Signet Jewelers: Revisiting the Bear Case

Why a reassessment of the lab-grown thesis leaves me more constructive than consensus

The market’s bear case on Signet has been straightforward for years: lab-grown diamonds (LGD) are deflationary, Signet is heavily exposed to bridal, and lower stone prices should eventually compress ticket and margin economics across the business. That framing gets an important part of the story right. Lab-grown has been deflationary at the stone level. But it may be incomplete in how that deflation has actually flowed through to the retailer. (See below for how bear thesis is positioned, most recently highlighted by The Bear Cave / Edwin Dorsey, who, to be fair, makes credible points).

Across the last five reported quarters, Signet’s average unit retail have held up better than that narrative would suggest, helped by upsizing behavior, fashion mix, and assortment architecture that positions lab-grown not as a discount product but as a way to preserve ticket at higher carat weights. If that lens is closer to correct, then the real risks are less immediate ticket collapse and more long-run bridal volume pressure and eventual lab-grown commoditization. That distinction matters for a business trading around 9x forward earnings with a double-digit free cash flow yield.

Why the Original Lab-Grown Thesis Was Incomplete

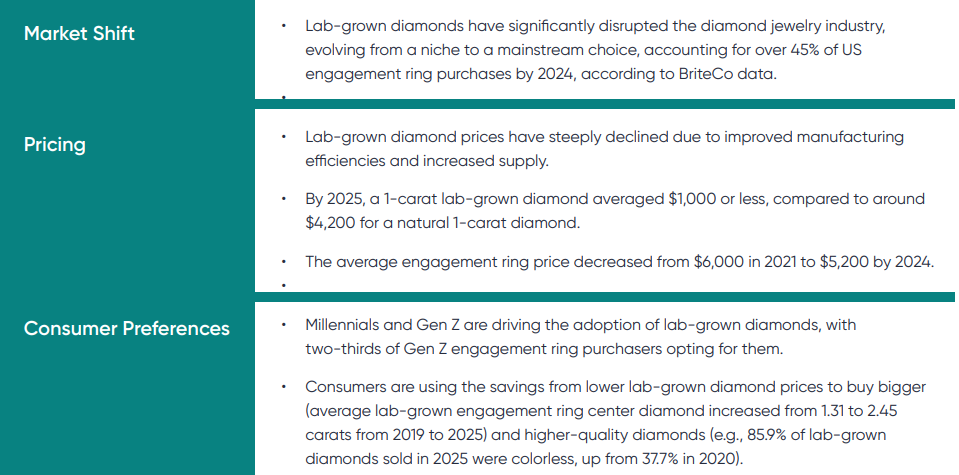

The conventional framing when lab-grown diamonds entered the mainstream around 2020 was intuitive: a product that is chemically identical to a mined diamond but costs 70-80% less should trade at 70-80% less. That price gap should flow through to retailers in the form of lower average selling prices, compressing gross margins across the bridal category. For a business deriving roughly 60% of revenue from bridal, the market read this as an existential structural headwind.

The flaw was not that the concern was baseless. LGD has been genuinely deflationary at the stone level. BriteCo’s insurance data shows a one-carat lab-grown diamond averaging around $1,000 in 2025 versus roughly $4,200 for the natural equivalent. Average engagement ring prices nationally fell from approximately $6,000 in 2021 to $5,200 by 2024. That is real deflation at the category level, and the bears who predicted it were not wrong about that part.

Where the thesis was incomplete is in what it predicted would happen at the retailer. It assumed the buyer would anchor on the diamond, purchase the same stone they would have bought in natural form, and pocket the savings. What actually happened is that the buyer anchored on the budget, walked in with the same $3,000-$5,000 they had always allocated to an engagement ring, and bought a materially larger stone, often in a higher-karat gold setting. Signet offset most of the per-stone deflation through upsizing, mix shift into fashion categories, and setting cost increases driven by higher gold prices.

