The Peptide Foundries

Brief discussion on two important specialized peptide manufacturers

Every blockbuster GLP-1 drug, every next-generation obesity therapeutic, every peptide in the combined clinical and preclinical pipeline of over 500 candidates requires the same thing before it can reach a single patient: someone has to manufacture the active pharmaceutical ingredient. At the commercial scale that semaglutide and tirzepatide now demand, the number of organizations on earth capable of doing that work reliably, at purity levels that satisfy regulators, is still small relative to demand.

Bachem Holding (SIX:BANB) and PolyPeptide Group (SIX:PPGN) are among the leading independent Western peptide API manufacturers, with scale, regulatory history, and installed capacity that few peers can match. Third-party estimates of their combined peptide CDMO market share vary, some put Bachem at 25% and PolyPeptide at 20% while others have placed Bachem closer to 17%. The exact numbers are less important than the structural picture: these two companies, along with CordenPharma (private, owned by Astorg, €880 million in 2023 revenue, targeting over €1 billion in peptide platform sales by 2028), form the core of the Western peptide CDMO capacity base.

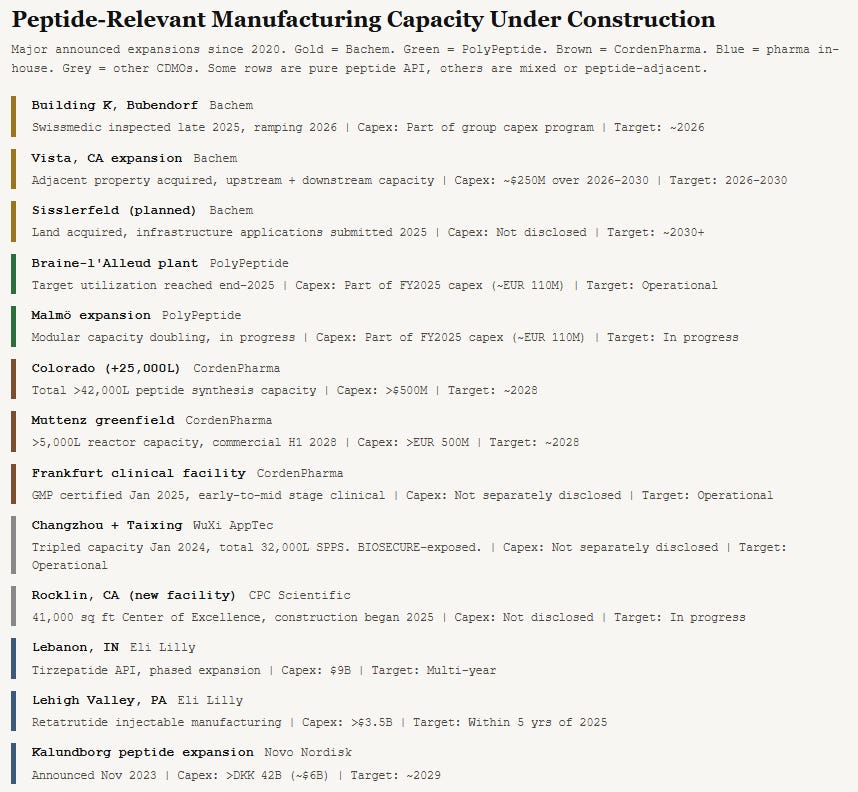

The market is concentrated but not static. CordenPharma is investing more than €1 billion across a Colorado expansion (adding 25,000 liters of peptide synthesis capacity to reach 42,000 liters by 2028) and a new greenfield facility near Basel in Muttenz, Switzerland. AmbioPharm, Thermo Fisher, and a growing set of Asian manufacturers are investing as well. The competitive set is broadening even as demand grows.

