From Trail to Street: Salomon's Second Act

Long: Amer Sports, Inc. (NYSE:AS), 12-month Target of $45.00, or ~39% upside

Salomon is a 75-year-old brand that started in the French Alps as a ski equipment manufacturer. Over time, it has evolved into one of the leading brands in trail running and hiking footwear. If you’re looking for a technical, durable shoe to carry you through the trails (and you rely on reviews and trade publications to guide the decision) there’s a good chance Salomon shows up near the top of the list.

While the brand’s heritage sits firmly in trail and hiking, Salomon has expanded into adjacent categories like gravel and road running as well as Sportstyle. Sportstyle is essentially the brand’s lifestyle expression, taking the same technical design language and bringing it into everyday wear.

What makes Salomon particularly interesting right now is the trajectory of the Sportstyle subsegment:

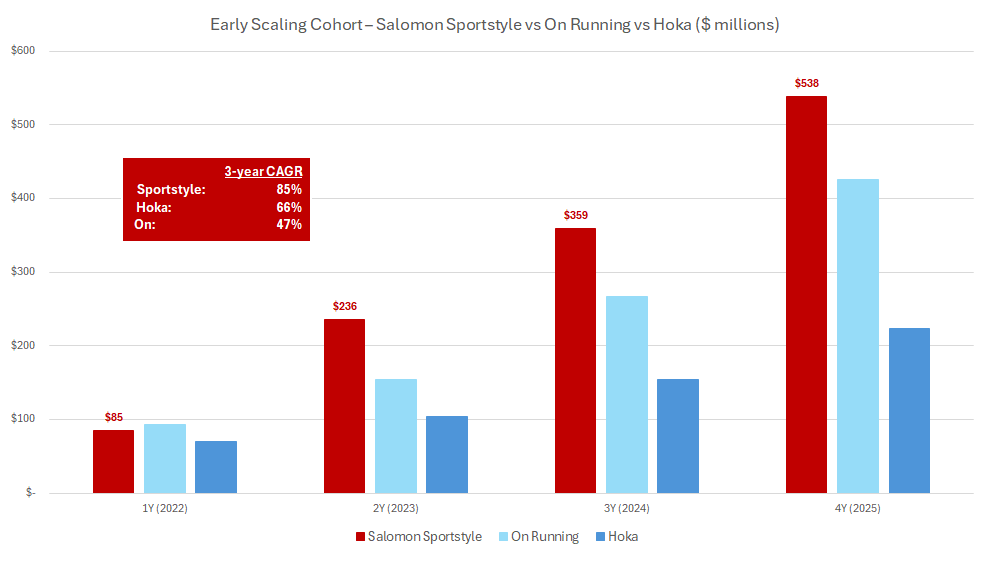

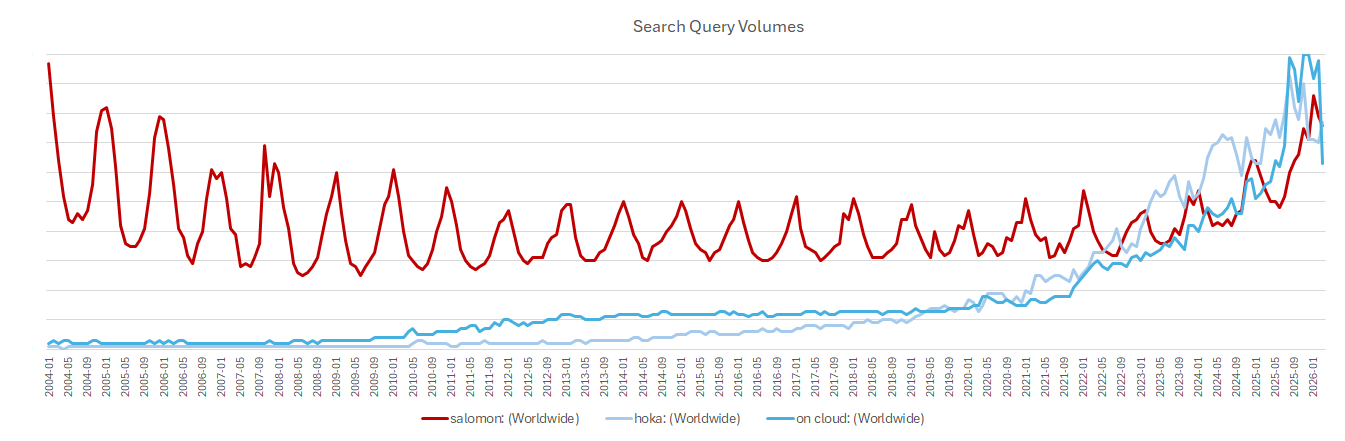

The chart below helps visualize the point. When we line up the early scaling of Sportstyle against Hoka and On, starting from a similar ~$80 million base, Salomon’s ramp stands out: Salomon’s Sportstyle is tracking ahead of both Hoka and On at a comparable point in their development.

That’s notable because Hoka and On are widely viewed as two of the most successful footwear launches of the past decade. Yet Sportstyle appears to be scaling at least as quickly and with far less global distribution than those brands had at similar stages.

