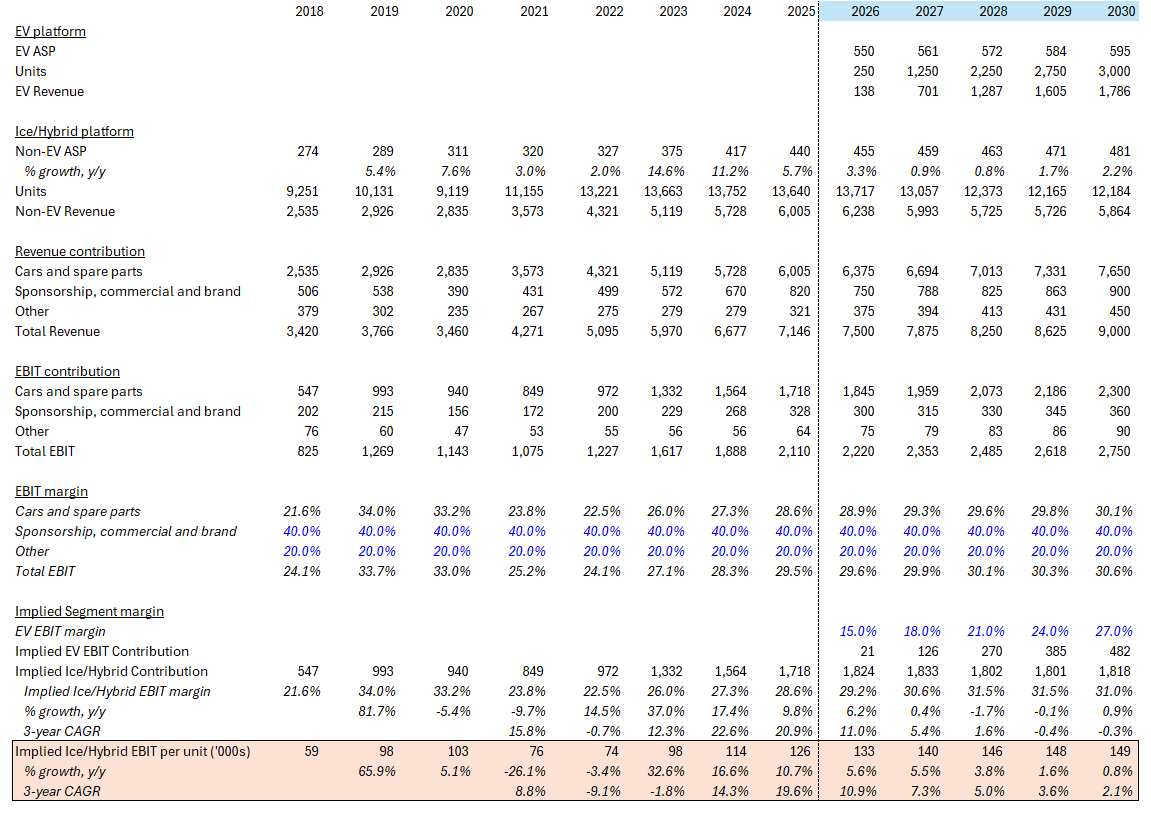

For a business that compounded revenue and EBIT per shipment at 7% and 11% annually between 2018 and 2025, the 2030 guidance implies that the core ICE/hybrid revenue and EBIT per shipment compound at roughly 2% and 3% respectively over the next five years. The guidance is effectively saying the core run-rate business, before any EV contribution, barely grows on a per-unit basis and basically flat on an aggregate basis.

This is almost impossible to reconcile with observable reality. Look at the 2023 to 2025 period: shipments were essentially flat across those three years, and yet per-unit profitability improved meaningfully, primarily through mix, not even straightforward price increases. The 812 Competizione, SF90 XX, and Daytona SP3 each generated dramatically more EBIT per unit than the Range cars they displaced in the delivery mix. The pattern is consistent and structural.

The company is about to embark on:

The largest Supercar delivery cycle in the modern era with the F80

The 849 Testarossa enters full run-rate deliveries as the highest-ASP Range car Ferrari has ever produced.

The 296 Speciale matures from launch-year minimal personalization toward peak personalization attach rates over 2027–2028.

The next Icona is presumably in development.

To believe that per-unit ICE/hybrid profitability would compound at only 2–3% annually through all of that, with a product cycle this favorable, requires assuming either severe cost inflation or deliberate sandbagging.

One important nuance: the EV margin assumption matters here in ways that cut in a counterintuitive direction. If Luce EBIT margins are lower than commonly modeled in the early years (and for a first-generation EV platform on a bespoke 880V architecture, producing 250–500 units annually, with full E-Building depreciation hitting from day one, margins in the 5–10% range in early years appear more realistic) then hitting the blended ≥30% EBIT target by 2030 requires the ICE/hybrid core to run at approximately 35% EBIT, equivalent to roughly 45% EBITDA. That would place Ferrari's combustion and hybrid business alongside the most profitable luxury goods franchises on earth, margins that have no precedent in automotive manufacturing at this volume.

