LOCO: Initial Work on a Potential Inflection

Encouraging early signals, though durability and portability remain open questions

SITUATION OVERVIEW

Your PM sees $LOCO up following its latest earnings print and asks for a quick read on whether the move is supported and worth further work.

Much of the buyside process is iterative, advancing the ball rather than underwriting a full position upfront. This note is meant to establish an initial view on the setup, highlight what appears to be working, and frame the key questions that would justify a deeper dive.

VALUATION / SETUP

ASSESSING WHAT HAPPENED

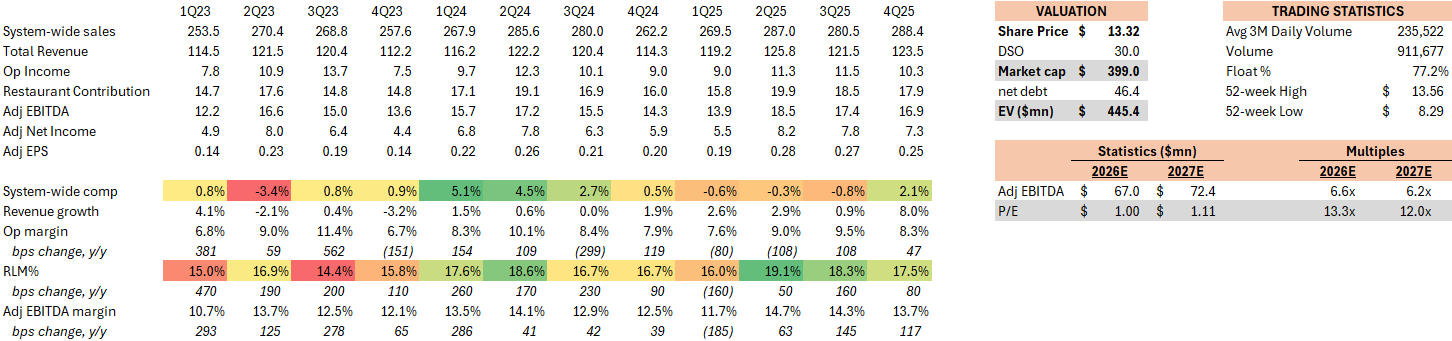

Restaurant stocks are largely driven by same-store sales (SSS), both in the reported quarter and implied forward trajectory.

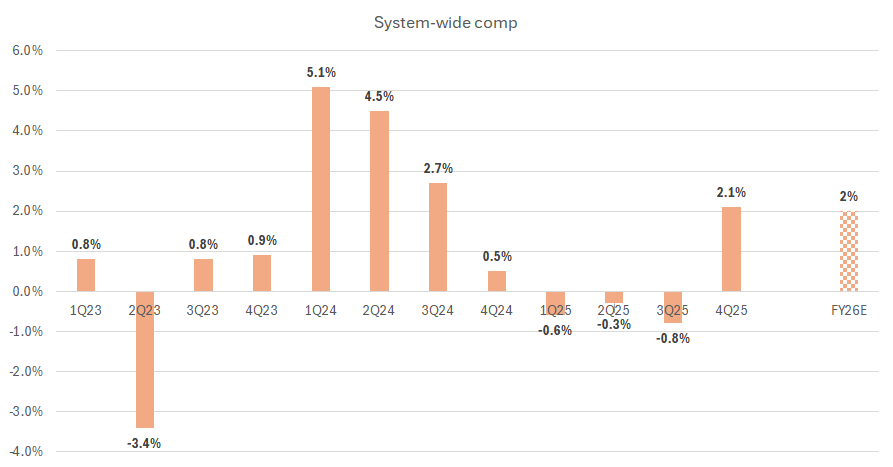

LOCO reported +2.1% comps, an improvement from -0.8% in the prior quarter (against an easier base).

Here’s the breakdown of the comp, below.

The company-operated comparable sales increase consisted of a 2.7% increase in average check size, partially offset by a 2.3% decline in transactions….

The 3.3% increase in comparable franchise store sales consisted of a 2.5% increase in average check size and a 0.8% increase in transactions.

Importantly, the composition of the comp remains skewed:

Check growth: +2.5–2.7%

Transactions: flat to negative (company stores -2.3%, franchise +0.8%)

This suggests the inflection is primarily mix/check-driven rather than traffic-led, which is directionally positive but not yet indicative of a broad-based demand recovery.