The trajectory suggests Sportstyle could evolve into a meaningful growth engine within Salomon rather than simply a niche lifestyle offshoot.

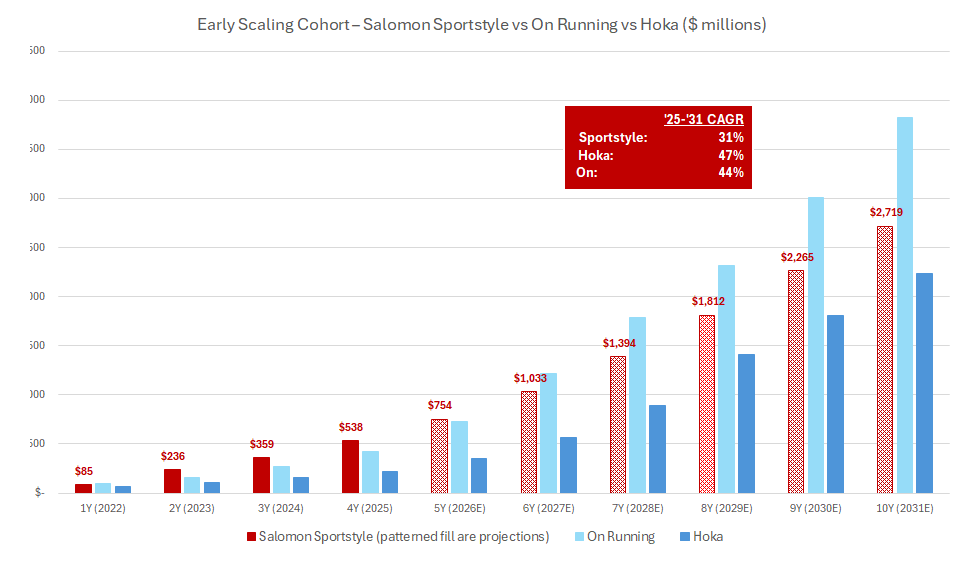

Even if we assume Sportstyle’s 2025-2031 CAGR settles at 31 percent (meaningfully below Hoka and On’s historical 4Y-10Y CAGR of 47 and 44 percent, respectively), we’re in the realm of possibility of Sportstyle nearing $2.5 billion of revenue by 2030, which of course is a very long ways away. Still, it’s a tantalizing possibility and one that investors should keep track of (Sportstyle needs to track towards $750 million by end of ‘26) over the course of this year.

So how has Sportstyle scaled this quickly?

A big part of it is that Salomon didn’t set out to build a lifestyle sneaker from scratch. The core models, collectively the XT platform with the XT-6 leading the way, were already established technical products with credibility in trail running and mountain sport. When fashion began pulling the silhouettes into everyday wear, Salomon was effectively starting with a product that already had performance legitimacy and a distinctive design language.

From a 2019 GQ feature:

“For me, it was exactly the same sensation as the first time [Nike design legend] Tinker Hatfield decided to open the sole to show the Air,” Steinmetz says of his first encounter with a pair of Salomon runners. “It was something new, and it was something that took time to be completely understood by everybody, but it created a reaction.”

