Re2O: The Next Generation Botox

Long: L&C Bio (KOSDAQ:290650), 12-month Target of ~₩96,000, or ~40% upside

L&C Bio presents a fascinating barbell of clinical stability and hyper-growth. The company boasts a storied history in the Korean medical sector, growing its core surgical graft business into the undisputed domestic gold standard over the last thirteen years. It is an impressive foundation, but while the legacy tissue business certainly has its merits, it merely provides a highly profitable floor to the stock rather than meaningful upside.

Rather, what is driving the massive, ongoing appreciation of the asset is Re2O. The market knows Re2O is a commercial success, and the stock’s recent re-rating reflects the reality of a product that completely overwhelmed its initial supply chain. However, investors are currently pricing a hit domestic product, not a global franchise. Re2O is rapidly positioning itself as the fastest-growing biocompatible injectable in the market, boasting structural advantages over legacy treatments.

As L&C Bio resolves its manufacturing bottlenecks and initiates its export strategy, forward earnings estimates will likely require massive upward revisions. The market has priced in the invention of Re2O, but it has not yet priced in the math of its industrial scaling.

As of this past week, the production ceiling is being removed. L&C Bio received a new GTP facility license from Korea's Gyeonggi regional MFDS office on March 24, 2026, confirming that production capacity will begin scaling from approximately 30,000 units per month to 80,000 units per month starting in May. This is not the gradual ramp management originally guided to. It is an accelerated schedule, with 80,000 units now targeted in H1 rather than H2, and a further expansion targeting 150,000 units per month by October under review. The company is entering its industrial scaling phase.

The investment case is not about whether Re2O will work. It already works. And if you know K-aesthetics customers, these are the most sophisticated beauty consumers in the world, the product provides real results. Rather, this exercise is about what the business looks like when supply finally catches demand, and what multiple that business deserves.

At ₩68,300, the market is pricing a promising medical device company. It is not yet pricing a global aesthetic platform with a structural manufacturing moat, an 80-to-170% price premium over the dominant incumbent product, and expansion vectors in Japan, China, and eventually the United States that are each independently meaningful. The inflection is not coming. It arrived this past week.

The Legacy Foundation: More Than Just a Tissue Bank

Lee Hwan-chul founded L&C Bio in 2011 with a thesis that was straightforward to articulate and extremely difficult to execute: Korea had a world-class medical system with strong demand for reconstructive and aesthetic surgery, but almost no domestic capacity to produce high-quality human tissue allografts. Most of the hADM (human acellular dermal matrix; processed donated human skin from which all cells have been removed, leaving only the structural protein scaffold of collagen, elastin, and related proteins) used in Korean hospitals at the time was imported from the United States, primarily from large non-profit tissue banks that had no particular incentive to develop a Korea-specific distribution relationship. Lee’s plan was to build the Korean version of a tissue bank but with the industrial mindset of a med-tech company rather than the procurement focus of a donation-driven non-profit.

What followed was a decade of genuinely hard work in a category that generates no headlines. Building a GTP-certified manufacturing facility requires navigating Korea’s MFDS at every step. Establishing AATB-accredited donor tissue sourcing relationships with US tissue banks requires demonstrating processing quality standards that meet international benchmarks. Getting surgeons to switch from imported allografts to a domestic product requires clinical trust that accumulates visit by visit, procedure by procedure. None of this is fast, and none of it is glamorous.

By the time Re2O launched in late 2024, L&C Bio had sold 1.72 million units of surgical allograft products across approximately 6,500 hospital, plastic surgery, and dermatology accounts in Korea. That number is the foundation of the commercial story in a way that a simple headcount does not capture. Each of those 6,500 accounts represents an active purchasing relationship, a familiarity with the company’s processing quality, and a physician who has seen the company’s materials perform in clinical settings where failures have real consequences for patients and careers. In Korea’s Gangnam aesthetic medicine market, where a single documented side effect can circulate through medical social networks overnight and end a clinic’s reputation with a particular product line, that institutional credibility is not a soft advantage: It is the reason Re2O could reach 2,000+ clinic accounts within its first year of launch with a highly favorable safety profile noted in early clinical adoption.

The legacy business that built this network is not exciting. Revenue grew from ₩52.6B in 2022 to ₩68.9B in 2023, ₩72.1B in 2024, and ₩85.5B in 2025, the last figure partly reflecting the early Re2O contribution. The allograft products carry approximately 50% gross margins, stable and predictable. MegaDerm for breast reconstruction and burn coverage remains the dominant product in its category in Korea. MegaCarti, for knee cartilage resurfacing, launched in 2023 and is building an independent clinical evidence base. These products are not going to drive meaningful multiple expansion on their own. But they do something equally important: they fund the company’s operations, maintain the clinical relationships that Re2O is being sold through, and provide the regulatory track record that makes international expansion of human tissue products manageable rather than prohibitive.

The Science: Building the Soil vs. Adding Fertilizer

The skinbooster category in Korea has undergone a genuine scientific evolution over the past decade, and understanding where each product sits in that progression is essential for understanding why Re2O commands both a price premium and genuine physician enthusiasm rather than just marketing enthusiasm.