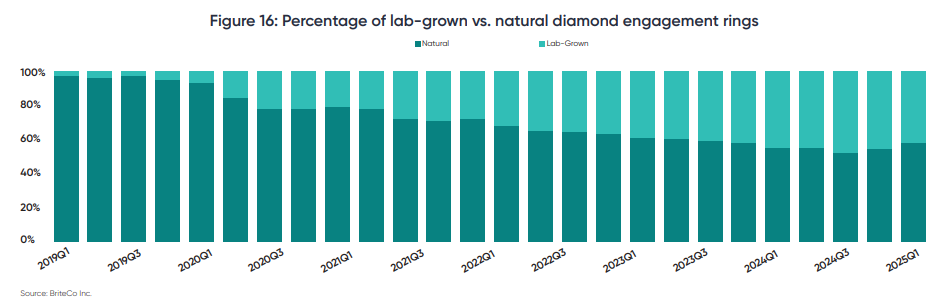

BriteCo’s data makes the upsizing dynamic concrete. The average lab-grown engagement ring center stone grew from 1.31 carats in 2019 to 2.45 carats by 2025. Over the same period, the average natural diamond center stone moved from 1.50 to 1.62 carats. The LGD buyer did not buy a cheaper ring, they bought a bigger ring for roughly the same money. The 5.7% decline in average ring prices looks considerably more benign than what a pure stone-deflation model would have predicted given LGD going from 2% to over 50% of center stone sales in five years.

Kay’s vice president of merchandising put it directly in JCK Magazine in February 2025:

“Many couples gravitate toward 1.5 to 2 carats, but with lab-created diamonds, they’re able to go even bigger while staying within budget.”

The budget is the anchor while the carat is the variable. That behavioral reality is what the market mis-prices, and understanding it is the starting point for the Signet thesis.