What did the XT-6 unlock that previous Salomons couldn’t? A near-perfect balance of accessible design and practical performance. In an era when labels like Balenciaga and Versace balloon their sneakers to gargantuan sizes in the name of fashion, a clean-lined, purpose-built shoe like the XT-6 felt like a revelation. “It’s the perfect aesthetic to touch everybody,” Steinmetz explains. “[My father] likes them to work in the fields, but also cool kids love them.”

In a market that’s so often driven by hype and exclusivity and the hot new thing, the fact that a seven-year-old sneaker that can take you from a night out in New York to a run through the Alps and back again—a shoe that looks good on dads and rappers alike and is widely available to everyone—was able to cut through all the noise is something worth celebrating. And so we’re doing exactly that. Ladies and gentlemen: the Salomon S/Lab XT-6 LT ADV, your 2019 GQ Sneaker of the Year.

Distribution also played a role. Early adoption came through fashion-forward boutiques and specialty retailers rather than traditional sporting goods channels. That helped seed the brand in style-conscious communities and allowed the product to travel organically through streetwear and editorial channels before it reached broader distribution.

Put together, Sportstyle benefited from a somewhat unusual combination: authentic performance roots, a silhouette that felt visually differentiated from mainstream running shoes, and early validation from fashion retailers. That mix allowed the category to scale quickly while still maintaining the perception that the product was discovered rather than manufactured for lifestyle from day one.

The natural question that follows is how durable this demand really is.

Sportstyle clearly benefited from fashion discovery, which raises the risk that some portion of the growth is tied to trend cycles. Trail silhouettes and technical outdoor gear have been a major part of the “gorpcore” aesthetic over the past several years, and if that trend fades, some of the lifestyle demand could soften as well.

That said, there are a few reasons to think the opportunity may prove more durable than a typical fashion cycle. First, the product itself is grounded in real performance footwear rather than a purely lifestyle design. Second, Salomon’s visual identity (Quicklace, aggressive tooling, technical overlays) is fairly distinct from the broader running category. And finally, the brand is still relatively underpenetrated in global lifestyle footwear, which suggests there is room for the category to grow even if the fashion tailwind moderates.

In other words, while some of the early adoption likely came from fashion trends, the brand may now have enough product credibility and distribution momentum for Sportstyle to evolve into a more structural growth driver rather than a short-lived style moment.

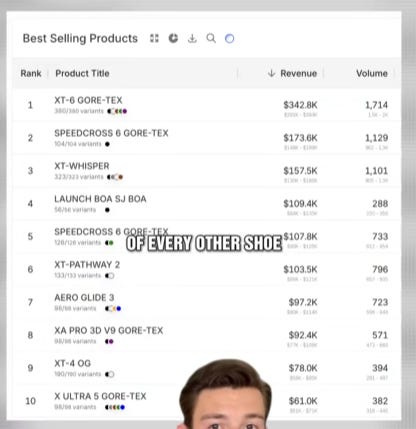

And beyond the XT-6 hero product, Sportstyle has been doing a credible job in diversifying into new models, which substantiates the XT platform as a legitimate growth vehicle going forward. Below we see a screenshot and TikTok video from Particl, an e-commerce competitive tracking tool, showing that the newer XT-Whisper holds its own as a top-3 best selling Salomon footwear product along with the XT-Pathway 2 and XT-4 OG contributing solidly as well.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