Every product in this category is ultimately trying to address the same underlying biology. Skin aging is fundamentally a structural problem. The dermal extracellular matrix, the scaffold of collagen, elastin, fibronectin, laminin, and glycosaminoglycans that physically supports skin cells and provides mechanical properties like firmness and elasticity, degrades over time. Collagen synthesis declines from approximately age 25 onwards. Matrix metalloproteinases, enzymes that break down ECM (extracellular matrix; the structural protein scaffold of collagen, elastin, and related proteins that gives skin its firmness and elasticity) components, become progressively more active with age, UV exposure, and inflammation. The visible signs of aging, including fine lines, enlarged pores, reduced elasticity, and the flattened appearance of thinning dermis, are the surface expression of a deeper structural collapse that has been occurring for years before it becomes aesthetically apparent.

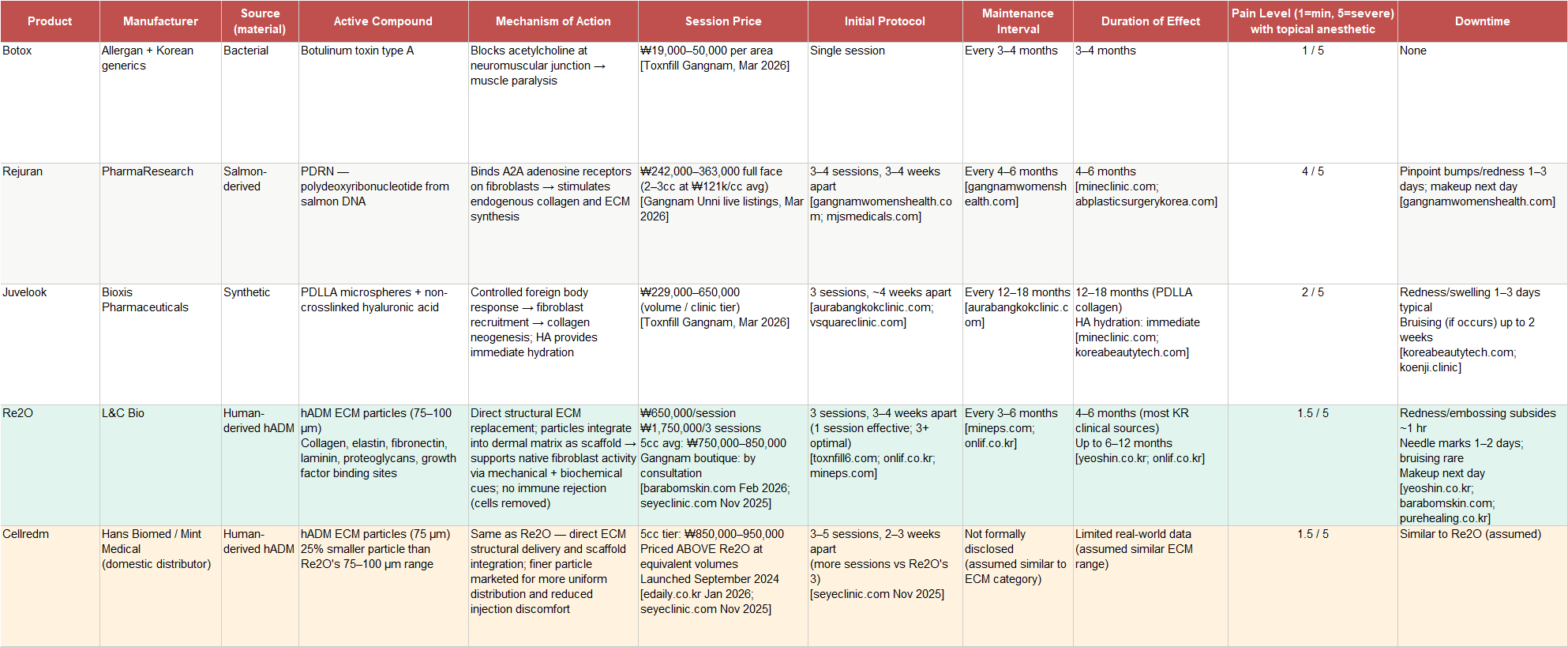

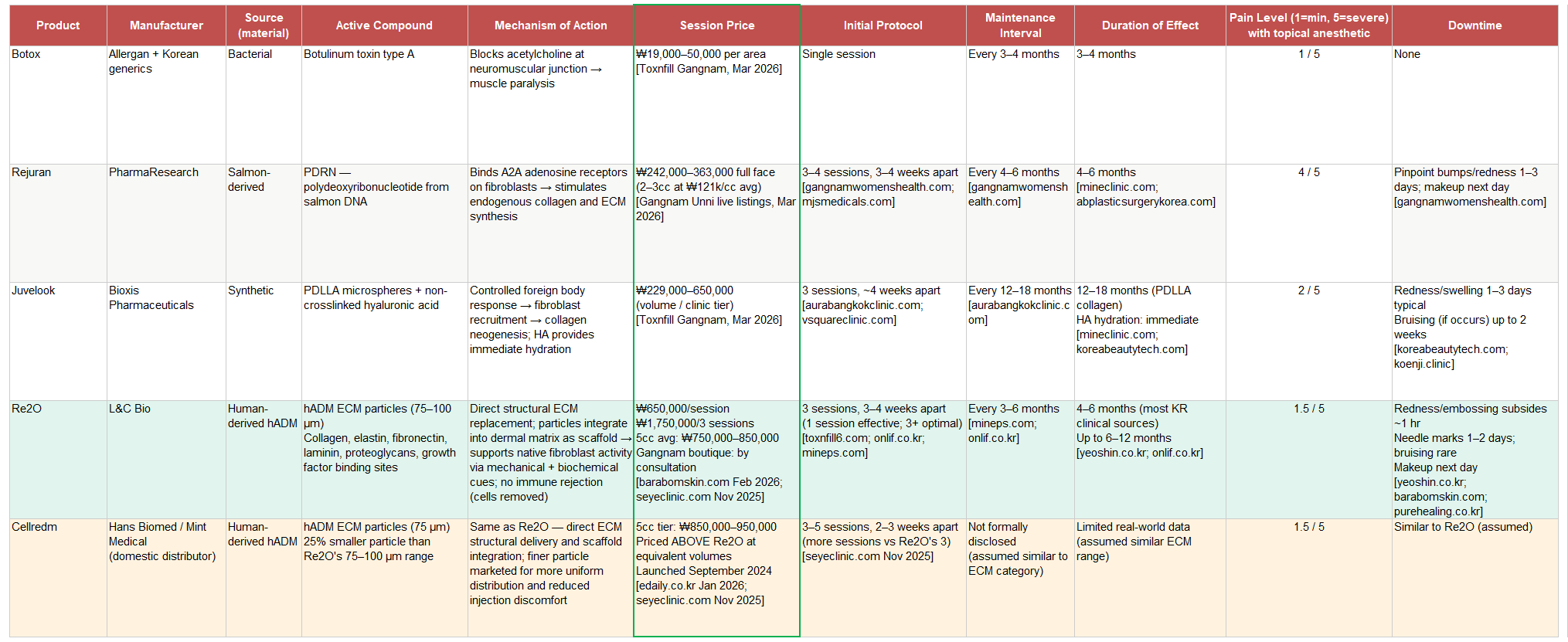

Botox addresses the most superficial layer of this problem by paralyzing the muscles that create dynamic wrinkles. It is effective, highly profitable for the companies that manufacture it, and genuinely useful for its intended purpose. It is also a symptom treatment rather than a structural one. The neurotoxin market in Korea has been competed into commodity territory, with Toxnfill Gangnam listing jaw botox from ₩19,000 per area. That commoditization is not a problem for the skinbooster category. It is the foundation that created it: Korean patients who are already comfortable paying for injectable aesthetic treatments are naturally receptive to moving up the value chain toward products that address more fundamental concerns, at higher price points, as their own skin ages.

Rejuran represents a genuine scientific advance over botox in that it actually engages with the regenerative biology of the dermis rather than simply blocking nerve signals. PDRN, polydeoxyribonucleotide derived from salmon DNA, binds to adenosine receptors on fibroblasts and stimulates those cells to proliferate and produce more collagen and ECM proteins. The signaling cascade is real and the clinical results are documented across a large body of Korean dermatological literature. The limitation is that the mechanism is fundamentally dependent on the functional capacity of the patient’s own fibroblasts. In younger or less damaged skin, Rejuran works well because the fibroblasts are healthy enough to respond vigorously to the signaling. In more aged or UV-damaged skin, where fibroblast function is already compromised, the response is attenuated. You can send all the signals you want, but if the workers are exhausted, the factory output stays low.