This is a picks-and-shovels thesis. The question is not which GLP-1 drug wins, which obesity indication gets approved next, or whether Novo Nordisk or Eli Lilly captures the incremental prescription. The question is whether the total volume of peptide API manufactured globally will be dramatically larger five years from now than it is today. If the answer is yes, Bachem and PolyPeptide are among the primary beneficiaries.

The capacity constraints already suggest the answer is yes.

What Exactly Do These Companies Do?

It is worth understanding the actual work, because the nature of peptide manufacturing is central to why these businesses are difficult to replicate.

Semaglutide is a 31-amino-acid peptide. Tirzepatide is 39 amino acids. Each must be assembled one amino acid at a time in precise sequence, then separated from its manufacturing scaffold, purified to pharmaceutical grade, and converted into a stable form for formulation. The basic chemistry has been understood since the 1960s. What cannot be easily replicated is how to do this at commercial scale with the yield, purity, and consistency that regulators require across tens of thousands of batches.

Bachem has been refining this process since 1971. PolyPeptide since 1952. Between them they have accumulated well over a century of institutional knowledge about what goes wrong when you try to manufacture complex peptides in 1,000-liter reactors: side reactions that accumulate as chains get longer, impurities that appear only at scale, purification challenges that no textbook covers. The most valuable process know-how is proprietary, accumulated through decades of production experience rather than captured in published literature.

Bachem operates manufacturing sites in Bubendorf and Vionnaz (Switzerland), Vista and Torrance (California), and St Helens (UK). Building K in Bubendorf, its newest and most advanced large-scale production plant, completed its initial regulatory inspection by Swissmedic in late 2025, creating an essential prerequisite for high-volume production. Gradual commercial ramp-up is planned for 2026. The company employs over 2,300 people.

PolyPeptide operates six GMP-certified sites: Braine-l’Alleud (Belgium), Malmö (Sweden), Strasbourg (France), Ambernath (India), Torrance and San Diego (California). The company employs approximately 1,400 people. The Belgian site, where a large-scale peptide manufacturing plant ramp-up drove a 24% revenue increase in H1 2025, is the most important near-term growth driver. The Malmö site is undergoing modular capacity doubling.

Both companies provide end-to-end services: process development, clinical-stage manufacturing, and commercial manufacturing. This cradle-to-commercial relationship creates strong stickiness. Once a pharmaceutical company has validated its manufacturing process with a CDMO and received regulatory approval based on material produced at that specific facility, changing suppliers requires a site transfer, process revalidation, and a regulatory supplement filing. For a blockbuster drug generating billions in annual revenue, the risk and cost of switching are rarely justified.

Why This Trend Is Sustainable

The dominant force is the GLP-1 market itself. The global GLP-1 receptor agonist market was valued at approximately $66 billion in 2025 and is projected to reach somewhere between $130 billion and $250 billion by the early 2030s depending on the estimate. Novo Nordisk and Eli Lilly together generated tens of billions in GLP-1 revenue in 2025, and both are investing aggressively in manufacturing capacity while relying on CDMOs to supplement their own production. Every milligram of semaglutide or tirzepatide requires peptide API. Bachem signed a single supply contract worth a minimum of CHF 1 billion over five years (2025 to 2029).

But the thesis does not depend on GLP-1 alone. There are currently more than 150 peptides in active clinical trials, with another 400 to 600 in preclinical development. The pipeline extends well beyond metabolic disease: peptide-drug conjugates in oncology, radiopeptide therapies in prostate cancer, antimicrobial peptides against drug-resistant infections, and next-generation multi-agonists like retatrutide and survodutide in late-stage trials. Each of these programs needs a CDMO.

Why Can’t Someone Bigger Just Do This?

This is the most important question. The answer reveals why Bachem and PolyPeptide’s positions are durable, though not impregnable.

The barriers to entry are reinforcing.