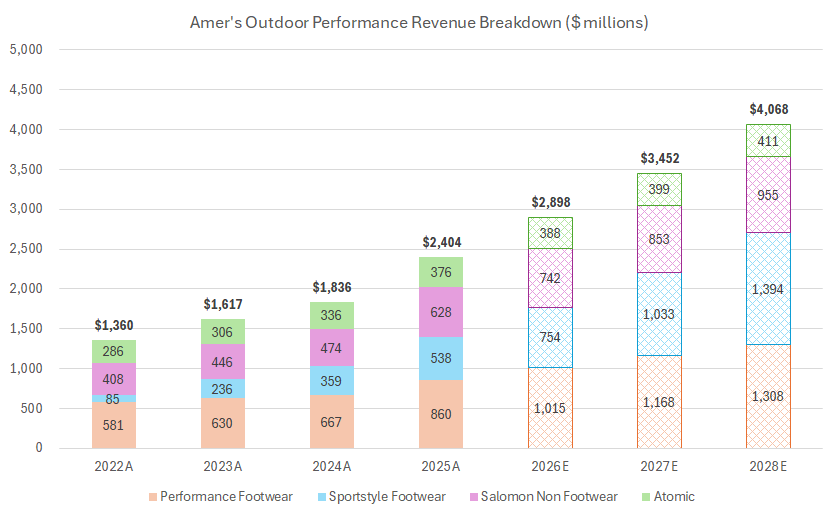

Even before taking Sportstyle into account, Salomon’s core Performance footwear division saw a marked upturn in its business through 2025. Salomon’s performance footwear business has historically been driven by the brand’s technical credibility in trail and mountain sport, alongside DTC expansion and strong growth in Asia. Through 2024 and into early 2025, management still described Sportstyle as the leading driver of footwear growth, even as performance lines were starting to build momentum.

What appears to have changed in 2025 is that performance running became a much more meaningful contributor in its own right. Management specifically called out Aero Glide 3 as one of the best footwear launches in Salomon’s history and said the new GRVL franchise was helping unlock the run category “like never before.” By the back half of 2025, Salomon was also seeing traction in the run specialty channel in North America and EMEA, while even China was beginning to show stronger demand for Performance products, which is a positive sign of growing brand awareness and cross sell as a primarily Sportstyle geography.

So relative to prior years, 2025 looks less like a story of Sportstyle carrying the entire footwear platform and more like a year where the performance side began to inflect as a real second growth engine, which is a real feat as the Performance division will likely surpass $1 billion in sales this year.

With evidence of category expansion beyond trail/hike and with planned channel expansion, Salomon’s footwear business legitimately has a shot at becoming a $2.5+ billion franchise in a few years:

As someone based in the U.S., there was skepticism about Salomon as a brand and how far reaching it could possibly be. But doing some quick Google trends searches and it’s easy to see that ex-U.S., the brand has a wide and growing presence. It was potentially a brand that stagnated, as it did for much of the 2010s, but Amer’s investment into Salomon’s footwear business has allowed awareness to compete with the best of them and to accelerate in recent periods.

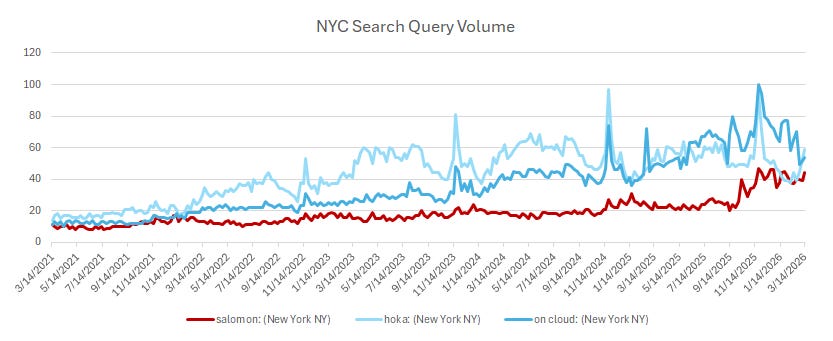

While the brand itself had been quietly establishing itself state-side, when we look at the U.S. search trends as whole, Salomon is still 25 percent of Hoka and On’s levels. But the market here is still so nascent, that it’s more appropriate to look at key landing zones like NYC to get leading indicator of demand. In the case of NYC, we’re looking at Salomon nearing parity with the leading disruptive footwear brands.

The most recent period of U.S. search acceleration was likely due to a confluence of events:

Fall 2025

Shoe collaborations

Feid (the Colombian artist known as Ferxxo) x Salomon XT-Pathway 2

MM6 Maison Margiela x Salomon XT

Celebrity

Jennifer Lawrence was frequently photographed by paparazzi in New York City wearing the Salomon XA Pro 3D

New Footprint

Opened new key locations in Williamsburg, Brooklyn (the heart of U.S. lifestyle trends) and Woodbury Common (a high-traffic premium outlet)

And there is clear opportunity for retail expansion in the U.S.:

This has obviously not gone unnoticed by the Salomon team. Last week (first week of March 2026), the team brought on Laura Stauth as SVP of Sales to drive the specialty run and wholesale strategy in North America. In her prior role at Vans, she grew wholesale doors by 2x to the mid-single digit thousands globally as well as brokered relationships with larger U.S. retailers such as Dick’s, which could potentially come in handy with the new Salomon role down the line.