One practical consequence of Rejuran's mechanism deserves mention before the price comparison: it is the most painful procedure in its peer group by a significant margin. The high-viscosity PDRN solution injected into shallow dermal layers creates substantial tissue resistance at the needle tip. Patient reviews in Korean online communities are consistent enough to be reliable data; multiple users describe crying during full-face treatments with topical anesthetic, and the product is specifically singled out as the reason many Korean patients ask for gas anesthesia at their clinic. This is not a disqualifying attribute; Rejuran has maintained market leadership for years despite the discomfort. But it is a meaningful gap that Re2O explicitly closes.

Juvelook addresses this problem by bypassing fibroblast signaling entirely and instead inducing a controlled foreign body inflammatory response. PDLLA particles, a bioresorbable synthetic polymer combined with hyaluronic acid, cause the tissue to initiate wound healing, which includes collagen production as a component of the repair cascade. The collagen stimulation is sustained, with effects lasting 12 to 18 months. The mechanism's limitation is the inflammation itself. When PDLLA particles do not distribute evenly in the tissue, the inflammatory response can localize, producing papules that are uncomfortable for the patient and require the treating physician to manage. Juvelook's pain profile is moderate and variable, meaningfully less than Rejuran in most patient comparisons, but dependent on how the clinic dilutes and handles the product.

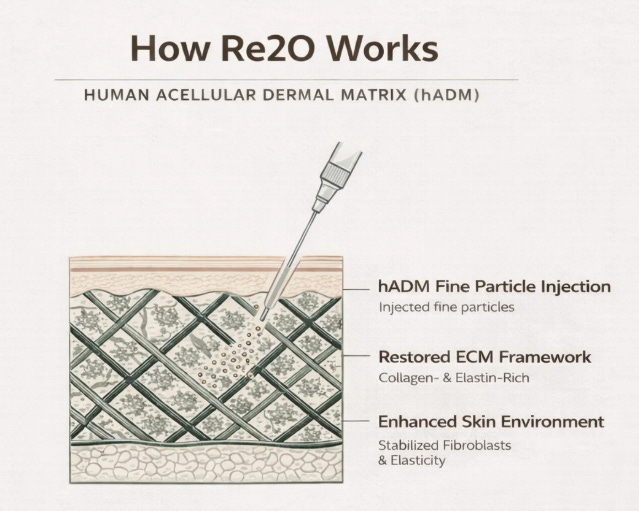

Re2O operates on a different premise entirely. Rather than signaling cells to produce ECM or triggering inflammation to stimulate repair, it directly delivers actual human ECM material into the dermis. The source is hADM processed from donated human skin using the same techniques L&C Bio has employed for surgical reconstruction since 2011. The processing removes all cellular and lipid components, including the immune-activating elements that would otherwise trigger a rejection response, while preserving the native ECM architecture intact: the triple-helix collagen structure that provides tensile strength, the elastin networks that provide recoil, the proteoglycans that bind water and create the hydrated matrix environment, and the growth factor binding sites that naturally facilitate tissue remodeling. This processed material is then micronized to particles averaging 75 to 100 micrometers and suspended in saline for injection.