Regulatory validation is the most obvious. Peptide API manufacturing facilities must be inspected and approved by the FDA, EMA, Swissmedic, PMDA, and others. Bachem’s facilities have been continuously inspected and approved for over four decades. Building a new facility and getting it through regulatory inspection takes three to five years minimum. Building the track record that gives pharmaceutical companies confidence takes a decade or more.

Process know-how is harder to see but more durable. The gap between textbook chemistry and commercial-scale manufacturing with consistent yield and purity is enormous. Bachem has published peer-reviewed research on specific failure modes in peptide synthesis that represents the visible tip of a much larger body of proprietary knowledge. The unpublished knowledge is the moat.

Customer switching costs lock in relationships. Once a drug is approved using API from a specific CDMO facility, switching requires site transfer, process revalidation, and a regulatory supplement filing. For a blockbuster generating billions in annual revenue, switching is rarely justified.

Capital intensity sets the floor. Bachem reported CHF 333 million of capex in 2025 and plans more than CHF 400 million in 2026. Building K has been under construction since 2021. PolyPeptide reported EUR 110 million in 2025 capex. CordenPharma is investing more than €1 billion over three years.

Vertical integration widens the gap. Bachem manufactures its own protected amino acid building blocks, the fundamental raw materials of peptide synthesis. Its catalog lists over 4,400 products. When Bachem produces a peptide API, it is using its own internally manufactured starting materials at every step. This creates cost, quality, and supply-chain security advantages that PolyPeptide (which lacks comparable backward integration, one reason its margins are structurally lower) and new entrants cannot easily match.

These barriers are real but not absolute. CordenPharma is explicitly targeting the leading position in peptide CDMO. Some large pharma customers will insource over time. The industry structure may evolve from a tight oligopoly to a somewhat broader Western supply base. But even in that scenario, total market growth is fast enough that Bachem and PolyPeptide can continue to grow without needing to win share from competitors.

Bachem: The Category Leader

Bachem describes itself as a leading, innovation-driven company specializing in the development and manufacture of peptides and oligonucleotides for research, clinical development, and commercial application. Founded in 1971 by Peter Grogg, Bachem grew from a two-person operation in Liestal, Switzerland into a global specialist through decades of reinvestment. Grogg ran the company as CEO for over 30 years and served as Chairman until 2012. The Grogg family still exerts meaningful influence through Ingro Finanz AG, with Nicole Grogg Hötzer serving as Vice-Chairwoman of the Board.

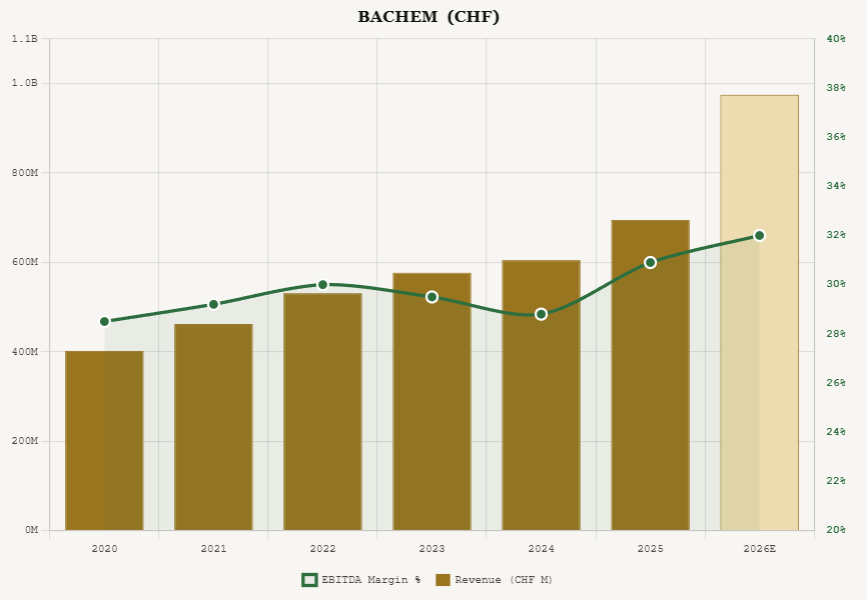

Revenue grew from approximately CHF 300 million in 2018 to CHF 402 million in 2020, then to CHF 531 million in 2022, CHF 577 million in 2023, CHF 605 million in 2024, and CHF 695 million in 2025. Management is guiding for 35 to 45 percent sales growth in local currencies for 2026, implying revenue approaching or exceeding CHF 1 billion. The wide range reflects genuine uncertainty about the Building K ramp pace.