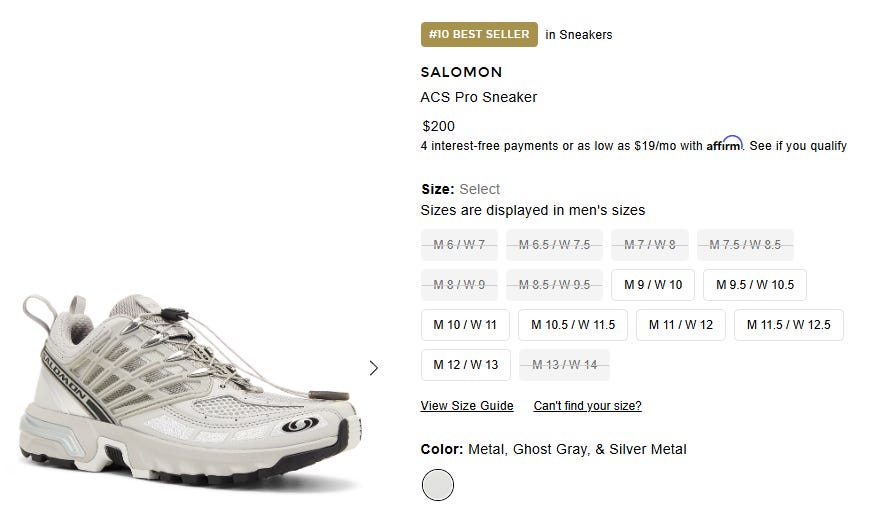

From a product perspective, we can see that Salomon and its newer products are showing up well in the marketplace. Salomon’s newly relaunched ACS Pro, is the #10 best selling sneaker on FWRD, and it’s the only $200 sneaker in the top 25. The ACS Pro is another example of the Sportstyle business extending beyond the XT-6 franchise.