The clinical hypothesis is elegant precisely because of its directness. Human-derived ECM, having been stripped of its cellular components, is recognized by the recipient’s immune system as structural material rather than foreign tissue. It integrates into the existing dermal matrix, physically filling the architectural voids that aging has created, and then serves as a scaffold that actively supports fibroblast activity through the mechanical and biochemical signals that native ECM provides. Doctors explaining this to patients have converged on the “soil and fertilizer” analogy: Rejuran is adding fertilizer to struggling soil. It works beautifully if the soil still has the capacity to respond. Re2O is changing the soil itself. If the growing environment has degraded to the point where no amount of signaling can restore it, the only path forward is to restore the structural environment first.

What makes this more than just a clever analogy is that L&C Bio’s hADM products have been implanted in surgical contexts for over a decade with an extensive safety record. The biological behavior of processed human acellular dermis in a human host is not a hypothesis. It is a documented clinical reality across millions of MegaDerm implantations in breast reconstruction, burn coverage, and soft tissue repair procedures. Re2O is the same material in injectable form. The mechanism of action in the aesthetic context is newer, but the fundamental safety and biocompatibility profile is grounded in a far larger clinical dataset than any synthetic skinbooster competitor can claim.

The clinical data that has been published specifically for Re2O in the skinbooster indication, while company-sponsored and not yet independently peer-reviewed at scale, reports collagen density 2.9 times higher and elastin density 3.2 times higher at 6 months post-treatment compared to baseline. These figures should be read as directionally indicative pending independent validation. What is corroborated independently and consistently across clinic accounts and patient communities is a pattern of qualitative feedback that aligns with the mechanism: faster downtime than Rejuran, lower procedure pain due to the lower-viscosity suspension, and a distinctly different subjective outcome that patients describe as increased skin density and structural firmness rather than simply surface hydration. For a repeat-procedure product where patient satisfaction directly determines retention rates and referrals, these experiential differences are commercially meaningful.

The Competitive Landscape: Pricing Power as Proof of Concept

The most concrete validation of Re2O’s clinical differentiation is not physician testimony or patient surveys. It is the price. Real-world clinic pricing in Korea tells you more about genuine demand than any marketing document, and the Re2O pricing data, gathered from active clinic websites and booking platforms as of Q1 2026, is striking.

Botox sits at the floor of the Korean aesthetics market. Toxnfill’s Gangnam main branch, one of the most heavily trafficked aesthetic clinics in Korea with a reputation for pricing transparency, lists jaw botox from ₩19,000. The neurotoxin category has been competed to near-commodity pricing, which matters primarily as a reference point for how far the skinbooster category has moved beyond it.

Rejuran is the incumbent second-generation product and the most direct comparator for Re2O's patient population. The standard protocol is an initial course of 3 to 4 sessions spaced 3 to 4 weeks apart, followed by maintenance sessions every 4 to 6 months. A full-face session requires 2 to 3cc. At ₩121,000 per 1cc, the current platform average on Gangnam Unni based on live listings across hundreds of clinics, a single full-face treatment runs ₩242,000 to ₩363,000. Effects last 4 to 6 months. For a patient in active maintenance, the realistic annual spend is ₩500,000 to ₩1,100,000 once the initial loading course is complete.

Re2O published pricing at Barabom Skin in the Seoul metro area is ₩650,000 per session, ₩1,750,000 for three initial sessions. That is an 80 to 170% premium over a comparable single Rejuran session. Re2O requires the same initial course structure (3 sessions at 3 to 4 week intervals) followed by maintenance every 3 to 6 months. At ₩650,000 per maintenance session and 2 to 4 sessions per year, the annual patient spend for Re2O in a maintenance phase runs ₩1,300,000 to ₩2,600,000. Re2O patients spend more annually than Rejuran patients, not approximately the same. The premium is real and sustained across the treatment cycle. Central Gangnam boutique clinics including ID Clinic Gangnam list Re2O by consultation, which typically means pricing above the published floor at practices serving the wealthiest patient demographic.

The competitive differentiation that justifies this premium operates on three levels simultaneously.

First is the mechanism: Re2O is replacing structural tissue rather than stimulating its production, which is a qualitatively different proposition for patients with more advanced skin aging where Rejuran's fibroblast-signaling approach produces diminishing returns.

Second is the procedural experience: Re2O is consistently described as less painful than Rejuran, with faster resolution of post-injection appearance changes. For patients who have tried Rejuran and found the experience difficult, Re2O represents an upgrade in comfort at a premium price point: a combination that markets itself through word of mouth in the Gangnam clinic network.