Management attributed much of the improvement to recent menu innovation, particularly higher-protein, value-oriented offerings.

Before I discuss how we capitalize on this opportunity further in 2026, I want to take a moment to celebrate the success of our Street Corn Double Chicken and Queso Crunch Double Chicken Burrito Bowl that we launched in late September. These bowls were instrumental in driving our fourth quarter performance, exceeding our expectations in both guest response and sales contribution. The popularity of these hearty, value-driven, high-quality offerings was so positive that we made the strategic decision to keep both bowls as permanent menu items.

(Liz Williams, CEO)

WHAT WE’LL NEED TO ASSESS

The key question is whether LOCO can transition from check-driven stabilization to traffic-driven growth, supported by:

Sustained innovation (pipeline depth and repeatability)

Incremental traffic drivers (e.g., Loco Tenders)

Expansion outside California (longer-term growth lever)

LOCO doubling down on more innovation to start off 2026:

Turning to 2026, we are pleased with the momentum from our Double Pollo Salads that launched in January with fresh options to meet new year resolutions. Featuring Street Corn, Mexican Caesar, and Bacon Ranch options, each salad delivers over 50 g of protein with a double portion of our signature fire-grilled chicken…Building on our salad success, in mid-February, we launched Baja Double Tostadas, reimagining our beloved tostada with bold new flavors and notably a seasonal seafood option.

Launched a Protein menu to capture demand from a macro trend, but with no operational enhancement required as it was more of a packaging maneuver to highlight menu items they already had:

Turning to protein, we are proud of our position as a true protein leader. We further capitalize on the macro trend by launching our version of a protein menu, which is a collection of menu items with more than 20 g of protein.

Also discussed future innovation pipeline:

Loco Tenders (final stages of preparing for this launch; tested in stores)

Loaded Quesadillas

Crispy Grilled Chicken Sandwich (that delivers crunch and flavor of a fried sandwich)

Horchata Ice Coffee

Cold Foam Coolers

Accelerating unit development outside of CA:

These second-generation site construction costs were typically in the low- to mid-million-dollar range, and all have been averaging above $2 million in annualized sales volume. These successes reinforce our confidence as we look toward 2026, where we are targeting approximately 18-20 new restaurant openings, with three to four being company-owned locations. Similar to last year, the vast majority of the 18-20 new openings in 2026 are expected to be outside of California.

My take: there’s always a million things thrown at you during an earnings call, but the (1) innovation pipeline and (2) the ex-CA unit development step up are the two initiatives that stand out.

CHANNEL CHECK: INNOVATION PIPELINE

Game plan: find which stores tested the Loco Tenders, call them, just get a general sense of how the tests went / are going.

Which stores? We can see them here in this local SoCal article, which highlights 20 locations. Called 11 of them and got through to 9.

Some operators are chatty, some are not, but basically you’re trying to hang around the hoop until it’s uncomfortable asking them how a test went, what attach rates were, how many customers were new because of the tests, etc. You’ll only get so much information, but if you have no credit card data, this is still informative. I focused on the Loco Tenders, as it was the most active test across the units.

Lake Forest: 21212 Bake Parkway

Only sold them for a limited time, test has stopped since

Have a lot of people asking for them even today

Test was very popular

Costa Mesa: 3131 Harbor Blvd

Test was for only a limited time, hard to remember as it’s been 3-4 months but think it was popular

San Clemente: 963 Avenida Pico

Tenders were really popular, was a very successful test

Kids in particular really liked them

But not sure if the tenders will come back on the menu

San Juan Capistrano: 33953 Doheny Park Road

Test didn’t go well actually and don’t think the tenders will come back on the menu

Why? Just didn’t sell well, not sure, was not popular

Mission Viejo: 25110 Marguerite Parkway

Tested here for a bit but it’s at other stores now - Lake Forest and Rancho Santa Margarita

Still have people asking for the tenders so it was quite popular

Tustin: 13421 Newport Ave.

Testing now, but don’t think it’s going well, don’t have a lot of people buying them

Brea: 2500 E. Imperial Highway, Suite 186

Tenders did not sell well, we don’t carry them anymore

You’re the only person who’s asked about them actually

Garden Grove: 12909 Harbor Blvd.