EBITDA was CHF 215 million in 2025 with a margin of 30.9%. Net income reached CHF 149 million, up 24% year over year. Earnings per share were CHF 1.98. Management guided for an EBITDA margin in the low thirties in local currencies for 2026.

At the April 10, 2026 close of CHF 66.35, Bachem’s enterprise value was about CHF 5.00 billion, including CHF 26.4 million of year-end 2025 net debt. That implies roughly 23.3x trailing EV/EBITDA on FY2025 EBITDA of CHF 214.7 million. On 2026 guidance, forward EV/EBITDA compresses to roughly 15–16x, depending on where the EBITDA margin lands within management’s “low thirties” range.

The CHF 1 billion supply contract signed for 2025 to 2029 provides unusual revenue visibility. For a CDMO, multi-year committed volumes of this magnitude are rare and reflect the strategic importance Bachem holds for at least one major pharmaceutical customer.

Bachem has been building an oligonucleotide business since 2019. The FDA-approved oligonucleotide therapeutic base has expanded materially over time, reaching roughly two dozen therapies by 2025.

PolyPeptide: The Margin-Recovery Play

Where Bachem is the established premium player, PolyPeptide is the higher-beta recovery story.

The company traces its origins to 1952 in Malmö, Sweden. It was taken public on the SIX Swiss Exchange in 2021 at approximately CHF 64 per share. The stock subsequently fell below CHF 13 in 2024 as the company struggled with margin compression and the hangover from a post-IPO investment cycle. Draupnir Holding B.V. controls 55.47% of shares, with ultimate control through the Cryosphere Foundation (registered in Guernsey) and Frederik Paulsen (based in Lausanne) named as a beneficiary. Draupnir has committed to maintaining majority ownership for the foreseeable future. Older PolyPeptide corporate materials describe the company as producing around one third of all commercial therapeutic peptides, underscoring its historical scale in the category.