Third is the safety profile: Re2O is derived from processed human tissue with over a decade of surgical safety data. Physicians who have seen reactions to animal-derived collagen skinboosters, including the pig-collagen products that have generated nodule complaints in Korean clinical settings, treat Re2O's human-derived origin as a genuine differentiator.

Juvelook occupies the price tier between Rejuran and Re2O, with Toxnfill Gangnam listing it from ₩229,000 for a basic volume to ₩650,000 for a full vial. Its longer duration, 12 to 18 months per completed treatment course, means fewer sessions annually and a different annual cost profile than either Rejuran or Re2O. It is a legitimate competitor for patients who prioritize longevity and are comfortable with the inflammatory mechanism and slightly higher post-treatment swelling.

What the pricing data confirms in aggregate is that Re2O has earned its premium through clinical differentiation rather than purchased it through marketing. The company has run no consumer advertising. The product cannot legally be advertised directly to consumers in Korea under the rules governing human tissue products. The ₩650,000 per session floor at a suburban Seoul clinic, and the consultation-only pricing at Gangnam's top-tier practices, represent entirely organic market acceptance. That is the most durable form of pricing power in aesthetics medicine.

Cellredm, from Hans Biomed, is the most important competitive development in the ECM category and requires more precise characterization than it has received in most analyses. It launched in September 2024, a couple month before Re2O, making these two products simultaneous market entrants rather than a first-mover and follower. Cellredm uses finer 75-micrometer hADM particles versus Re2O’s 75 to 100-micrometer range, and markets this as an advantage for uniform distribution and reduced injection discomfort. At the clinic level, Cellredm prices above Re2O at equivalent volumes, approximately ₩850,000 to ₩950,000 for a 5cc session versus ₩750,000 to ₩850,000 for Re2O, positioning itself as the premium offering within the ECM category.

While these two products were launched into the market at similar times, the number of searches for Re2O vastly outstrips Cellredm. So while stated efficacy could be similar, the customer acquisition costs required for Cellredm to reach similar mindshare as Re2O would be difficult financially, which is a critical aspect of L&C Bio’s competitive advantage in this realm.

The Third Pillar: MegaCarti and the Cartilage Opportunity

While the aesthetics market drives the multiple, L&C Bio is quietly building a second high-value application for its ECM platform in orthopedics that the market is not currently pricing at all.

Knee cartilage occupies a uniquely frustrating position in medicine: it is one of the most commonly damaged tissues in the human body, it does not regenerate on its own in any clinically meaningful way, and the current standard of care options are either inadequate or extraordinarily complex. Microfracture surgery, which involves drilling small holes in the subchondral bone to stimulate a bleeding response that creates fibrocartilage, produces repair tissue that is mechanically inferior to native hyaline cartilage and frequently deteriorates within 5 years. Stem cell therapies such as Medipost’s Cartistem represent a genuine scientific advance but require a complex live-cell supply chain: the cells must be harvested from a donor, cultured in a laboratory under controlled conditions, and implanted in a second surgical procedure, creating logistical complexity, cost, and outcome variability based on cell viability at the time of implantation.

MegaCarti applies the same logic to cartilage that Re2O applies to skin. It is micronized human cartilage, an off-the-shelf ECM material that does not require culturing or a separate cell harvest surgery. A surgeon can apply MegaCarti during a routine arthroscopy, the same single-procedure that patients are already undergoing for cartilage damage assessment and treatment. The material is bioidentical to the tissue it is replacing, eliminating the immune compatibility concerns that affect synthetic alternatives, and it provides the structural scaffold that supports native chondrocyte activity and tissue integration.

The economic case for hospitals and surgeons is compelling. A single-step arthroscopic procedure is significantly more efficient than a two-step protocol requiring cell culture coordination between harvest and implantation. For a busy orthopedic practice, the workflow simplification alone is a meaningful adoption driver. For patients, particularly older patients where cartilage damage from osteoarthritis is most prevalent and where the risks of complex multi-stage procedures are most significant, an off-the-shelf solution that can be applied during a procedure they are already scheduled for has obvious appeal.

The addressable market is substantial. Knee osteoarthritis affects an estimated 300 million people globally. In Korea specifically, where the aging demographic is pronounced and the population is highly willing to pay for medical interventions to maintain quality of life, MegaCarti has a natural growth runway that extends well beyond the current early-adopter base. The global cartilage repair and restoration market was estimated at approximately $5B in 2023 and is growing at roughly 8% annually.

MegaCarti’s current position is that of an early-stage product with a compelling clinical rationale but limited revenue contribution relative to Re2O. In 2024 it experienced a sales pause that management attributed to the timing of reimbursement negotiations; the product is currently approved under Korea’s new medical technology exemption status for patients aged 19 to 60, and expansion of the eligible age range following the 2026 full evaluation could substantially widen the addressable patient pool. The orthopedic opportunity is genuinely a medium-term story rather than a 2026 catalyst, but the fact that the market is paying zero for it in the current valuation makes it pure optionality that costs nothing to hold.

The Inflection: May 2026 Is the Moment

The single most important datapoint this week was not a clinical result, a new market entry, or an analyst upgrade. It was the March 24 announcement that L&C Bio had received a new GTP facility license from the Gyeonggi regional MFDS office and that production would scale from 30,000 to 80,000 units per month beginning in May 2026.