Tested but not sure if they’ll come back, haven’t heard anything from management

The tenders were ~kinda popular but they weren’t selling the most

Top 10 item? No wouldn’t have been in the Top 10

Santa Ana: 1702 E. 17th St.

Had the tenders as part of test, not selling them anymore

Decent amount of people bought them

While the sample is limited, ~5 of 9 stores described the tenders test as at least moderately successful, with several noting continued customer inquiries post-test. If we spend more time and are able to extrapolate the findings, could be more informative. If even half the store base sees the tenders doing well, you’d consider that a success.

Based on these conversations, tenders appear capable of driving incremental traffic, potentially skewing toward younger customers, with an estimated +4–6% uplift in test stores, translating to ~2–3% system-wide SSS upside if broadly rolled out. This is even before layering in other innovation items like the Crispy Grilled Chicken Sandwich, that supposedly tastes like a fried on. I haven’t seen the sandwich in the wild, but this SKU concept intuitively sounds like it can be incremental.

That said, it remains unclear whether this reflects sustained demand or initial trial, and repeat behavior will be a key variable to monitor.

CHANNEL CHECK: PRICING ARCHITECTURE AND COMPETITION

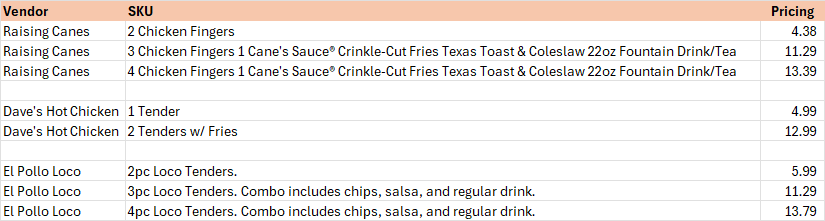

As only the Tustin, CA location was still doing the active test, I looked for concepts that are active in the chicken tender space within a couple mile trade radius:

It’ll be interesting what the final pricing architecture will be at launch as it doesn’t look like they’re trying to be actively competitive in the trade area. I’ve tried the Loco Tenders and they run slightly smaller than Raising Canes and much smaller than Dave’s, so I don’t believe they’d win on a $/oz perspective either. This is a test after all, so I don’t think we should be reading too much into it. What the tenders do help with is highlight the rest of the LOCO menu, which is highly competitive on value.

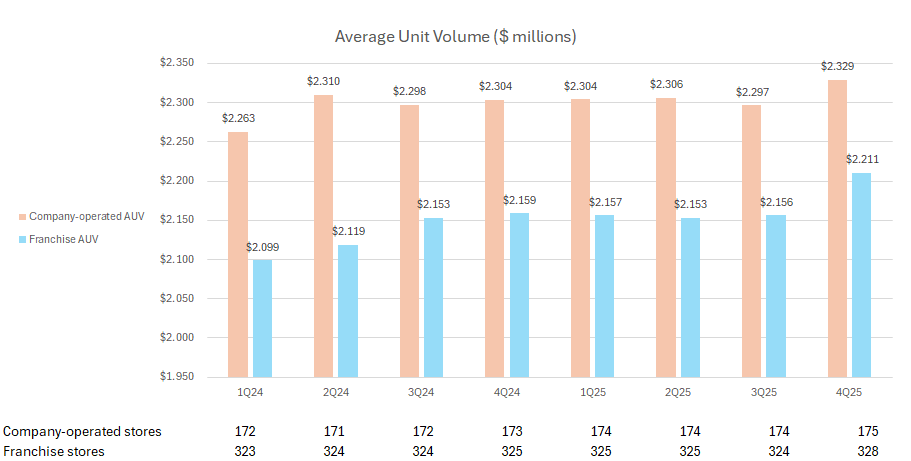

AVERAGE UNIT VOLUME TRENDS

Before the company embarks on an accelerated path to build stores outside of California, it’s important to assess whether the latest units have been productive. While the numbers below are shown on a net basis, there have been changes at the gross level, and the overall AUV trends indicate an increasingly healthy store base.