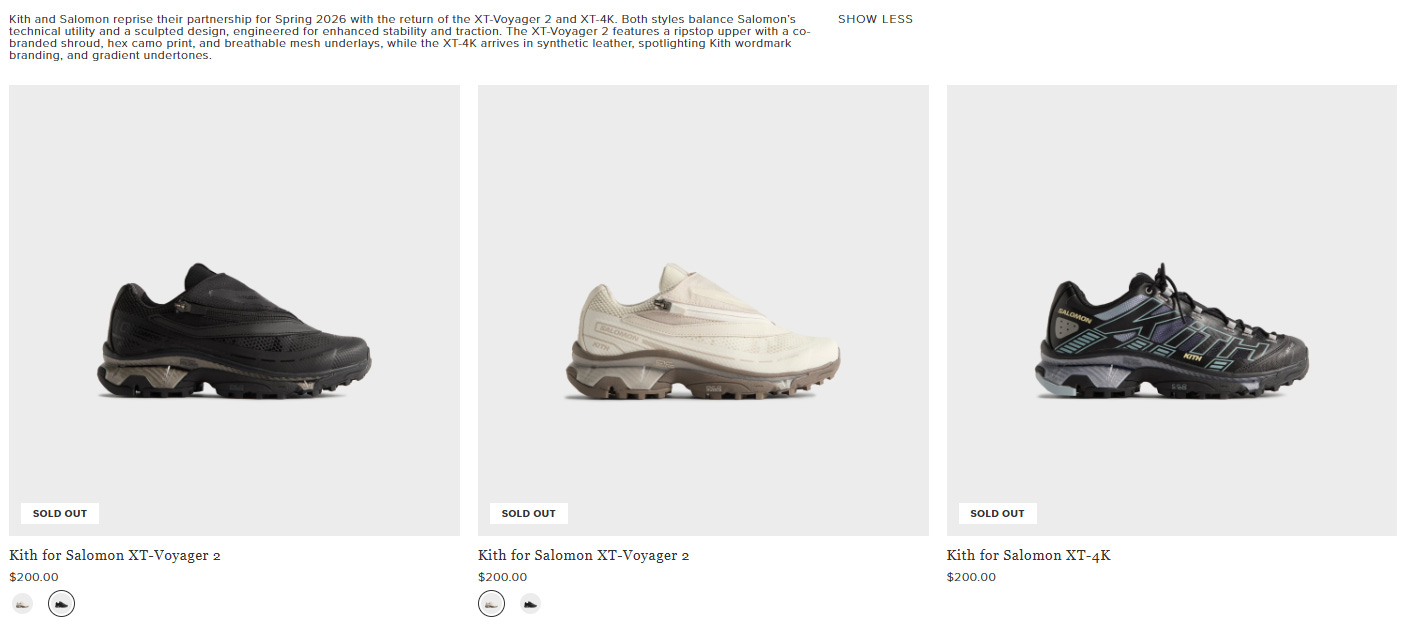

It also appears that the strategy to elevate the brand from a fashion perspective remains intact. We see the Spring 2026 collection Salomon launched in partnership with Kith below, and it appears the collection is already sold out.

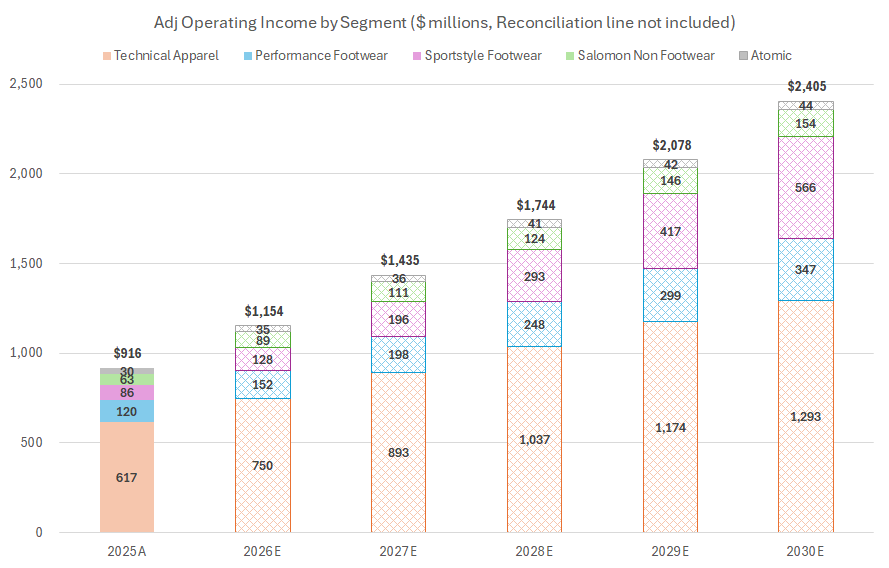

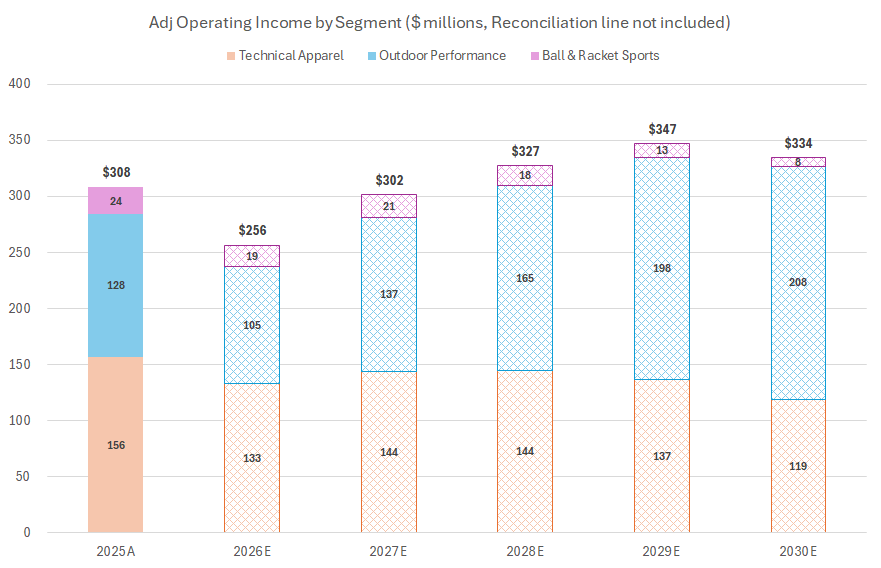

So, what can this mean from a profitability perspective? A couple charts provided below sketch the potential opportunity at the operating income level. While I’ve provided precise numbers, this is mainly a directional exercise, and the findings are that Salomon becomes the primary profit driver of the business within a few years, provided that the footwear business expands in a manner consistent with the growth profile of its peers (I know, it’s a big if).