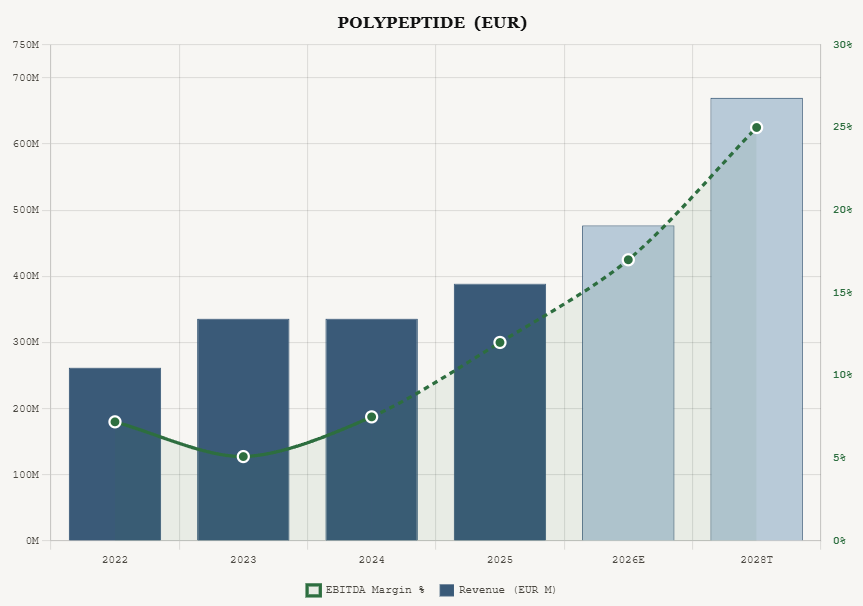

Revenue was EUR 389 million in 2025, up 16% year over year, driven primarily by metabolic therapeutics (per management commentary). EBITDA reached EUR 47 million with margins improving to 12.0% from 7.5% in 2024. Management guided for 20 to 25 percent revenue growth in 2026 with an EBITDA margin in the mid- to high-teens. The midterm target is to double 2023 revenue by 2028 (implying roughly EUR 670 million) with EBITDA margins approaching 25%.

At the April 10, 2026 close of CHF 31.65, PolyPeptide’s enterprise value was about CHF 1.14 billion, or roughly EUR 1.24 billion. That implies approximately 26.5x trailing EV/EBITDA on FY2025 EBITDA of EUR 46.8 million. On 2028 targets of roughly EUR 670 million revenue and ~25% EBITDA margin, forward EV/EBITDA compresses to about 7.4x. These multiples remain low relative to CDMO peers, though not as cheap as they appeared at the CHF 28 level where the stock traded earlier in April.

The risk is execution. PolyPeptide is still rebuilding margins, its multi-site manufacturing footprint is complex, and any slippage in capacity ramp-up or utilization could push the 25% EBITDA-margin target further out. The company is still losing money on a net income basis, with FY2025 EPS of negative EUR 0.64.

The Bull Case

The pharmaceutical industry is experiencing a generational shift toward peptide therapeutics, and the manufacturing infrastructure required to support that shift does not yet exist at sufficient scale.

For Bachem, the case is that Building K ramps successfully, driving revenue past CHF 1 billion in 2026 with EBITDA margins in the low thirties. The catalyst calendar is rich: CagriSema’s FDA decision is expected around October 2026, retatrutide has seven Phase 3 readouts through 2026 with projected approval in 2027 or 2028 (GlobalData projects $15.6 billion in sales by 2031), survodutide’s SYNCHRONIZE Phase 3 program should deliver initial readouts by late 2026, and oral semaglutide (still a peptide requiring peptide API, unlike orforglipron) is ramping commercially. Each commercial launch means a new long-duration manufacturing relationship for the CDMOs that supplied the clinical material. The consensus analyst target as of March 2026 is approximately CHF 78, with a wide range from CHF 46 to CHF 110 reflecting disagreement about Building K execution and long-term growth rates.

For PolyPeptide, the case is a margin recovery story. Revenue growth in the low twenties funded by GLP-1 demand combines with operating leverage from capacity expansion to drive EBITDA margins from 12% in 2025 toward 25% by 2028. Net income flips positive, analyst coverage increases, and the stock re-rates from distressed turnaround levels. Analyst consensus as of March 2026 sits around CHF 36, with a range from the mid-twenties to the mid-forties.

The Risks

The most immediate risk for Bachem is Building K execution. The 2026 revenue target of CHF 1 billion-plus is explicitly contingent on the successful ramp-up of this single facility. The guidance range of 35 to 45 percent growth (a spread of hundreds of millions of CHF) reflects genuine uncertainty. Bachem itself described Building K’s gradual ramp-up as a “key prerequisite” for achieving its 2026 sales target.

For PolyPeptide, the primary risk is that margin recovery stalls. The company is still losing money on a net income basis. If expansion costs overrun or demand does not materialize at the pace expected, the path to 25% EBITDA margins could stretch beyond 2028.

Both companies face customer concentration risk. Bachem’s top 5 customers accounted for 48% of 2025 sales and its top 10 for 63%. The CHF 1 billion supply contract, while providing revenue visibility, means a meaningful portion of revenue depends on a single customer relationship.