STORE EXPANSION OPPORTUNITY

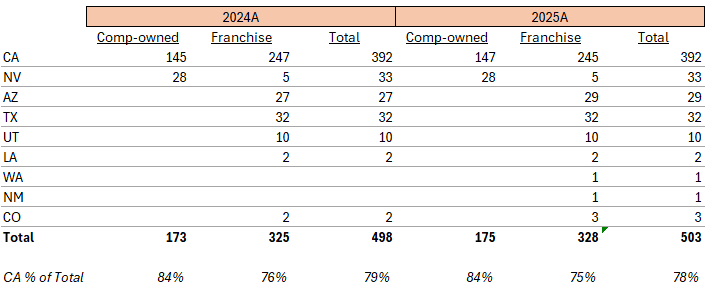

With ~80% of the store base concentrated in California, LOCO’s ability to scale meaningfully depends on expanding outside the state. Notably, ~70% of new units over the past two years have been built ex-CA, reflecting a clear strategic shift. Until this geographic mix becomes more balanced, the concept is likely to carry a “regional” discount.

Encouragingly, AUVs have improved over the same period despite the majority of development occurring in newer markets, suggesting early evidence of concept portability. If sustained, this should support continued acceleration of unit growth outside California.

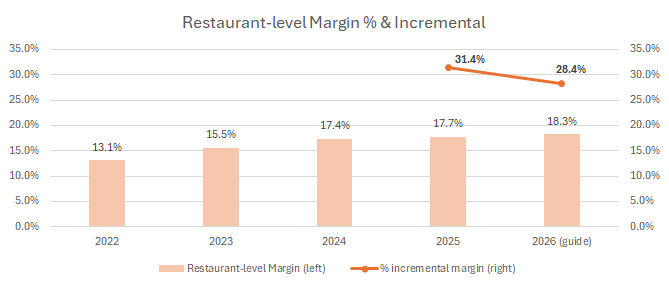

After having stood up 9 new stores last year, they’re guiding to 18 to 20 new stores for this upcoming year. The reason for the confidence is that they’ve successively improved the unit level economics starting in 2024 and they’ll be launching the latest prototype for this year. Here’s that discussion in the 10-K:

We believe that creating strong margins is as important as driving topline sales. In 2024 we launched a concerted effort analyzing our product offering, labor, and controllables to determine areas of opportunity. Through this effort, we identified several workstreams to optimize product costs, supplier efficiencies, and labor deployment. While some of the savings were realized in 2024 and 2025, we believe that these initiatives will have a positive impact on overall profitability for future years as well.

In addition to managing cost of sales and operating expenses, we believe that a cost-improved restaurant prototype is critical to enhancing returns and supporting disciplined growth. Cost optimization efforts related to furniture, fixtures, and equipment (“FF&E”), layout, materials, and design standards were initiated at the end of 2024. Identified savings – particularly within FF&E – have been incorporated into new restaurant builds beginning in 2025. The full next-generation prototype, inclusive of identified cost savings to date, is expected to open in 2026.

A simple per capita framework highlights the potential opportunity: while California and Nevada operate at ~10 stores per million people, Texas (~1 per million) and Arizona (~4 per million) remain significantly underpenetrated. Even applying a discount to California-level density, Texas could support a store base several multiples of its current footprint, with Arizona still offering meaningful whitespace.

The key question is whether LOCO can replicate its unit economics outside its core market. If so, unit growth becomes a more durable and less cyclical driver of earnings.

The company is guiding to ~18–18.5% restaurant-level margins in 2026 (vs. 17.7% in 2025), implying ~28% incremental margins on top of ~31% in the prior year. If sustained, this suggests attractive returns on incremental units, particularly in lower-cost geographies outside California, supporting continued reinvestment in new store development.