Directionally, the overall Amer Sports business will generate an incremental $300 million of EBIT per year, and Arc’teryx and Salomon will contribute near 50/50 in the next couple years and will likely weigh 40/60 in subsequent periods.

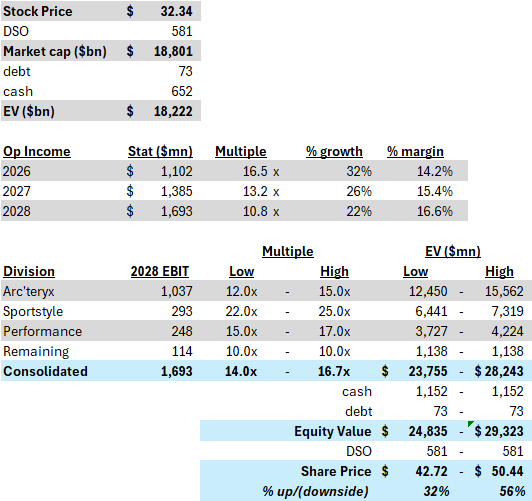

Looking at the entire Amer business from a valuation perspective, it’s clear that the asset is valued at a premium. What you need to believe is that both Arc’teryx and Salomon are still early on their execution path, and with Salomon, you need to believe in more open-ended growth for the Footwear business and particularly on the Sportstyle side. The checks and analysis provided in this and the prior post suggest that the two businesses are capturing share against legacy competitors as well as taking share in new adjacencies.

Currently, the asset is worth 16.5x ‘26 EBIT or ~11x ‘28 EBIT, based on my estimates, which are generally 20-25 percent higher than street. I think there’s a distinct possibility that the ‘28 EBIT multiple can graduate closer to 14x, as this level would put it closer on par with a quality growth asset like On. From a recommendation standpoint, while the table below shows a range of upside from 32 to 56 percent from current levels, as we’ve seen how 2026 has progressed, it’d be wise to layer in a healthier dose of conservatism into these numbers. As such, we’re probably closer to 30 to 40 percent of upside in the next 12 months, which is good, but I’m sure there are better ideas out there. This is probably a starter-to-lower sized position at this point. That said, if there’s further evidence of Sportstyle progress or if the core Performance footwear business starts seeing success in its GRVL/run franchise, the upside calculus can probably go north from where I’ve laid it out below.

Stepping back, the Salomon story increasingly looks like one of brand rediscovery rather than brand creation. The technical credibility and product DNA have existed for decades, but the combination of Sportstyle adoption, expanding footwear distribution, and renewed investment under Amer has unlocked a much larger market than the brand historically addressed.

What makes the situation interesting today is that the growth engine is no longer singular. Sportstyle appears to be establishing itself as a durable lifestyle franchise anchored by the XT platform, while the Performance side is beginning to reaccelerate with launches like Aero Glide and GRVL and improving traction in run specialty channels. If both sides of the footwear business continue to develop simultaneously, Salomon’s addressable market expands well beyond its traditional trail running niche.

For investors, the key variable to watch over the next 12–24 months is simple: whether Salomon can convert its rising brand awareness into broader footwear distribution and sustained sell-through across multiple silhouettes. If Sportstyle continues diversifying beyond XT-6 and the Performance running category gains traction in North America, the footwear segment has a credible path to becoming a multi-billion-dollar franchise.

That outcome is far from guaranteed, and the stock already embeds a meaningful amount of optimism. But if Salomon executes even moderately well against that opportunity, the earnings power of the broader Amer portfolio could look meaningfully different several years from now. At current levels the setup probably warrants a measured position rather than an aggressive one, but it is clearly a story worth following closely as the next phase of Salomon’s growth unfolds.