To understand why this matters, it helps to track how the capacity guidance has evolved. At the time of the 2025 annual results in late February, the company was running at approximately 24,000 units per month. The guidance at that time was for 50,000 units per month in H1 2026 and 80,000 in H2. The March 24 announcement superseded all of that. The company has now pulled the 80,000 unit target forward from H2 to H1, with May as the start of the ramp. Additionally, a further expansion is under review targeting a separate production facility for completion in October 2026, which the company believes could push monthly capacity to 150,000 units or more by year end.

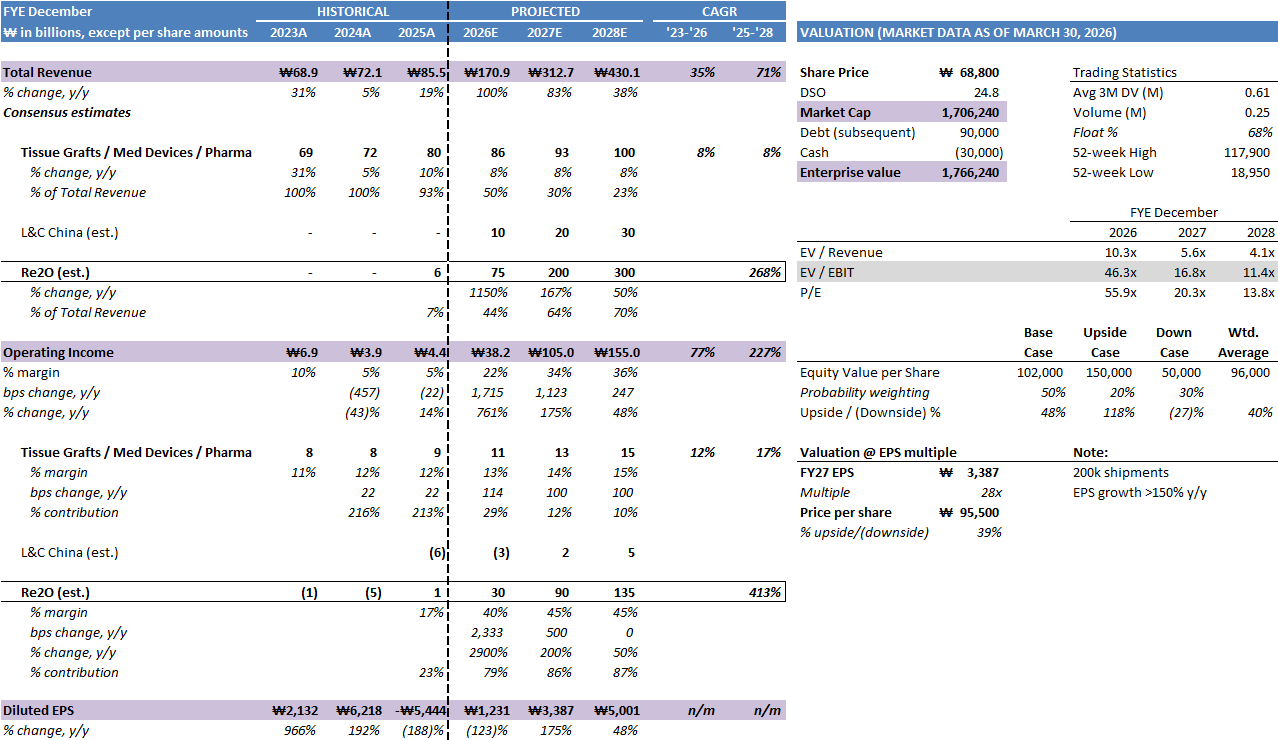

At 150,000 units per month in H2 as the baseline (likely to expand >200,000), and assuming an average selling price that scales upward as geographic expansion shifts the blended rate toward premium international markets, the annualized Re2O revenue run-rate should approach ₩200B to ₩250B on a standalone product basis. That number is not a prediction for 2026. It is an illustration of where the capacity ceiling moves if the October expansion completes and export to new geographies is executed.

The practical implications for 2026 revenue are meaningful. At 80,000 units per month from May through December, total Re2O production capacity for the remaining 8 months of 2026 is approximately 640,000 units. At an average realization of roughly ₩80,000 per unit at the clinic level (consistent with the ₩650,000 session price spread across a patient population and accounting for the domestic versus export channel mix), that is approximately ₩51B of capacity-driven revenue potential in the back half of the year alone, before any H1 contribution. The ₩50B annual guidance does not look aggressive against this production backdrop. If anything, it looks conservative.

The mechanism of the expansion also matters. This is not greenfield construction. The new GTP certification covers a facility that was already physically built and equipped, requiring certification rather than construction as the final step. The H2 150,000-unit target uses process automation and efficiency improvements in existing certified space, meaning the capital intensity is low relative to the revenue upside. For a company with ₩85.5B in annual revenue and approximately ₩40B in gross profit, a scaling initiative that adds potentially ₩100B to ₩150B in high-margin revenue through process improvements rather than major capital expenditure is exactly the kind of operating leverage that drives dramatic multiple re-rating.

The Regulatory Map: Four Markets, Four Different Stories

Korea is resolved and requires minimal elaboration. Re2O is MFDS-approved as a human tissue product, the manufacturing facility is GTP-certified, and the clinical track record across 2,000+ accounts is building the evidence base that supports ongoing market penetration. The regulatory dimension in Korea is now purely an execution question: how fast can the company supply the demand that the market has already demonstrated it will absorb.