SOCIAL / ALTERNATIVE DATA

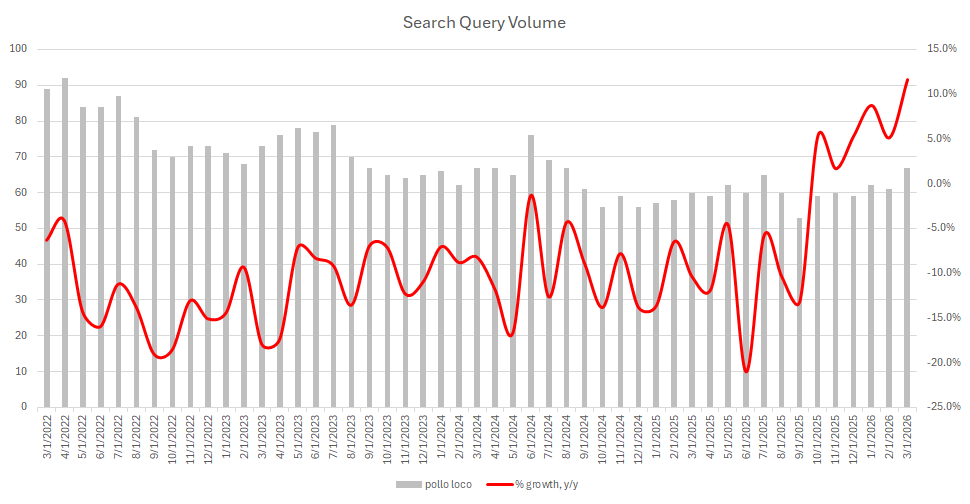

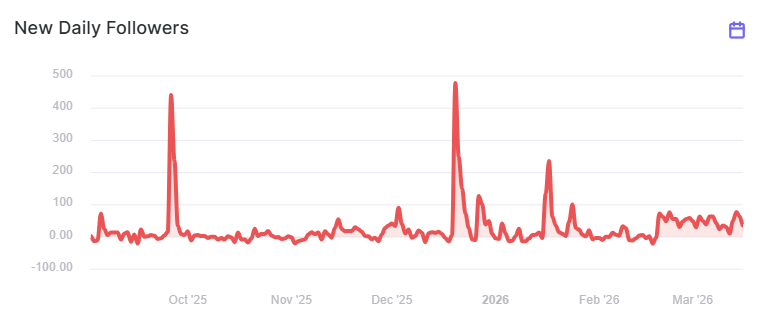

Search interest for “pollo loco” has inflected meaningfully since late 2025, while social engagement (e.g., Instagram follower growth) has remained consistently positive.

Their Instagram page has also been consisting adding net new followers (area under the curve but above 0), which is a positive sign. There’s been sustained strength in the last 30 days.

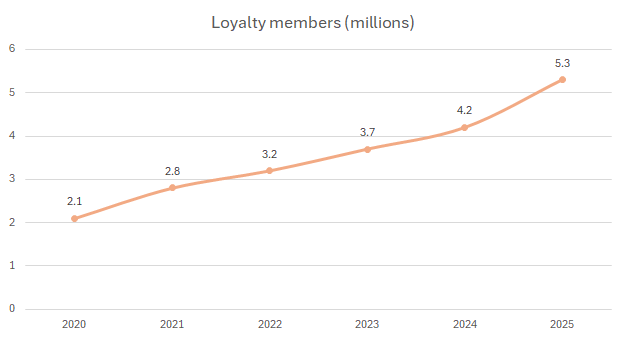

The company’s focus on digital initiatives is seen clearly in the momentum of the Loco Rewards loyalty program, which saw an acceleration of signups in 2025:

While imperfect, these signals are directionally consistent with improving brand awareness and recent product traction.

PUTTING IT ALL TOGETHER

The post-earnings move in LOCO appears to be grounded in a modest but real comp inflection, driven primarily by mix (check growth) and supported by early success in menu innovation. While transaction trends remain mixed, the pipeline (particularly Loco Tenders & potentially the Crispy Grilled Chicken Sandwich) offers a credible path to incremental traffic, with channel checks suggesting potential low- to mid-single-digit SSS upside if scaled.

More importantly, the longer-term opportunity is increasingly tied to unit growth outside of California. With the store base still heavily concentrated in-state, LOCO remains underpenetrated in newer markets despite a clear shift in development strategy. Encouragingly, AUV trends and restaurant-level margins have held or improved despite this shift toward newer markets, suggesting early evidence of concept portability. Combined with structurally lower cost environments outside CA, this raises the possibility that incremental units may generate attractive returns, supporting management’s confidence in accelerating development.

Taken together, this is not yet a clean, traffic-led recovery story, but rather an early-stage setup where incremental progress across innovation and ex-CA unit expansion could compound into a more durable growth profile. Worth advancing for a deeper dive, with focus on traffic sustainability, tender rollout performance, and validation of unit economics outside California, followed up by a full model build as well as a conversation with the management or investor relations team at El Pollo Loco.