What Signet’s Own Catalogs Reveal

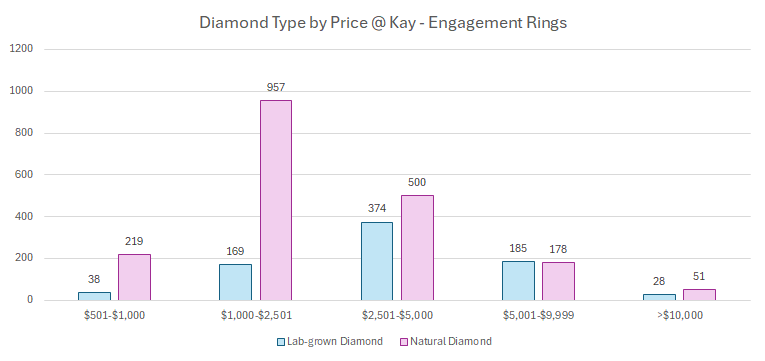

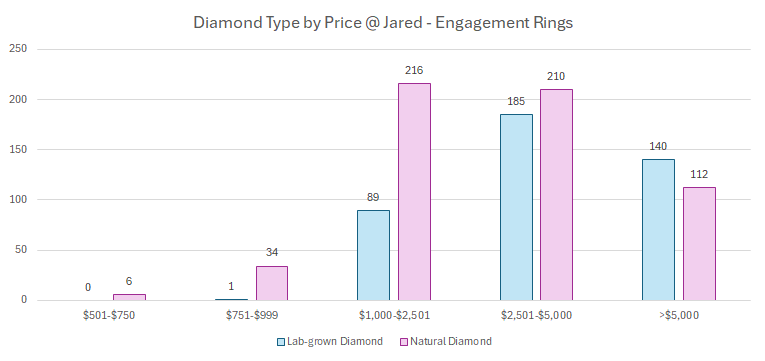

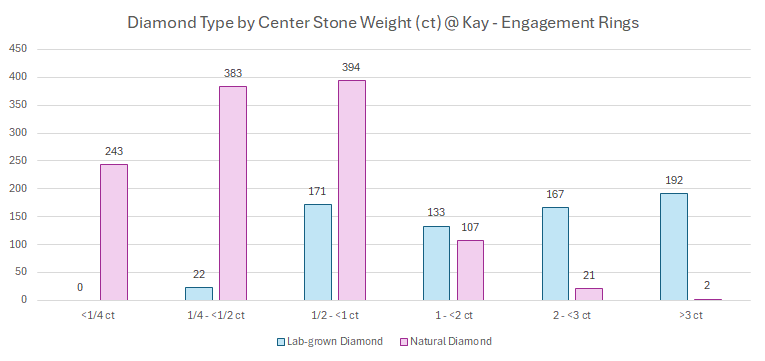

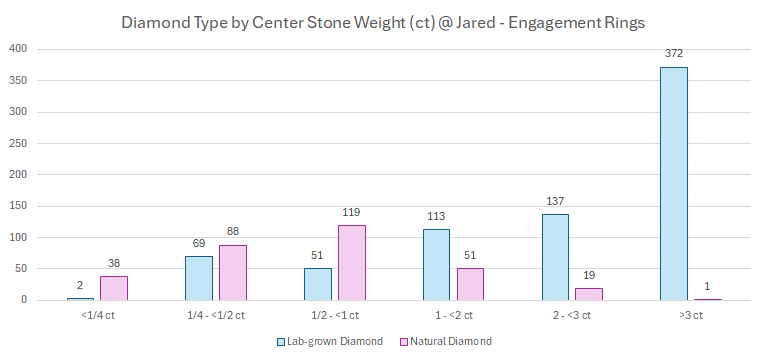

Proprietary analysis of the Kay.com and Jared.com engagement ring catalogs, categorized by diamond type across price point and center stone weight, produces four charts that map the same structural pattern across two distinct price tiers. The specific SKU counts will shift as listings rotate, but the architecture they reveal reflects deliberate assortment strategy rather than random variation. Kay is Signet’s mass-market flagship with a sweet spot in the $1,000-$5,000 range. Jared is the premium off-mall banner, running heavier toward $2,500-$10,000 and above. Both banners tell the same story.

At both banners, natural diamonds dominate the entry-level price tiers by a wide margin and lab-grown closes the gap and then inverts it as you move up. At Kay, natural leads below $2,501 by roughly 5-to-1. In the $2,501-$5,000 tier, lab-grown closes to 374 against 500. In the $5,001-$9,999 tier, the count is 185 lab-grown against 178 natural, essentially parity. At Jared, which runs heavier toward $2,500-$10,000, the crossover comes faster: from near-parity at $2,501-$5,000, lab-grown leads outright above $5,000 at 140 to 112. At Signet’s own premium banner, lab-grown has more listings than natural at the highest prices. Signet is not merchandising LGD as a discount product; it is using it to populate premium visible price tiers that natural diamonds at those price points would have left thinner.

The carat weight data makes the mechanism explicit. Below one carat at both banners, natural overwhelms lab-grown by roughly 5-to-1 across all size buckets. The crossover comes at one to two carats, where lab-grown takes a narrow lead at Kay (133 to 107) and a wider one at Jared (113 to 51). Above two carats, natural diamond has effectively exited the assortment: at Kay the ratio is 167 to 21 at two-to-three carats and 192 to 2 above three. At Jared it is 137 to 19 at two-to-three carats and 372 to 1 at three carats and above.

That figure is evidence of strategic merchandising positioning rather than proved unit economics. SKU count does not translate directly to sales volume or gross profit contribution. But it does tell you what Signet believes the premium customer wants access to, and at what price tier. A three-carat natural diamond engagement ring at Jared prices would cost $30,000-$80,000. Lab-grown makes the same visual experience accessible for $8,000-$15,000. Signet has structured its premium banner around that accessibility, and the question for investors is whether it is capturing the transaction value that comes with it.