The biggest long-term risk is the oral pill. On April 1, 2026, the FDA approved Eli Lilly’s Foundayo (orforglipron), the first approved non-peptide oral GLP-1 for weight management. It is a conventional small molecule, meaning it can be manufactured cheaply at enormous scale using standard pharmaceutical chemistry. No specialized peptide reactors, no cold chain, no injectable delivery. Patients can take it at any time with or without food. Self-pay pricing starts at $149 per month. Clarivate projects $11.1 billion in obesity sales by 2031 in major markets. Those are revenues that will not flow through peptide manufacturers.

The bear case is clear: if oral pills capture the majority of new obesity prescriptions, demand for peptide manufacturing grows far more slowly than the headline market figures suggest. Lilly is building a facility in Alabama at a cost of more than $6 billion for Foundayo and other pill-based drugs.

Here is why the bear case may cap upside without necessarily breaking the thesis.

The pills work, but not nearly as well as the injectables. Foundayo delivered roughly up to 12% body weight loss in its main trial. The injectable peptide drugs deliver far more: tirzepatide (Zepbound) up to 22.5%, retatrutide (still in trials) 28.7%, and CagriSema (Novo Nordisk’s next-generation combination) 20.4%. Every one of these higher-efficacy drugs is a peptide. The most effective weight loss drugs on the market and in the pipeline are peptides, and that gap is unlikely to close.

Meanwhile, these peptide drugs are expanding into entirely new diseases. Semaglutide (the Ozempic ingredient) now has FDA approval for fatty liver disease and kidney disease, and is under review for heart failure and artery disease. These are new patient populations worth billions in additional revenue, and the oral pill has no clinical data in any of them yet.

The market is also not zero-sum. Roughly 40% of US adults are clinically obese and fewer than 5% are currently on a GLP-1 drug. The oral pill will bring in patients who would never have given themselves an injection. Many of those patients will eventually switch to injectables for stronger results. The net effect: Foundayo likely caps what share of the obesity market flows through peptide manufacturers, but the total market is growing so fast through new drugs and new diseases that the floor keeps rising.

The semaglutide patent cliff is a separate risk that on closer examination looks more like a tailwind. The core patent expired in March 2026 in India, China, Brazil, Canada, and several other large markets. Multiple generic versions are in advanced trials. Every generic manufacturer needs peptide ingredient, and they are far more likely to use chemical synthesis rather than Novo Nordisk’s proprietary fermentation process. The regulatory pathway for a short peptide like semaglutide (31 amino acids) is simpler than for a full biologic, which lowers the barrier for generic entrants. More generic producers means more demand for peptide manufacturing capacity. In the US and Europe, Novo Nordisk’s secondary patents extend protection until 2031 to 2032.

U.S. policy is also shifting in favor of Western manufacturers. The BIOSECURE Act, signed into law in December 2025 (per Latham & Watkins, Ropes & Gray, and other legal analyses), restricts federal agencies from contracting with designated foreign biotech companies. The practical effect is narrower than many investor narratives have implied, but the directional signal favors Western manufacturers with no Chinese production exposure.

Currency risk is a practical consideration for non-Swiss investors. Both companies report in Swiss francs (Bachem) or euros (PolyPeptide) but generate substantial revenue in US dollars.

Valuation risk is the simplest to describe. Bachem, at 33.5x trailing earnings, is priced for continued execution, so any stumble would likely result in meaningful multiple compression. PolyPeptide is less exposed on that dimension because more of its valuation still depends on future margin recovery than on already-delivered profitability, but its lower liquidity means selling pressure could produce outsized price moves.