LUCE: THE PUROSANGUE PLAYBOOK

When Ferrari revealed the Purosangue in 2022, the reaction from traditionalists was immediate and, in some cases, severe. A four-door, four-seat vehicle that was quickly labeled an SUV. The automotive press spent months debating whether the company had drifted from its core identity. Some longtime clients openly questioned their allocations. The language, at times, was unusually strong for a product launch.

A version of that response is beginning to take shape around the Luce. No internal combustion engine. A grand touring sedan, developed in collaboration with a former head of Apple design. A materially different proposition from anything Ferrari has produced historically.

The comparison to the Purosangue is useful, not because the products are similar, but because the initial reaction followed a familiar pattern. In the Purosangue’s case, early skepticism had little bearing on how the car ultimately performed in the market. The model was effectively spoken for before most reviews were published. Secondary market prices initially traded well above list. Waitlists extended meaningfully beyond initial deliveries.

That outcome was not driven by a broad shift in perception around what constitutes a “Ferrari.” It was driven by allocation. The company placed the car with a defined set of clients and maintained tight control over supply. Under those conditions, demand from within the existing client base was sufficient to absorb production and support pricing.

The mechanism is not entirely independent of the product itself, but it is heavily influenced by who receives allocations and how constrained overall supply remains.

There is, however, an important caveat. Secondary market premiums for the Purosangue have moderated since launch, with more recent transactions closer to list price than the levels observed in 2022 and 2023. Supply has gradually caught up with early demand. Ferrari’s 20% production cap allows for a meaningful number of units annually, and as allocations broadened, pricing normalized. This dynamic is closely related to the residual value concerns that have weighed on the stock the last couple years.

The early indications suggest a more measured approach with the Luce. Initial allocations appear to have been placed selectively, ahead of a full public reveal. Ferrari has also been explicit that electrification will be additive rather than a wholesale transition, with EV production capped at 20% of total output. At current volumes, that implies an upper bound of roughly 2,800 units annually at scale, with earlier years likely operating below that level.

There is also a practical constraint that did not apply in the same way to the Purosangue. The Luce will be produced within Ferrari’s new E-Building, which introduces an additional near-term limit on ramp capacity. While not necessarily a permanent constraint, it does suggest a more gradual increase in supply during the initial years of production.

The target customer base may also broaden at the margin. The Purosangue was largely directed toward existing clients seeking a more practical addition to their garage. The Luce appears positioned to appeal both to that same group and to a subset of buyers with a stronger orientation toward design and technology, some of whom may not have previously engaged with the brand. To the extent that incremental demand materializes alongside a controlled supply profile, the conditions that supported early Purosangue pricing could re-emerge.

The Purosangue provides a useful reference point, though not a guarantee. It demonstrated that, under the right supply conditions, Ferrari can introduce a product that initially sits outside traditional expectations without impairing demand. The Luce represents a second iteration of that approach, with tighter early supply and a different set of constraints. The initial setup appears supportive, though the outcome will ultimately depend on how closely supply discipline is maintained as production scales.

THE STOCK SETUP

The setup does not rely on a step-change in the business. It relies on a small number of assumptions that are each consistent with how Ferrari has operated historically.

First, that management is once again guiding conservatively. The 2022 Capital Markets Day targets were effectively treated as a floor and were reached ahead of schedule. The current framework is being presented in similar terms, despite a product cycle that appears at least as supportive.

Second, that the F80 program translates into reported financials on a timeline broadly consistent with what is already visible. The majority of the production run is pre-allocated, with deliveries concentrated over the next two to three years. That creates a period where mix alone should be sufficient to drive a meaningful step-up in revenue and earnings, even without relying on incremental volume.

Third, that recent actions within the Range segment are sufficient to stabilize residual values. The underlying issue does not appear structural, but rather a function of pacing and supply. Adjustments to future launches, alongside a more measured approach to volumes, would be consistent with how Ferrari has historically managed periods of imbalance.

Taken together, these are not particularly demanding assumptions. They do not require a change in demand, nor a departure from Ferrari’s established playbook. They require execution and a degree of discipline around supply.

At the same time, the risks are not difficult to identify. The multiple can compress further, particularly if near-term estimates move lower or if macro conditions weigh on deliveries and mix. Ferrari has not been immune to those pressures in prior cycles.

What has shifted is the balance between those risks and the embedded expectations.

Following the recent drawdown, the current valuation reflects a more cautious view of both growth and profitability. If the next several years develop in line with the existing product cycle and backlog, the direction of estimate revisions is more likely to be upward than downward.

Ferrari at these levels is not obviously inexpensive. It is, however, closer to a point where the forward setup begins to look more favorable than it has in recent years.