The pattern is consistent across both banners: sub-one-carat is largely natural, above one carat belongs increasingly to lab-grown, and the price data shows lab-grown achieving and then exceeding natural in SKU count above the $2,500-$5,000 tier. A buyer with $4,000 at Kay chooses between a one-carat natural and a two-carat lab-grown, and Signet preserves the transaction opportunity either way. A buyer with $7,000 at Jared finds more lab-grown options than natural ones. That catalog architecture reflects a deliberate strategy built around keeping the transaction value intact while expanding carat access, not one built around competing on price.

The AUR Data Checks the Catalog Thesis Against Reported Numbers

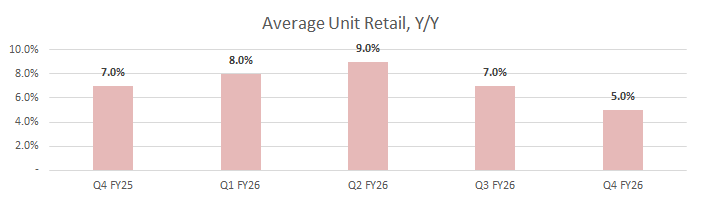

Signet reported average transaction value through FY2025 (ending January), then transitioned to the average unit retail metric from Q4 FY2025 under new CEO J.K. Symancyk. The sequence matters because it covers the exact period when LGD penetration was accelerating hardest.

Signet reported average transaction value (ATV) through most of FY2025, with North America ATV turning -1.6% in Q1 FY2025, then improving in Q2 and holding in Q3 rather than continuing to deteriorate. That sequence matters because it spans the period when the market’s bear case hardened around lab-grown diamonds: LGD penetration was rising sharply, and a weak ticket early in FY2025 reinforced the view that mix was shifting lower. By Q4 FY2025, after J.K. Symancyk had taken over as CEO, Signet began emphasizing average unit retail (AUR) instead, and the metric inflected to +7%. AUR then stayed positive for five consecutive quarters: +8% in Q1 FY2026, +9% in Q2 FY2026 (Bridal +4% and Fashion +12%), +7% in Q3 FY2026 (Bridal +6% and Fashion +8%), and +5% in Q4 FY2026. Full-year FY2026 AUR was +7%. In other words, Signet delivered sustained positive unit-retail growth during the same broad period when LGD penetration was at or near its highest levels in bridal and rising meaningfully in fashion, which undercuts the simpler bear read-through that higher LGD mix necessarily meant ongoing ticket pressure.

Here’s how Signet’s FY2026 10K attributes AUR growth in North America:

AUR in North America was bolstered by a focus on our assortment strategy, particularly in LGD fashion, as well as the impact of higher gold prices.

That attribution matters because it identifies two distinct contributors. Gold prices lifted the cost of settings on every ring mechanically, regardless of diamond type. LGD fashion expansion drove higher average prices because lab-grown made diamond jewelry economically viable in categories previously priced below $200 per piece: tennis bracelets, everyday earrings, stackable rings. Both are real, but only the second is a Signet-specific advantage.

The merchandise margin line reflects the tension. In Q4 FY2026, when AUR was up 5%, Signet reported merchandise margin down 30 basis points year over year because of higher commodity costs and tariffs, only partially offset by assortment architecture and services mix. AUR growth is a necessary condition for the pricing-power thesis but not sufficient on its own. What the data establishes clearly is that the simplest version of the deflationary bear case, that LGD would mechanically collapse revenue per unit, has not materialized across five reported quarters.

Where the Bears Still Have a Case

The operating data weakens one version of the bear thesis, not all of them. Two legitimate concerns survive.

The first is demographic. The structural tailwind that underpinned Signet’s business for a century was a simple sociological norm: people got married, and they bought diamond rings to mark the occasion. Marriage rates in the United States have been declining for decades. The average age of first marriage has risen to 30 for men and 28 for women. Each year of delayed marriage compresses the bridal addressable market in the near term, and a population that marries less frequently eventually compresses it structurally. Signet’s own guidance for FY2027 assumes comparable sales in a range of down 1.25% to up 2.5%, a range centered close to flat. The company is managing for volume pressure, with roughly 100 store closures planned in FY2027. Portfolio rightsizing is disciplined capital management, not a growth strategy.