Japan is live and underappreciated. L&C Bio has actively initiated its Japan expansion, with official export momentum building in early 2026. Japan’s PMDA has established pathways for human tissue products used in regenerative medicine, and L&C Bio leveraged its existing MegaDerm Japan registration as a template for Re2O approval. The Japanese aesthetic medicine market is distinctive for several reasons that are favorable for Re2O specifically. Japanese patients have a strong cultural preference for treatments with visible scientific credibility rather than synthetic appearance. The K-Beauty influence in Japan has been well-documented and translated into strong consumer awareness of Korean aesthetic innovations before they are formally launched through Japanese clinical channels. And pricing in Japanese aesthetic medicine typically sits at a premium to Korea, supporting favorable margins on exported volume. The H2 2026 plan to expand overseas supply as domestic capacity normalizes positions Japan as the first major international revenue contributor beyond Korea.

China is the most complex and the most important medium-term opportunity in the model. The strategy is layered and worth understanding in detail.

The foundation layer is MegaDerm Plus. After receiving NMPA import approval, L&C Bio appears to have moved MegaDerm Plus into the early commercial stage in China, though public reporting on the exact timing of full-scale sales has not been entirely consistent. The company has signed 23 distribution partner agreements and is targeting ₩10B of MegaDerm Plus revenue in 2026. This is not just a revenue contributor. It is a trust-building exercise with Chinese regulators, physicians, and distribution partners that creates the pathway for Re2O to follow. The company has noted that MegaDerm Plus sold through its initial Chinese import allocation rapidly, which is meaningful as a demand signal for premium human tissue products in the Chinese market.

The second layer is Re2O. Chinese clinical trials are planned for 2026, with NMPA approval for domestic production at the Kunshan facility targeted for 2027. The Kunshan facility already exists as the MegaDerm Plus processing base. Converting it to Re2O production does not require building a new facility; it requires securing the NMPA approval for the Re2O product specifically and potentially adding Re2O-specific processing equipment. Kunshan GMP certification for expanded operations is a 2026 target.

The third layer is the strategic partnership dimension. L&C Bio has disclosed that it is in discussions with Chinese strategic investors regarding technology transfer and equity participation in L&C China. If a major Chinese healthcare or aesthetics group takes an equity stake in L&C China, it changes the distribution dynamic from a foreign company selling into China to a jointly owned enterprise with local institutional backing, which materially reduces the political and regulatory friction that has historically impeded Korean medical product expansion in China.

China’s skinbooster market is estimated at approximately ₩2.5 trillion, roughly 15 times the size of the Korean market. Even 1% share would represent ₩25B. Even 0.5% share would represent ₩12.5B. These are not heroic assumptions. They are the mathematical consequence of a premium, differentiated, biocompatible human collagen product entering the largest aesthetics market in the world with established distribution infrastructure already in place.

The United States is the longest-duration opportunity and the most complex regulatory environment. Human tissue products in the U.S. are evaluated under the FDA’s HCT/P framework in 21 CFR Part 1271, and a product can be regulated solely under Section 361 only if it satisfies all of the relevant criteria, including minimal manipulation and homologous use. If a product does not fit cleanly within that framework, it can instead fall into a much heavier regulatory category as a device, biologic, or combination product.

For Re2O, the key point is that the U.S. pathway should still be treated as an open regulatory question. One possible strategy would be to pursue device classification for a reformulated ECM product through the 510(k) process, which would require an FDA-acceptable substantial-equivalence argument to a legally marketed predicate. But public evidence does not yet establish that such a pathway is available for Re2O specifically, or that FDA would accept the proposed classification.

Existing U.S. products such as Renuva are relevant mainly as proof that physicians and regulators are already familiar with certain injectable allograft-derived matrices. But Renuva is marketed as an allograft adipose matrix within the HCT/P framework, not as a 510(k)-cleared dermal matrix device, so it should not be treated as direct proof of a straightforward predicate path for Re2O.

That makes the U.S. opportunity valuable but still speculative. If L&C Bio can secure a lighter-touch regulatory route, the market could be economically important given materially higher U.S. aesthetic pricing. Until the company discloses a clearer FDA strategy and timeline, however, U.S. revenue is better treated as upside optionality than as part of a base-case model.

Channel Checks: The Signals Beyond the Financial Statements

Three independent analytical threads corroborate the demand picture that the financial statements are only beginning to reflect.

The clinic penetration trajectory is the most direct. Re2O launched at approximately 500 clinic accounts in its first months of availability. By August 2025, within 9 months of launch, it had reached 1,000 accounts including both direct L&C Bio relationships and Humedix partnership accounts. By end-2025 the company reported over 2,000 accounts, a further doubling in the second half of the year. This acceleration in the rate of clinic adoption is not typical of a product with ordinary demand characteristics. Products that plateau at 500 accounts tend to grow slowly from there as early adopter excitement fades and the mainstream clinical market proves more skeptical. Products that double from 1,000 to 2,000 accounts in the same timeframe that supply constraints are limiting the ability to serve existing demand are different animals.

The pricing discipline is the second signal. Re2O has maintained its ₩600,000 to ₩700,000 per session pricing despite supply shortages. In a normal product market, constrained supply creates pricing pressure in the opposite direction: clinics either substitute a competing product or negotiate harder for supply allocation. The fact that Re2O has not experienced either dynamic suggests that the clinical differentiation is sufficient that physicians are willing to wait for supply rather than immediately substitute, including with Cellredm, which is available from a credible manufacturer and priced at the same tier. That wide-spread substitution resistance is a meaningful data point about perceived replaceability.