Valuation Context: How CDMOs Trade

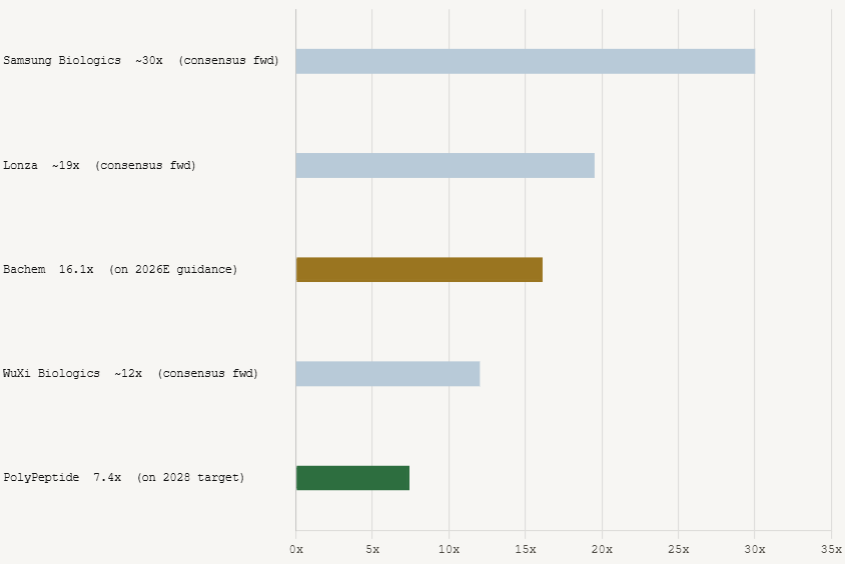

As of Q1 2026, the global CDMO sector spans a wide range on forward EV/EBITDA. Samsung Biologics trades at approximately 30x. Lonza sits at roughly 18 to 21x with 5.9x EV/Sales. WuXi Biologics has compressed to around 12x. The segment average for global leaders sits in the low to mid 20x range. Emerging growth CDMOs generally trade between 13x and 18x forward EV/EBITDA.

Bachem at an EV of approximately CHF 5 billion against CHF 215 million of 2025 EBITDA trades at roughly 23x trailing equity value to EBITDA. On 2026 guidance, the multiple compresses to approximately 16x forward, which is cheaper relative to Lonza and Samsung Biologics given that Bachem is guiding for 35 to 45 percent revenue growth while those peers are growing 10 to 20 percent.

PolyPeptide at an EV of approximately CHF 1.14 billion (EUR 1.24 billion) against EUR 47 million of 2025 EBITDA trades at roughly 26x trailing, but this is misleading because the margin is at trough levels (12% versus a 25% midterm target). On 2028 targets, the stock trades at approximately 7.4x forward EV to EBITDA. Even with a meaningful discount for execution risk, the valuation compression from trailing to forward multiples is significant, and the underlying business is growing 20 percent annually on demand that management attributes specifically to metabolic therapeutics.

Positioning Within The Opportunity Set

The most useful frame is to think about these two companies as complementary expressions of the same structural thesis.

Bachem is the lower-risk, higher-quality expression. A compounder: the category leader with 54 years of operating history, a 31% EBITDA margin, a CHF 1 billion multi-year supply agreement, and family ownership alignment.

PolyPeptide is the higher-risk, higher-reward expression. A turnaround: a business with meaningful market share at roughly one-fifth of Bachem’s equity value, with the explicit bet that margins normalize as capacity ramps and operating leverage kicks in.

A barbell approach, owning both, gives exposure to the structural peptide thesis through two distinct risk profiles. The correlation between the two stocks is high (same end-market), but the return drivers are different (Bachem is earnings growth, PolyPeptide is margin recovery).

The manufacturing bottleneck is real. The switching costs are real. The demand trajectory is as well-supported by evidence as any secular trend in healthcare today. The competitive set is broadening with CordenPharma’s billion-euro investment, and some customers will insource over time, so framing this as a permanent two-company monopoly overstates the case. But in a market growing 15 percent annually with multi-year customer lock-in and five-year build-out timelines for new capacity, incumbency has value.