The second surviving bear thesis is commoditization. LGD production costs have been falling rapidly, and BriteCo explicitly frames the category as bifurcating toward accessible everyday luxury. If consumers become more price-transparent and less banner-loyal in lab-grown, Signet’s ability to capture markup on the LGD assortment compresses over time. This risk is distinct from the demographic one: it is not about fewer rings being sold, but about each ring generating less gross profit for Signet specifically (as of now, LGD is margin accretive to SIG). The question is not whether this dynamic is possible but whether it has yet shown up in reported numbers, which is what the previous section addresses.

The services business provides a partial structural offset to both. Services revenue has comped positive for nearly five consecutive years at high-single-digit growth, driven by repair, protection plans, and extended warranties attached to existing rings. That installed base of covered jewelry does not contract when fewer new rings are sold in a given year. Services carries structurally higher margins than merchandise and generates the repeat visits that drive fashion attachment from existing customers. The services business is not a disclosed standalone segment with clean separable valuation inputs, so calling the market’s treatment of it a proved pricing error goes further than the data supports. But the general observation that a recurring revenue stream growing at high single digits deserves a better multiple than the transactional jewelry business it sits alongside is not unreasonable.

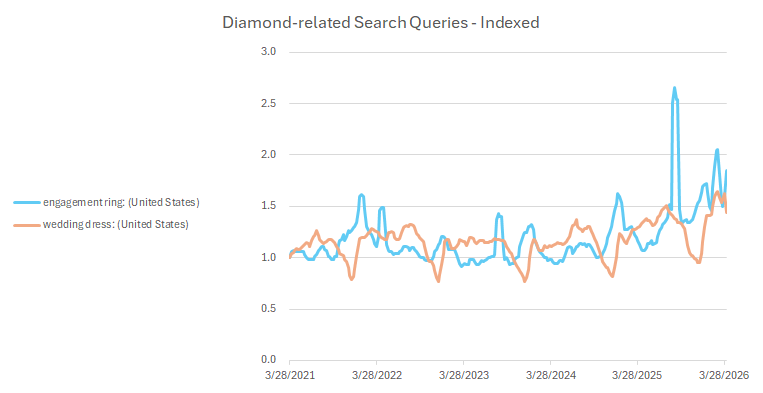

On timing, the near-term bridal picture is better than the structural framing implies. Management discussed positive Valentine’s Day momentum going into FY2027 and engagement unit growth across Kay, Zales, and Jared. Google Trends data for “engagement ring” searches in the United States, indexed to 2021, shows the sustained floor running well above the 2021-2024 range from late 2024 onward, with “wedding dress” searches tracking in the same direction.

Search intent is directional rather than conclusive, but the combination of improving operating data and elevated search activity is at least inconsistent with a category in acute structural decline. The more precise read is that delayed proposals during 2022-2023 may be coming through now, a cohort effect rather than a permanent demand loss.

What the Multiple Implies

At roughly $85 per share with approximately 40.1 million shares outstanding as of mid-March 2026, Signet’s current market capitalization is approximately $3.4 billion. Net of $875 million in cash, net enterprise value is approximately $2.5 billion. For the trailing earnings multiple, Signet reported FY2026 adjusted diluted EPS of approximately $9.60 on a diluted weighted-average share count of 41.6 million for the fiscal year. Using that reported EPS against the current share price gives a trailing P/E of approximately 8.8x, and EV against FY2026 adjusted EBITDA of approximately $687 million gives roughly 3.7x.

Those multiples imply the market expects today’s transaction value resilience to prove temporary. That may turn out to be correct. The commoditization and demographic risks are real and this piece does not dismiss them. But the specific mechanism the market appears to have been discounting, that LGD would immediately compress Signet’s reported ticket values, has not appeared across five quarters of data. If that mechanism was the primary driver of the discount, the multiple is harder to justify at current levels.