The physician conference activity provides the third independent thread. L&C Bio served as a featured presenter/sponsor of Korea Derma 2025, Korea’s largest international dermatology conference, where Re2O was presented not merely as a commercial product but as a clinical topic with academic physicians presenting data from their own patient populations. An academic physician who presents data at a major conference is not a passive user of a product. They are an advocate who has incorporated the product into their practice sufficiently to generate publishable outcomes. The number of KOL physicians at 50+ hospitals actively generating formal clinical datasets for Re2O, as reported by the company, is a downstream indicator of the product’s clinical credibility independent of any company-controlled messaging.

The Financial Architecture: Reading Through the Noise

L&C Bio’s 2025 financial statements contain three numbers that require careful interpretation.

The first is revenue of ₩85.5B, a 18.5% increase from ₩72.1B in 2024. This growth rate understates the Re2O contribution because production constraints limited how much of the existing demand the company could actually convert to revenue. At 24,000 units per month near the end of 2025, Re2O generated approximately ₩6B against demonstrated demand that exceeded supply at every point in the year. The revenue figure is a capacity number, not a demand number. When capacity is the binding constraint, comparing revenue growth rates across periods obscures what matters, which is what the demand curve looks like when supply normalizes.

The second is operating income of ₩4.2B at a 5% margin, down from the 2024 trajectory. This is directly attributable to the China consolidation cost, as explained elsewhere in this piece: L&C Bio converted L&C China from a minority equity stake to a fully owned subsidiary in late 2025, triggering full consolidation of the Chinese subsidiary’s costs and losses into the parent’s income statement. The company’s own Q3 2025 filing attributed the operating margin compression explicitly to this accounting change. With that one-time effect behind it, and with Re2O contributing a larger share of revenues at structurally higher margins in 2026, the operating margin trajectory is strongly upward.

The third is the GAAP net loss of ₩129.1B, which is the number that generates confusion among investors unfamiliar with Korean convertible bond accounting. L&C Bio issued a convertible bond in April 2025. As the stock price rose during the year, the fair value of the embedded conversion option increased, and under K-IFRS this unrealized appreciation is recognized as a financial expense in the issuer’s income statement.

Strip these two items out and operating net income for 2025 was approximately ₩3.2B, consistent with ₩4.4B operating income. That is the operational baseline from which the 2026 ramp begins.

The Risk Register

Intellectual honesty requires acknowledging the scenarios under which this thesis fails.

The capacity ramp is management guidance, not a committed production schedule. Biological manufacturing scale-up is nonlinear. Validation timelines can extend. Yield rates are not publicly disclosed. The 80,000 unit May target may slip by weeks or months without fundamentally breaking the thesis, but a multi-quarter delay would compress the 2026 revenue profile meaningfully and might delay the market’s willingness to price 2027 earnings, which is what the price target is premised on.

China is almost certainly going to produce timeline disappointments relative to official guidance. NMPA review for human tissue products is slow, politically sensitive, and subject to disruption from Korea-China bilateral dynamics. The ₩10B MegaDerm Plus China revenue target for 2026 is achievable given the distribution agreements signed and the product approval already in hand, but Re2O China revenue should not be embedded in base case models before 2028.

Conclusion: The Regenerative Sovereign

L&C Bio is what happens when a deep-moat medical company discovers a consumer-luxury application for technology it has been quietly perfecting for over a decade. The infrastructure is already built. The clinical credibility is established. The product has proven it can command a premium at scale. The international pipeline is funded by free cash flow from a stable legacy business. And as of this week, the single constraint that had been limiting revenue recognition, production capacity, is formally being removed.

The market is paying ₩1,700B for a business that generated ₩85.5B in revenue last year and is guiding to ₩150B this year. That looks expensive until you decompose the unit economics: Re2O at 80 to 170% price premiums over its nearest competitor, 50% gross margins on a product with demonstrated supply-constrained demand, >40% operating margins with limited ongoing operating expenses, and a capacity expansion that is front-loaded into H1 2026 rather than distributed across the year. The earnings trajectory from here to 2027, assuming execution, is steep enough that the current multiple is not the right frame for assessing value.

You are buying the infrastructure for something close to the price of a tissue bank, and the global aesthetic platform that sits on top of that infrastructure is still being valued as an afterthought. The production constraint that obscured the demand signal for all of 2025 is being resolved in May.

Looking forward: at ₩175B in 2026 revenue with Re2O at ₩75B (my estimate, company guided to ₩50B) carrying ~40-50% operating margins (lower in 2026 as production scales) and legacy at ₩100B carrying low-to mid-teens operating margins, this implies operating income of approximately ₩40B. At a 22% effective tax rate and normal interest costs, EPS is approximately ₩1,200 per share.

By 2027, if capacity reaches >150,000 units per month and Japan and China begin contributing meaningfully, a revenue base of ~₩300B with Re2O at ₩200B implies operating EPS of approximately ₩3,000 to ₩3,500, with a bull case approaching the ₩5,733 figure that a full capacity utilization scenario produces. At 30x forward earnings (which will be nearly tripling y/y) on the conservative end of that range, the stock is worth ~₩96,000.

Watch item: The key is H1 2026 monthly Re2O revenue, which should approach ₩5B to ₩6B per month by early 2H if the 80,000 unit production ramp executes as announced. If it does, the multiple re-rating happens quickly. If it does not, reassess.