The buyback math provides one concrete way to think about it. FY2026 adjusted EPS was $9.60 on 41.6 million diluted weighted-average shares. With approximately $518 million in buyback authorization remaining and the company repurchasing at roughly $175-200 million annually, the diluted share count for FY2027 is likely in the 38-40 million range. That mechanical tailwind alone adds approximately $0.40-$0.60 to EPS on flat operating income. Modest operating leverage at the midpoint of FY2027 guidance adds another increment, putting forward EPS in a range around $10.50-$11.50 (guidance is $8.80 to $10.74) without requiring any improvement in comparable sales. At 8.8x trailing and 8-9x forward, the stock prices in meaningful deterioration. If the market ultimately treats the current resilience as more durable than temporary, a case can be made for a 12x forward EPS. The multiple needed to reach that range is the real question, and it depends on whether commoditization and demographic pressure show up in margins or not before the market recalibrates.

Risks & Considerations

The commoditization risk introduced in the prior section would show up in the reported numbers in a specific way: merchandise margin compression even while AUR holds, driven by Signet needing to match online pricing to retain LGD traffic rather than capturing the full banner premium. As online retailers with lower overhead continue to expand LGD assortment and stone-quality comparisons become easier on price-comparison platforms, the markup Signet earns on lab-grown inventory faces structural pressure. The Q4 FY2026 merchandise margin declining 30 basis points is not conclusive evidence of this dynamic, since gold and tariff costs explain much of it, but merchandise margin rate is the metric to watch in coming quarters alongside AUR.

The demographic risk is structural and operates on a longer timeframe. If US marriage rates continue their secular decline without stabilizing, bridal volume pressure intensifies through the decade in ways that services growth and fashion expansion only partially offset. This is the scenario in which the stock earns its current multiple rather than re-rating. In terms of upside risk, I would not discount the influence of cultural factors such as Taylor Swift’s engagement and upcoming wedding/baby birth as well as increasing religious activity for the Gen-Z demo.

Gold prices cut both ways. Significantly higher gold prices through 2024-2025 contributed mechanically to AUR growth by lifting the cost of every 14K and 18K gold setting. A material gold price reversal would make FY2027 and FY2028 AUR comparisons harder independent of diamond economics.

Tariffs on imported finished jewelry are a near-term operational uncertainty. Signet sources meaningfully from Asian manufacturing, and escalating tariff costs either compress merchandise margins or get passed through in ways that soften demand at margin-sensitive price points. Management described the current tariff environment as manageable through pricing and assortment actions, but the uncertainty carries real optionality in both directions.

Closing Thoughts

The market has been pricing Signet as though lab-grown diamonds would mechanically collapse its ticket economics. That specific mechanism has not materialized across five reported quarters. The catalog architecture at both Kay and Jared shows LGD positioned at premium price points and carats, not discount ones. The operating data shows AUR expanding, with contributions from assortment mix, fashion category expansion, and higher gold settings alongside the mechanical gold-price lift. The simplest version of the bear thesis was mis-specified.

The risks that survive that conclusion are real but different. Structural demographic pressure on bridal volumes is a long-duration headwind. Future LGD commoditization, if it erodes banner loyalty and price transparency improves, could compress the markup that Signet has so far captured from the format shift. Merchandise margins are under pressure from gold and tariffs even as transaction values rise. These are the right questions to interrogate, not the question of whether lab-grown automatically destroys Signet’s revenue per ring.

I do not think the data presented here eliminates the bear case. But it does suggest the market may be leaning on the wrong mechanism. If lab-grown has not yet produced the ticket compression many expected, and the more relevant risks are instead slower-moving volume pressure and eventual commoditization, then the current multiple looks more pessimistic than the reported economics justify. A case can be made for a materially higher multiple for a business with demonstrated average unit retail resilience through a major format disruption, a recurring services stream growing at high single digits, and a share count contracting by 6-8% per year. The gap between 9x and a more defensible discount sits closer to 12x. That gap is where the opportunity lives.